Quick Summary

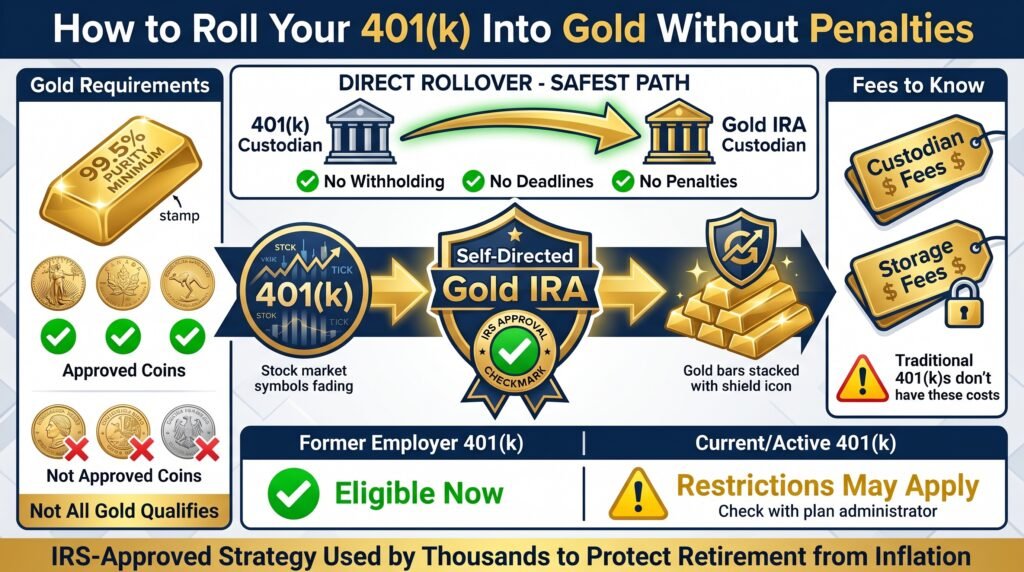

- Rolling your 401(k) into gold is possible without taxes or penalties, but only if you follow the IRS-approved rollover process correctly, starting with a self-directed Gold IRA.

- A direct rollover is the safest method: funds move directly from your 401(k) custodians to your Gold IRA custodian, with no withholding, no deadlines, and no risk of accidental penalties.

- Not all gold qualifies: the IRS requires a minimum purity of 99.5% for gold bars and only approves specific coins, so knowing what you can actually hold matters before you invest.

- There are fees involved: Gold IRAs come with custodian and storage fees that traditional 401(k) accounts do not, and understanding these upfront protects your long-term returns.

- Keep reading to find out which type of 401(k) you have and whether you can roll it over right now, because the answer is different depending on whether your plan is active or from a previous employer.

Your 401(k) doesn’t have to stay locked in the stock market while inflation quietly chips away at its value; rolling it into gold is a real, IRS-approved strategy that thousands of Americans use to protect their retirement.

A gold IRA rollover from Augusta Precious Metals and similar providers has become one of the most searched retirement strategies in recent years, and for good reason. When paper assets lose value, physical gold has historically held its ground. This guide cuts through the noise and gives you exactly what you need to make the move correctly, without triggering taxes or penalties.

Table of Contents

- Quick Summary

- What Is a Gold IRA and Why It Matters for Your Retirement?

- Direct Rollover vs. Indirect Rollover: Which One Should You Use

- How to Roll Your 401(k) Into Gold in 4 Steps

- Your 401(k) Can Work Harder for Your Retirement in Gold

- Frequently Asked Questions

What Is a Gold IRA and Why It Matters for Your Retirement?

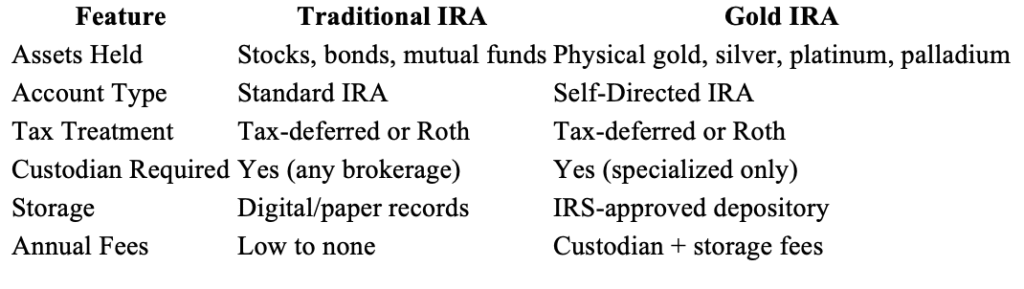

A Gold IRA is a self-directed individual retirement account that holds physical precious metals instead of stocks, bonds, or mutual funds. It operates under the same IRS rules as a traditional IRA, meaning the same contribution limits, the same tax treatment, and the same required minimum distributions apply. The critical difference is what sits inside the account.

How a Gold IRA Differs from a Traditional IRA

A traditional IRA is managed by a brokerage that offers a preset menu of paper investments. A Gold IRA, on the other hand, requires a self-directed IRA custodian, a specialized financial institution approved by the IRS to hold alternative assets including physical precious metals. You do not manage the gold yourself. The custodian handles all compliance, reporting, and storage logistics on your behalf.

This structure matters because it’s what makes a Gold IRA legally distinct from simply buying gold coins at a dealer. Inside a Gold IRA, your metals are held in a secure, IRS-approved depository, and the account retains all the tax advantages you’ve already built up in your 401(k).

Why Gold Has Been a Reliable Store of Wealth

Most beginning gold investors may not know that gold has functioned as a store of value for over 5,000 years. Unlike paper currency, it cannot be printed into devaluation.

During periods of high inflation, currency crises, and stock market downturns, gold has consistently preserved purchasing power in ways that bonds and cash equivalents often cannot. That track record is exactly why it remains a core diversification tool for serious retirement planners.

The Role of a Custodian in a Gold IRA

Every Gold IRA must have an IRS-approved custodian. This is non-negotiable. The custodian is responsible for holding the account, executing purchases of approved metals, arranging insured storage at an approved depository, and filing the necessary IRS reports each year.

Choosing the right custodian is one of the most important decisions in the entire rollover process. A custodian that specializes in precious metals IRAs will know exactly which gold products are IRS-compliant, which depositories meet federal standards, and how to execute a rollover from your specific 401(k) plan without triggering a taxable event.

Not every financial institution offers self-directed IRA custody. Banks, standard brokerages, and most 401(k) plan administrators cannot serve as Gold IRA custodians. You will need to open a new account specifically designed for this purpose before initiating any transfer of funds.

Quick Reference: Traditional IRA vs. Gold IRA

Augusta Precious Metals is an established precious metals provider that helps investors navigate the Gold IRA process, offering IRS-approved coins and bars, along with educational resources for beginners just getting started with precious metals retirement planning.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get started.

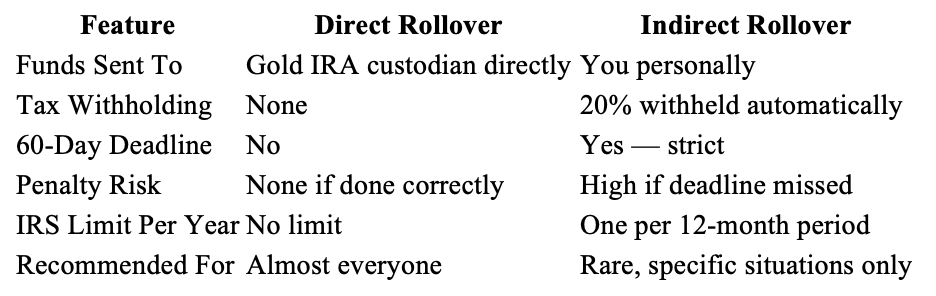

Direct Rollover vs. Indirect Rollover: Which One Should You Use

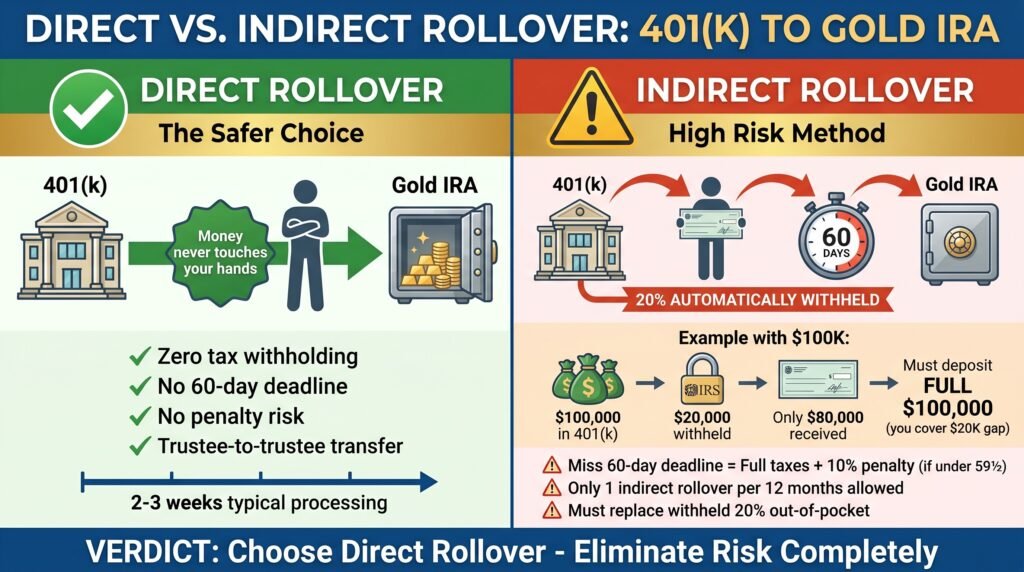

When moving your 401(k) into a Gold IRA, you have two options: a direct rollover or an indirect rollover. They both get your money to the same destination, but the risks involved are not even close to equal.

For most people, the answer is simple — use the direct rollover. It eliminates risk, removes the pressure of deadlines, and ensures not a single dollar is withheld for taxes during the transfer.

How a Direct Rollover Works and Why It Is the Safer Option

In a direct rollover, your 401(k) plan administrator transfers your funds directly to your new Gold IRA custodian. The money never passes through your hands. There is no IRS withholding, no 60-day countdown, and no chance of accidentally triggering a taxable distribution. This is the method the IRS refers to as a trustee-to-trustee transfer, and it is the cleanest way to move retirement assets.

The process typically involves completing paperwork with both your 401(k) plan administrator and your new Gold IRA custodian. Once both sides confirm the transfer, the funds move, sometimes within a few business days, sometimes in two to three weeks depending on your existing plan’s processing time.

The 60-Day Rule for Indirect Rollovers and the Risks Involved

An indirect rollover works differently. Your 401(k) plan administrator sends the funds directly to you, and you then have exactly 60 days to deposit the full amount into your new Gold IRA. Miss that deadline by even one day, and the IRS treats the entire distribution as ordinary income, taxable in full, plus a 10% early withdrawal penalty if you are under age 59½.

How Tax Withholding Can Catch You Off Guard with an Indirect Rollover

The Hidden Withholding Problem: When a 401(k) plan distributes funds directly to you in an indirect rollover, the IRS requires your plan administrator to withhold 20% for federal taxes automatically. That means if you have $100,000 in your 401(k), you only receive $80,000. To complete a full rollover without penalty, you must deposit the entire $100,000 into your Gold IRA within 60 days, which means you will need to pay the missing $20,000 out of pocket. You do get that 20% back as a tax refund later, but only after filing your return.

This withholding trap catches a surprising number of people off guard. Many assume they can simply deposit the check they receive and call it complete, only to find they owe taxes on the withheld portion because they didn’t cover the shortfall in time.

The 60-day indirect rollover also carries an additional restriction: the IRS only allows one indirect rollover per 12-month period across all your IRA accounts. Exceed that limit, and the second transfer is treated as a fully taxable distribution regardless of timing.

Given all these risks, the indirect rollover rarely makes sense for someone moving a 401(k) into a Gold IRA. Unless you have a specific reason to take possession of the funds temporarily, the direct rollover protects you completely.

How to Roll Your 401(k) Into Gold in 4 Steps

The rollover process is more straightforward than most people expect. Once you understand which type of account you have and confirm your eligibility, the actual execution comes down to four clear steps. Following each one in order is what keeps the process tax-free and penalty-free from start to finish.

1. Confirm Your 401(k) Rollover Eligibility

Before anything else, you need to confirm that your specific 401(k) plan allows a rollover and under what conditions. For old employer plans, eligibility is almost always automatic. For active employer plans, you need to check whether your plan includes an in-service distribution provision. Call your plan administrator directly and ask two specific questions: “Does my plan allow in-service distributions?” and “What documentation is required to initiate a rollover to an outside IRA?”

Get the answers in writing if possible. Plan administrators are required to provide you with a Summary Plan Description that outlines all rollover rules, and you are entitled to request one at any time. This step takes a day or two but prevents costly surprises later in the process.

2. Open a Self-Directed Gold IRA With an Approved Custodian

Your Gold IRA account must be open and ready to receive funds before you initiate the transfer from your 401(k). Choose a gold IRA company that has a clear, transparent fee structure. During the account opening process, you will complete identity verification and receive the account details your 401(k) plan administrator will need to send the funds. This step typically takes two to five business days once your application is submitted.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get the process started.

3. Initiate the Rollover and Transfer Your Funds

Once your Gold IRA account is open, contact your 401(k) plan administrator and formally request a direct rollover. Provide them with your new Gold IRA custodian‘s account information, including the receiving institution’s name, address, account number, and any wire transfer instructions. The administrator will process the request and send the funds directly to your new custodian — no check passes through your hands, no taxes are withheld, and no deadline clock starts ticking.

Processing times vary. Some 401(k) plans move quickly and complete the transfer in under a week. Others, particularly older plans or those with less modern infrastructure, can take three to four weeks. Your Gold IRA custodian will notify you when the funds arrive and are ready to be invested.

Direct Rollover vs. Indirect Rollover: At a Glance

Once your custodian confirms the funds have arrived, you will work with them to select which IRS-approved gold products to purchase. This is where the physical asset acquisition actually happens, and it is where purity standards and product eligibility become critically important.

Keep records of every step of this process. Retain the rollover request confirmation from your 401(k) administrators, any wire transfer receipts, and the purchase confirmations from your Gold IRA custodian. These documents are your evidence that the rollover was completed correctly if the IRS ever has questions about the transaction.

4. Select and Purchase IRS-Approved Gold for Your IRA

After the funds arrive in your Gold IRA, your custodian will guide you through selecting eligible gold products. This is not as open-ended as buying gold from a dealer; the IRS has a strict list of approved coins and bars that can legally be held inside a retirement account. Your custodian will only offer products that qualify, which removes most of the guesswork from this step.

Once you select your preferred gold holdings, the custodian purchases them on your behalf and arranges for secure delivery to an IRS-approved depository. You will receive confirmation of the purchase and documentation showing the specific metals held in your account, their weight, purity, and current valuation. From that point forward, your Gold IRA is fully funded and actively holding physical precious metals on your behalf.

If you are ready to get started with one of the most reputable gold IRA companies for lifelong customer service, prices, and education, click the banner below to visit Augusta Precious Metals’ official site. Access their free gold IRA guide by filling out their short contact form.

There are many other IRS rules, such as withdrawals, approved depositories, and more, that are worth reviewing once your gold IRA rollover is established. See the full guide here.

Find out whether gold IRAs are a good choice for your retirement needs. Access our Gold IRA and Inflation-Retirement Calculators. Perform real-time calculations as you read our reviews. See the buttons below to access these calculators and start protecting your wealth today.

Your 401(k) Can Work Harder for Your Retirement in Gold

If your retirement savings are sitting in a standard 401(k) exposed entirely to market volatility, you already understand the risk; you have probably watched your balance drop during downturns and wondered whether there is a better way to protect what you have built. Rolling part or all of that 401(k) into a Gold IRA is not a radical move.

It is a deliberate, IRS-compliant strategy to hold a portion of your wealth in an asset that has preserved value across centuries of economic upheaval. The process is straightforward, the protections are real, and when done correctly with a direct rollover, it costs nothing in taxes or penalties to make the move. Augusta Precious Metals’ step-by-step rollover process is one resource worth reviewing as you evaluate your options and choose a custodian that fits your retirement goals.

Click the banner below to receive a free gold IRA company integrity checklist from Augusta Precious Metals. Fill out their short contact form to get started.

Investment Minimums – Personal Considerations

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, life-long customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Frequently Asked Questions

Rolling a 401(k) into a Gold IRA raises a lot of specific questions, especially around taxes, timing, and IRS rules. Here are the most common ones answered clearly so you can move forward with confidence.

Can I Roll My Entire 401(k) Into a Gold IRA Without Paying Taxes?

Yes, you can roll your entire 401(k) balance into a Gold IRA without paying taxes, provided you use a direct rollover. In a direct rollover, your funds move from your 401(k) plan administrator directly to your Gold IRA custodian without ever passing through your hands. No taxes are withheld, no taxable event is triggered, and the full balance transfers intact.

The tax treatment of the Gold IRA going forward depends on which type you open. A Traditional Gold IRA mirrors a traditional 401(k) — contributions and growth are tax-deferred, and you pay ordinary income tax when you take distributions in retirement.

How Long Does a 401(k) to Gold IRA Rollover Take?

The timeline from initiating a rollover to having physical gold in your account typically runs between two and six weeks. Opening your Gold IRA account takes two to five business days. The fund transfer from your 401(k) plan administrator can take anywhere from a few days to three weeks depending on your plan’s internal processing speed and whether they require paper forms or accept electronic requests. Once the funds arrive at your Gold IRA custodian, purchasing the approved gold products and arranging depository delivery usually takes an additional two to five business days. Starting the process with all your paperwork organized shortens the timeline considerably.

What Happens if I Miss the 60-Day Deadline on an Indirect Rollover?

Missing the 60-day deadline on an indirect rollover is a costly mistake. The IRS treats the entire amount that was not deposited into a qualifying retirement account by day 60 as a taxable distribution. You owe ordinary income tax on that amount for the year it was distributed, and if you are under age 59½, you also owe a 10% early withdrawal penalty on top of the tax bill.

The IRS does allow for waivers in certain documented hardship situations, such as a serious illness, a natural disaster, or errors made by a financial institution, but these waivers are not automatic. You must formally request a waiver from the IRS and provide evidence of the qualifying circumstance. The safest way to avoid this scenario entirely is to use a direct rollover from the beginning, which eliminates the 60-day deadline completely.

Can I Hold Physical Gold at Home if It Is Purchased Through My Gold IRA?

No. Gold purchased through your Gold IRA must be stored at an IRS-approved depository, not in your home, not in a personal safe, and not in a safety deposit box that you control. The moment you take personal possession of gold that is legally owned by your IRA, the IRS considers that a distribution.

However, once you reach retirement age and begin taking distributions from your Gold IRA, you can choose to receive your distributions in the form of physical metal rather than cash. At that point, the gold is legally distributed to you and is no longer inside the IRA structure, meaning you can store it however you choose. Taking an in-kind distribution of physical gold is a legitimate retirement income strategy and one that some investors specifically plan for from the beginning of their Gold IRA journey.

Sources:

Gold IRA Rules and Regulations: LendEDU

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Investments in collectibles in individually directed qualified plan accounts: IRS.gov: Retirement plans FAQs regarding IRAs: IRS.gov

Leave a Reply