Quick Summary

- Federal employees and uniformed service members can roll over TSP funds into a Gold IRA, but only after separating from service or reaching age 59½.

- The TSP does not allow direct investment in physical gold; a self-directed IRA is the only way to hold precious metals in a federally tax-advantaged retirement account.

- A direct rollover is the safest transfer method, avoiding the 20% federal tax withholding that hits indirect rollovers.

- You don’t have to move your entire TSP balance; partial rollovers are allowed, giving you flexibility to diversify without going all in.

- Keep reading to find out which IRS-approved gold coins and bars qualify, how much a Gold IRA costs, and how gold stacks up against the TSP’s G Fund and C Fund.

Table of Contents

- Quick Summary

- Federal Employees Can Move TSP Funds to Gold: Here’s What You Need to Know First

- TSP Rollover vs. TSP Transfer: The Difference Matters

- How to Convert Your TSP to a Gold IRA in 5 Steps

- Costs Involved in a TSP to Gold IRA Transfer

- Tax Implications of Rolling Over a TSP to a Gold IRA

- Your TSP Retirement Savings Deserve More Than One Option

- Frequently Asked Questions

Federal Employees Can Move TSP Funds to

Your TSP has been quietly growing for years, but it only offers a handful of fund options, none of which include physical gold. For federal employees looking to hedge against inflation or diversify beyond stock and bond funds, a TSP-to-Gold IRA transfer opens a door most government workers don’t even know exists.

For people beginning their gold investment research, professional guidance is necessary to take the initial steps.

Augusta Precious Metals specializes in helping federal employees navigate this exact process, breaking down the rules, costs, and steps involved in moving TSP funds into IRS-compliant precious metals accounts.

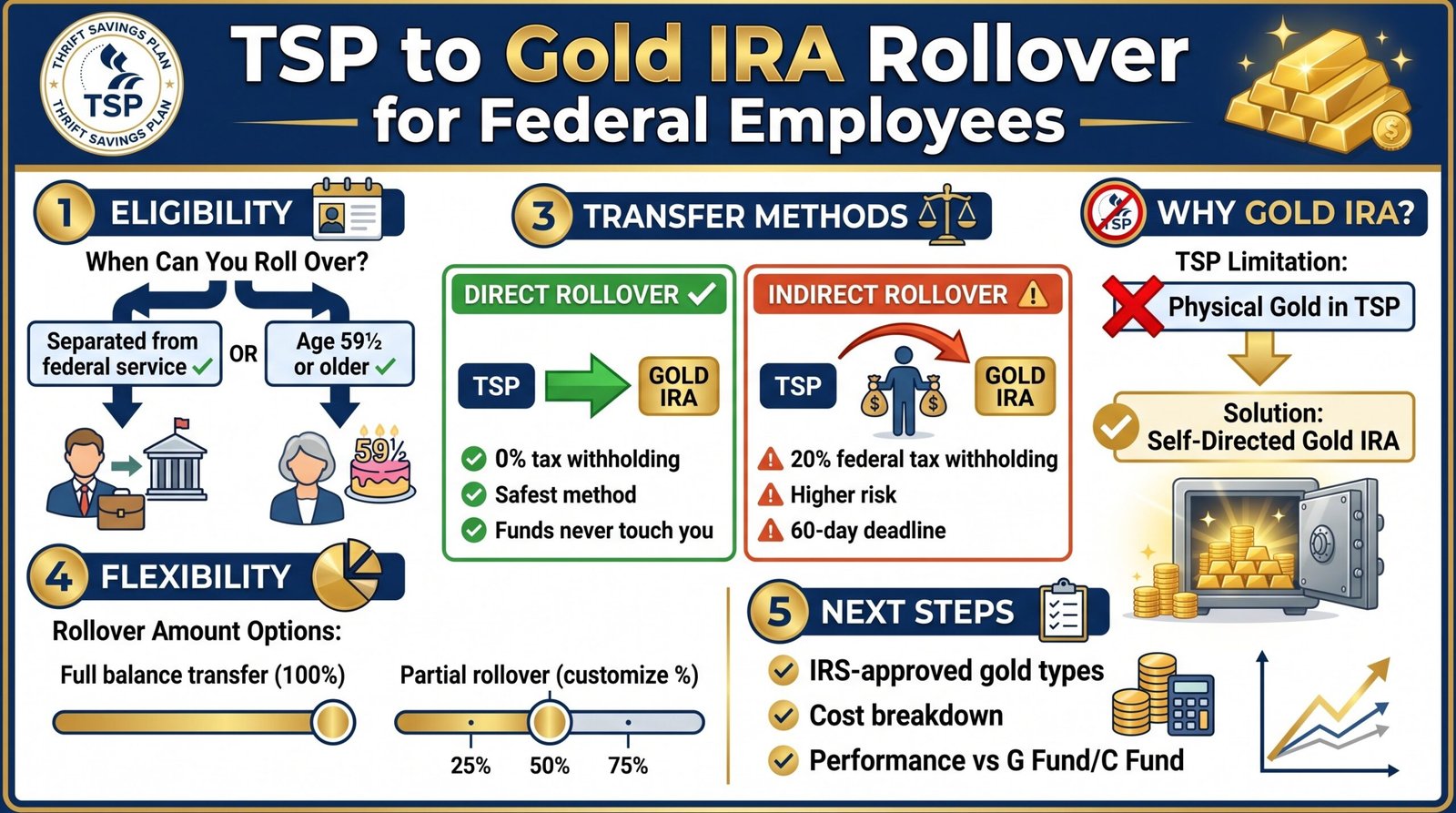

Who Is Eligible to Roll Over a TSP to a Gold IRA

Not every federal employee can initiate a TSP rollover at will. Eligibility hinges on two key conditions: you must have either separated from federal service or reached age 59½ while still employed. Once either condition is met, you’re eligible to roll over all or part of your TSP balance into a self-directed Gold IRA.

Members of the uniformed services follow the same rules. If you’re still actively employed and under 59½, an in-service withdrawal may be limited, so timing your rollover matters.

Why the TSP Cannot Hold Physical Gold Directly

The Thrift Savings Plan is a government-sponsored defined contribution plan with a fixed menu of investment funds: the G, F, C, S, I, and L Funds. Physical commodities like gold bullion are simply not on that menu. Even indirect exposure through gold mining company stocks is not permitted within TSP fund structures. The TSP is built for simplicity, not alternative assets.

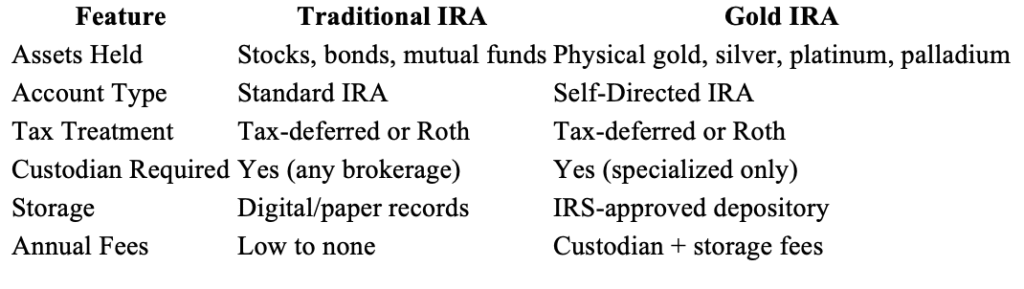

What a Self-Directed Gold IRA Actually Is

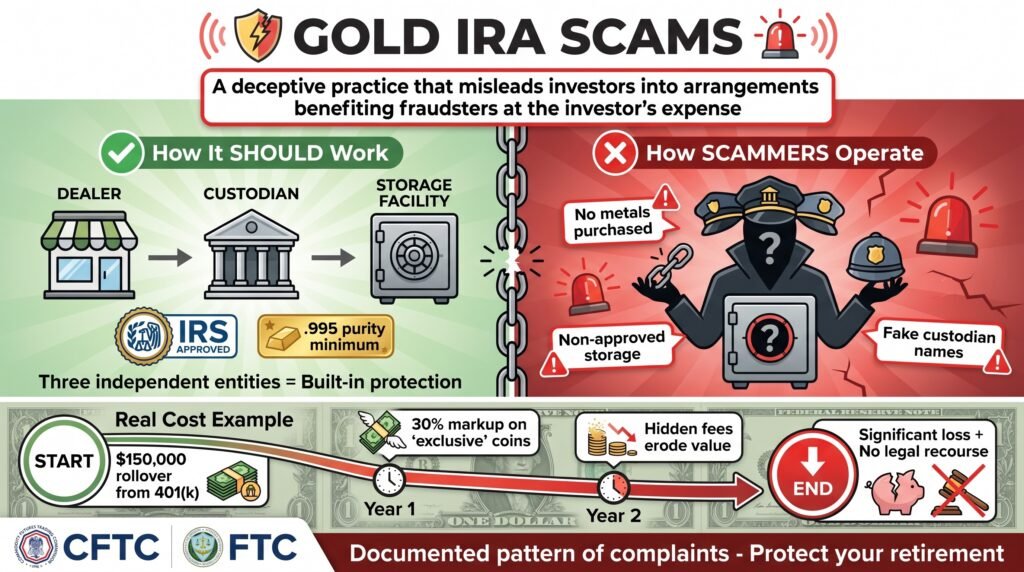

A self-directed IRA (SDIRA) is a type of individual retirement account that allows you to hold alternative assets, including physical gold, silver, platinum, and palladium, that standard IRAs won’t touch. The IRS permits this structure under specific rules, and it requires a specialized custodian who is approved to manage these asset types.

Unlike a brokerage IRA where the custodian controls your investment options, an SDIRA puts the investment decisions in your hands, within IRS guidelines. That means you choose which IRS-approved metals to buy, and those metals are stored in an IRS-approved depository, not your home.

- Holds physical gold, silver, platinum, and palladium

- Requires an IRS-approved custodian to manage the account

- Metals must be stored at an approved third-party depository

- Follows all traditional IRA contribution and distribution rules

TSP funds can be rolled into this structure tax-free via a direct rollover.

TSP Rollover vs. TSP Transfer: The Difference Matters

The terms “rollover” and “transfer” get used interchangeably, but they describe two different processes with very different tax consequences. Understanding the distinction before you move a single dollar out of your TSP can save you from an unexpected tax bill.

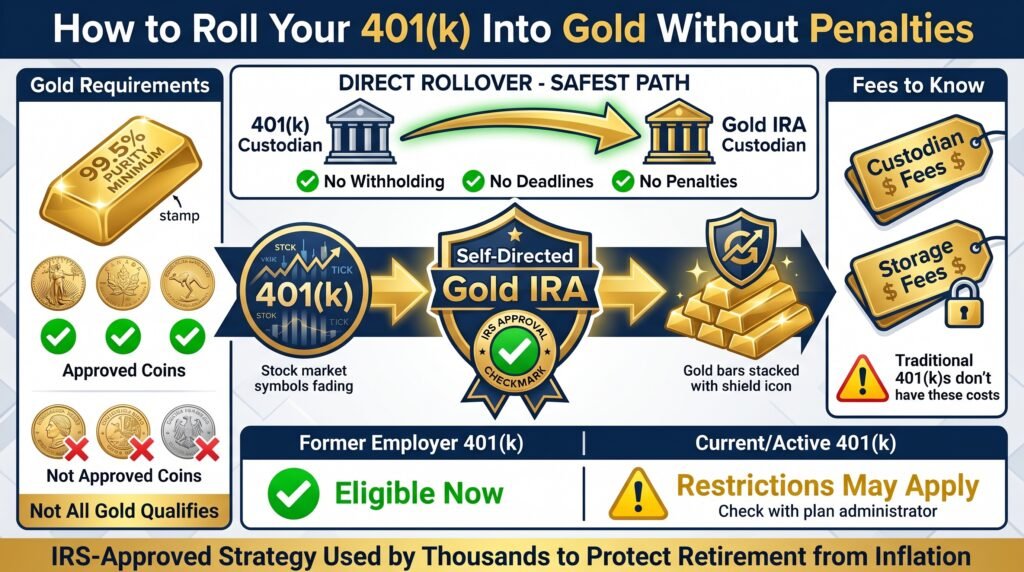

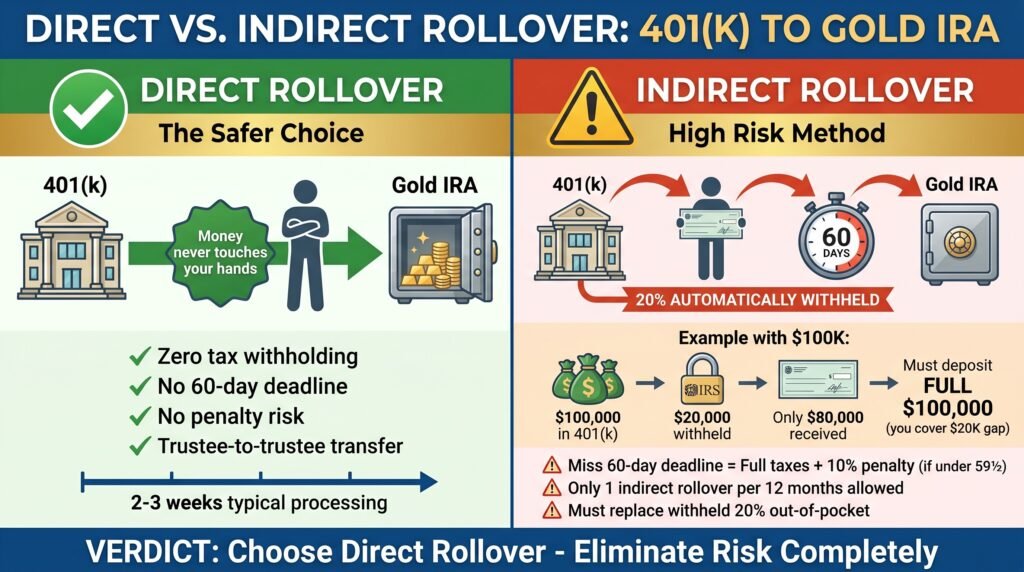

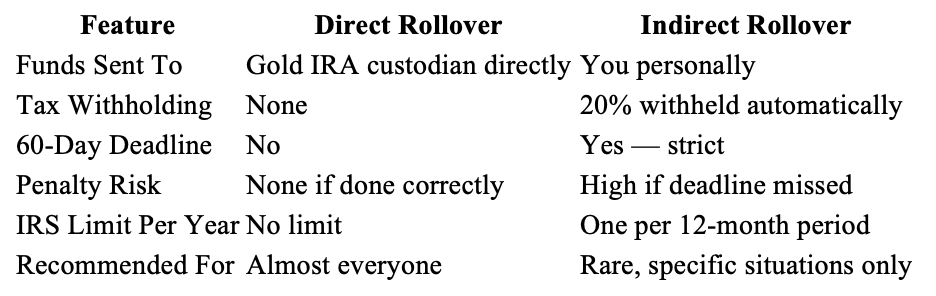

Direct Rollover: The Safest Way to Move TSP Funds

In a direct rollover, your TSP funds move directly from the TSP to your new Gold IRA custodian; you never touch the money. Because the funds go institution to institution, the IRS does not treat this as a taxable distribution. No withholding, no penalties, no 60-day clock. This is the method most Gold IRA companies will recommend, and for good reason.

The paperwork involved is straightforward. You’ll work with your Gold IRA custodian to complete the transfer request, and the custodian coordinates with the TSP on your behalf. The entire process typically takes up to two weeks from initiation to when your Gold IRA is funded and ready for metal purchases.

Indirect Rollover: The 60-Day Rule and Tax Risks

An indirect rollover means the TSP sends the funds directly to you, and you then have 60 days to deposit them into your Gold IRA. The problem is that the TSP is required to withhold 20% for federal income tax the moment it cuts that check. To complete a full rollover and avoid taxes and penalties, you must deposit 100% of the original amount, including the 20% that was withheld, into your new account within 60 days. That means coming up with the withheld portion out of pocket.

Miss the 60-day window and the entire distribution becomes taxable income for that year, plus a 10% early withdrawal penalty if you’re under age 59½. The indirect rollover route is rarely worth the risk when a direct rollover is available.

How to Convert Your TSP to a Gold IRA in 5 Steps

The process is more straightforward than most federal employees expect. Here’s exactly how it works from start to finish.

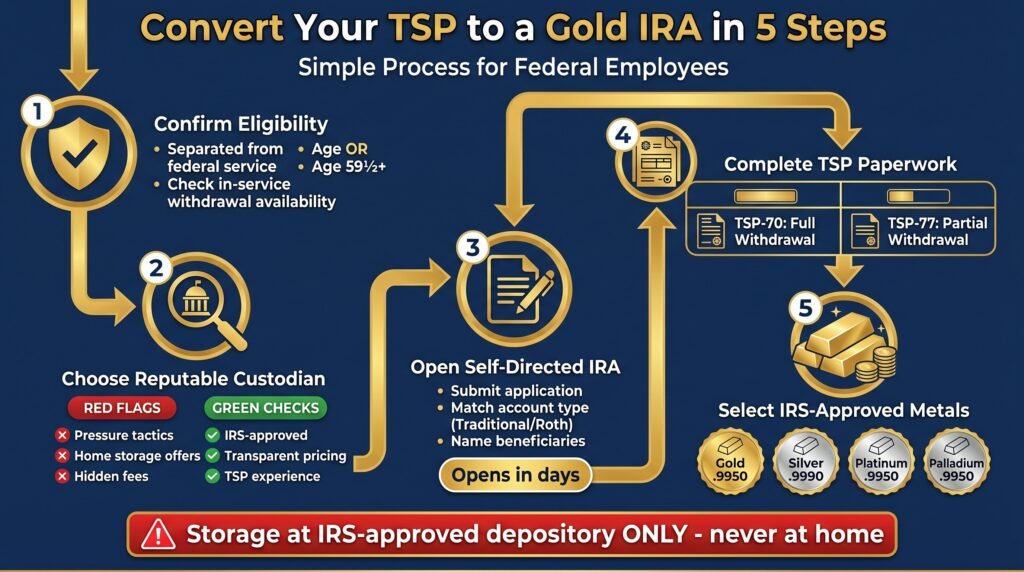

1. Confirm Your Eligibility to Withdraw From the TSP

Before anything else, verify that you meet the eligibility requirements. You must have separated from federal service or be at or above age 59½. If you’re still employed and under 59½, check whether your agency allows in-service withdrawals; these are limited and not always available.

2. Choose a Reputable Gold IRA Custodian

This is the most important decision in the entire process. Your Gold IRA custodian is the IRS-approved entity that will hold your account, coordinate the transfer, and facilitate metal purchases. Look for custodians with verifiable track records, transparent fee structures, and experience specifically working with federal employees on TSP rollovers.

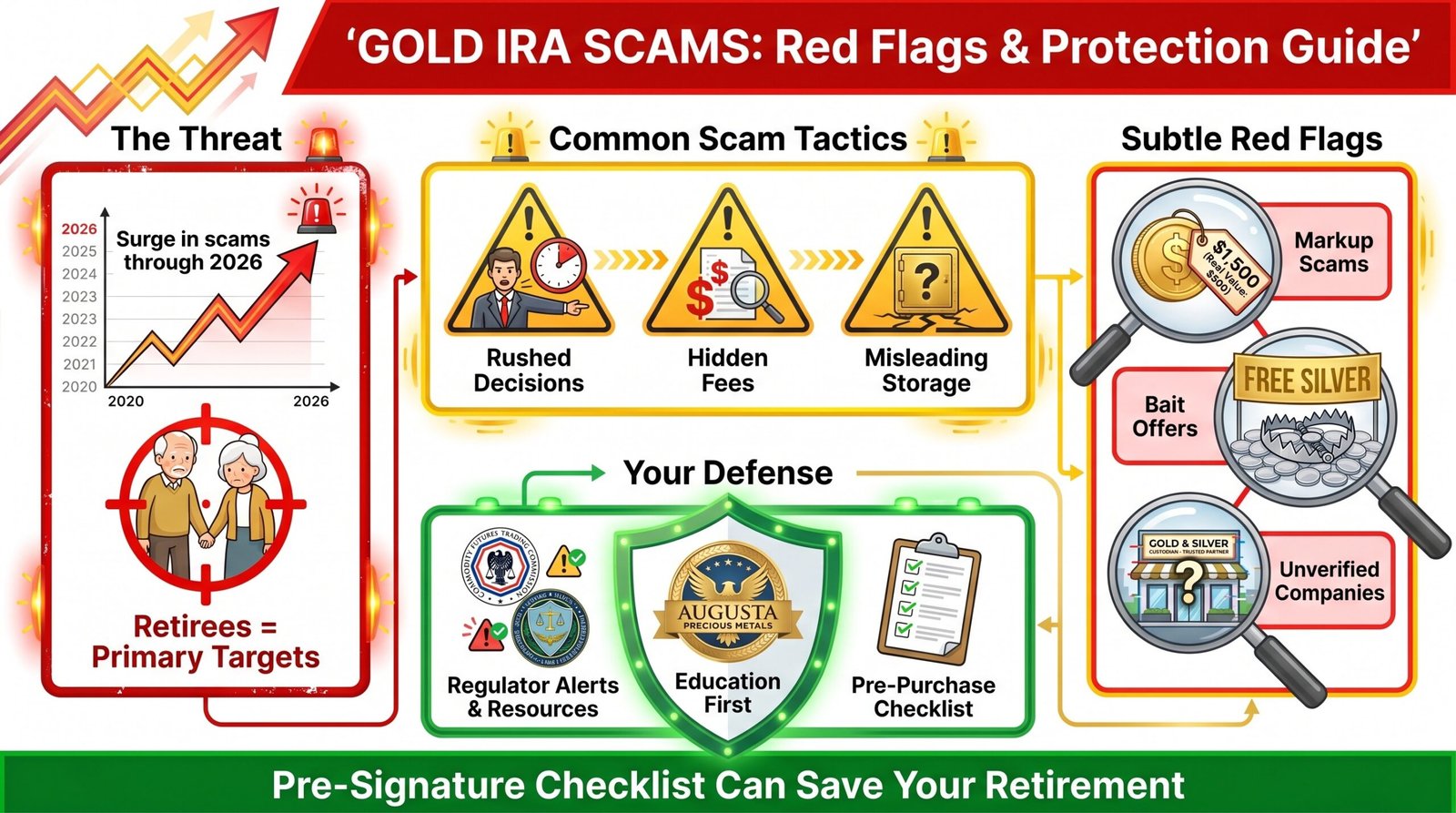

Be cautious of any company that pressures you to act fast, pushes numismatic or collectible coins with inflated markups, or is vague about storage arrangements and fees. Legitimate custodians never need to rush you. Avoid companies that suggest storing your Gold IRA metals at home; home storage of IRA-owned gold is not IRS-compliant and can result in full account disqualification.

Augusta Precious Metals is a leading and established gold IRA company that helps investors navigate the Gold IRA process, providing a combination of an ethics-centered approach to empower the customer, the best prices, superb customer service, and expert educational resources.

Click the banner below to visit Augusta’s official site and receive a free gold IRA company integrity checklist. Fill out their short form to get started.

3. Open Your Self-Directed IRA Account

Once you’ve selected a company, you’ll complete their account application to establish the self-directed IRA. This includes providing identification, selecting a traditional gold IRA structure that matches your TSP account type, and designating beneficiaries. Most custodians can get an account opened within a few business days.

4. Complete Form TSP-70 or TSP-77 to Initiate the Rollover

This is where the official TSP paperwork comes in. Form TSP-70 is used for a full withdrawal of your TSP balance, while Form TSP-77 covers partial withdrawals. Your Gold IRA custodian will typically help you complete these forms correctly; an error here can delay the transfer or trigger unintended tax consequences.

5. Select and Purchase IRS-Approved Precious Metals

With your Gold IRA funded, you can now direct your custodian to purchase IRS-approved precious metals on your behalf. You don’t physically buy the gold yourself; you instruct your custodian which metals to acquire, and they execute the purchase and arrange for storage at an approved depository. Your options go beyond just gold and include silver, platinum, and palladium, all subject to IRS purity requirements.

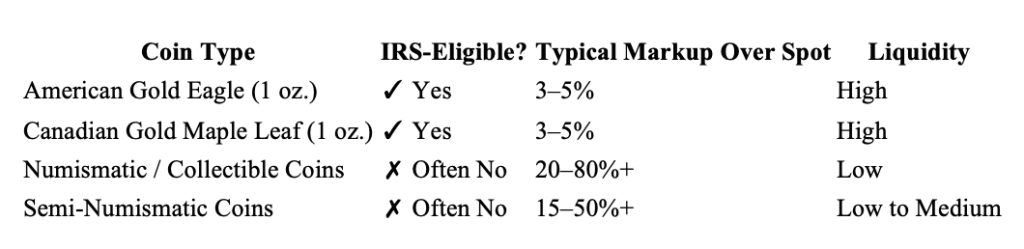

- Gold bullion bars and coins meeting .9950 minimum purity

- Silver bullion bars and coins meeting .9990 minimum purity

- Platinum and palladium products meeting .9950 minimum purity

- IRS-approved coins such as the American Gold Eagle and Canadian Gold Maple Leaf

- Storage arranged at an IRS-approved depository, not at home

You are not required to invest your entire rollover into gold. Many federal employees use this stage to build a diversified mix of metals based on their risk tolerance and retirement timeline.

Once the metals are purchased and transferred to the depository, your Gold IRA is fully operational. From this point forward, the account functions like any other traditional IRA for tax and distribution purposes.

Costs Involved in a TSP to Gold IRA Transfer

A Gold IRA is not a free account to maintain. Unlike a TSP, which has some of the lowest administrative fees of any retirement plan in the country, a Gold IRA involves multiple cost layers that you need to understand before committing.

The good news is that fee structures vary significantly between providers, and some companies offer zero-fee arrangements specifically designed for federal employees making TSP rollovers. Comparing total cost of ownership, not just the setup fee, is essential before choosing a custodian.

Setup Fees, Annual Maintenance, and Storage Fees

Most Gold IRA custodians charge a one-time account setup fee ranging from $50 to $150. On top of that, there’s typically an annual maintenance fee between $75 and $300 per year depending on the provider. The third cost layer, and often the largest, is the storage fee charged by the depository holding your physical metals.

Segregated storage (where your metals are stored separately from other clients’ holdings) costs more than commingled storage, typically ranging from $100 to $150 per year or a small percentage of your account’s total value.

Zero-Fee Gold IRA Options for Federal Employees

Some Gold IRA companies offer fee waivers for government workers rolling over TSP funds, covering setup costs, annual maintenance, and sometimes even the first year of storage fees. These offers are worth investigating closely; read the terms to confirm what’s included and for how long, since some waivers only apply for the first year before standard fees resume.

Learn if your TSP account qualifies for certain fee waivers. Click the banner below to visit Augusta’s official site, receive a free gold IRA company guide, and get the process started. Fill out their short form to get started.

Tax Implications of Rolling Over a TSP to a Gold IRA

Tax treatment during a TSP to Gold IRA transfer depends entirely on how the rollover is executed and which account types are involved. Get this part right, and the transfer is completely tax-neutral. Get it wrong, and you could face an unexpected tax bill plus penalties.

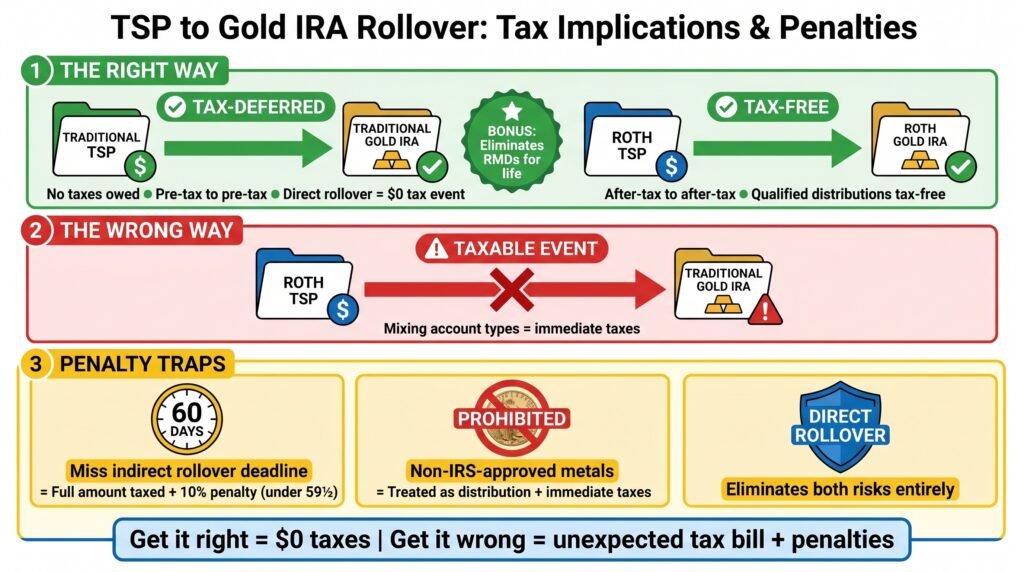

Traditional TSP to Traditional Gold IRA: Tax-Deferred Transfer

When you roll a traditional TSP directly into a traditional Gold IRA, the transfer is completely tax-deferred, meaning no taxes are owed at the time of the transfer.

Both accounts operate on the same pre-tax basis: contributions went in before taxes, growth compounds tax-deferred, and distributions in retirement are taxed as ordinary income. As long as you execute a direct rollover, the IRS sees no taxable event, and your full balance moves into the Gold IRA intact.

Roth TSP to Roth Gold IRA: What Changes

A Roth TSP rollover to a Roth Gold IRA follows the same tax-free logic; contributions were already made with after-tax dollars, so qualified distributions in retirement remain tax-free. The key is making sure you’re rolling Roth to Roth. Mixing account types, such as rolling a Roth TSP into a traditional Gold IRA, creates a taxable event that most federal employees want to avoid entirely.

One important detail: Roth IRAs do not have required minimum distributions (RMDs) during the account holder’s lifetime, while the Roth TSP does. Rolling a Roth TSP into a Roth Gold IRA can actually eliminate your RMD obligation on those funds, which is a meaningful long-term tax planning advantage worth discussing with a financial advisor.

Penalties to Avoid During the Rollover Process

The two biggest penalty traps in a TSP to Gold IRA transfer are missing the 60-day window on an indirect rollover and rolling funds into a non-qualifying account type. A failed rollover results in the full distributed amount being treated as taxable income for that year, plus a 10% early withdrawal penalty if you’re under age 59½.

Using a direct rollover eliminates both risks. Additionally, purchasing non-IRS-approved metals inside your Gold IRA, such as collectible coins, is treated as a distribution in the year of purchase, triggering immediate taxes on the full value of those assets.

Your TSP Retirement Savings Deserve More Than One Option

The TSP is one of the best employer-sponsored retirement plans available, low fees, consistent fund options, and decades of reliable performance for federal employees. But having all your retirement assets in a single plan with no exposure to hard assets is a concentration risk, especially during periods of inflation, dollar weakness, or prolonged market downturns. A TSP to Gold IRA transfer isn’t about abandoning your TSP; it’s about building a more complete retirement strategy that the TSP alone was never designed to provide.

Physical gold has preserved wealth through currency crises, recessions, and geopolitical instability for thousands of years. Adding even a measured allocation through a properly structured Gold IRA can give federal employees a layer of portfolio protection that no TSP fund- not the G Fund, not the C Fund- is built to deliver. You’ve spent a career building your retirement security. Protecting it with more than one tool is simply smart planning. Get the process started of rolling over your TSP account today.

Click the banner below to visit Augusta’s official site and receive a free gold IRA company guide. Fill out their short form to get started.

Frequently Asked Questions

Below are the most common questions federal employees ask when researching a TSP to Gold IRA transfer. The answers are based on current IRS guidelines and TSP regulations.

Can I Roll Over My TSP to a Gold IRA While Still Employed?

Generally, no, unless you are age 59½ or older. Federal employees under 59½ who are still actively employed cannot initiate a full TSP rollover to an external IRA. Once you reach 59½, an in-service withdrawal becomes available, giving you the ability to roll over TSP funds into a Gold IRA without separating from service. If you’ve already separated from federal employment at any age, you are eligible to initiate the rollover regardless of age, though the 10% early withdrawal penalty may apply if you’re under 59½ and use an indirect rollover incorrectly.

How Long Does a TSP to Gold IRA Transfer Take?

The typical timeline from initiating the paperwork to having your Gold IRA fully funded is up to two weeks. The exact duration depends on how quickly your forms are processed by the TSP and how efficiently your Gold IRA custodian handles the incoming transfer.

Delays can occur if forms are completed incorrectly or if additional verification is required by the TSP. Working with a Gold IRA company that has direct experience handling TSP transfers reduces the chance of paperwork errors that slow the process down.

Once the metals are purchased, they are transferred directly to your designated IRS-approved depository. You will receive confirmation of both the purchase and the storage arrangement from your custodian.

Do I Have to Roll Over My Entire TSP Balance?

No. Partial rollovers are fully permitted. Using Form TSP-77, you can specify exactly how much of your TSP balance you want to transfer to your Gold IRA while leaving the remainder in your TSP funds. This gives federal employees the flexibility to diversify into gold without fully exiting the TSP, a strategy that makes practical sense for those who want to maintain exposure to the C Fund or other TSP options while adding a hard asset allocation.

Is Physical Gold Stored at Home Allowed in a Gold IRA?

No, and this is a critical point. IRS rules require that all physical metals held inside an IRA be stored at an IRS-approved depository. Taking personal possession of Gold IRA metals, including storing them at home or in a personal safe, is treated by the IRS as a distribution. That means the full value of the metals becomes taxable income in the year you take possession, plus the 10% early withdrawal penalty if you’re under 59½. Any company suggesting home storage as a valid Gold IRA strategy is either misinformed or deliberately misleading you.

Will I Owe Taxes When I Move My TSP to a Gold IRA?

No taxes are owed when a TSP is rolled over directly into a Gold IRA of the same account type, traditional to traditional, or Roth to Roth. A direct rollover is a trustee-to-trustee transfer where the funds never pass through your hands, so the IRS does not classify it as a taxable distribution.

Taxes only become a factor if you choose an indirect rollover, miss the 60-day reinvestment window, roll funds into the wrong account type, or purchase non-IRS-approved assets inside your Gold IRA. All of these scenarios are avoidable with proper planning and the right custodian guiding the process.

If you have a mix of traditional and Roth TSP funds, work with your Gold IRA provider to ensure each portion rolls into the correct corresponding account type. Mismatching account types during a rollover creates a taxable event that cannot be reversed after the fact.

For federal employees ready to explore diversifying their retirement with physical precious metals, Augusta Precious Metals provides step-by-step guidance on TSP rollovers, custodian selection, and IRS-compliant precious metals investing tailored specifically for government workers and uniformed service members.

Investment Minimums – Personal Considerations

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, life-long customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group are trustworthy companies that provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Sources:

Gold IRA Rules and Regulations: LendEDU

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Investments in collectibles in individually directed qualified plan accounts: IRS.gov: Retirement plans FAQs regarding IRAs: IRS.gov

Transform Your TSP into a Secure Gold Investment – FedPilot

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance