Quick Summary

Gold IRA demand is surging in 2026 due to persistent inflation, geopolitical uncertainty, and fully enacted SECURE Act 2.0 provisions prompting investors to rethink retirement strategy. A Gold IRA offers tax-advantaged exposure to physical gold, portfolio diversification, and protection against currency debasement, but choosing the right company is critical.

Look for IRS-authorized custodians, transparent fee structures, and strong third-party reviews. Only IRS-approved metals (99.5%+ purity) qualify, and your metals must be stored in an approved depository — never at home.

Top providers like Augusta Precious Metals, Birch Gold Group, and National Gold Group offer different minimums and strengths to fit your situation.

Table of Contents

- Quick Summary

- Why Has Gold IRA Rollover Demand Surged in 2026?

- How to Evaluate a Gold IRA Provider Before You Commit

- How to Execute a Gold IRA Rollover in 2026

- Which Gold Products Are Actually IRS-Approved

- FAQ

Why Has Gold IRA Rollover Demand Surged in 2026?

According to Gold Silver News’ 2026 research report, Gold IRA rollover activity has risen sharply this year, with demand for physical asset-backed retirement accounts accelerating at a pace not seen in recent cycles. This isn’t speculative momentum; it reflects a structural shift in how retirement investors are thinking about portfolio resilience and purchasing power preservation.

The macroeconomic environment driving this shift is layered. Persistent inflation concerns, ongoing geopolitical instability, and growing skepticism about the long-term stability of dollar-denominated paper assets have all contributed to a renewed interest in physical gold as a retirement allocation. Investors who watched equity-heavy portfolios absorb volatility in recent years are now actively seeking assets with lower correlation to stock market performance.

What makes 2026 particularly significant is that the structural retirement planning landscape has also changed. The SECURE Act 2.0 provisions now fully in effect, have prompted investors to reassess distribution timing, Roth conversion strategies, and legacy planning, all areas where a Gold IRA can play a meaningful role. The rules are clearer, the custodian infrastructure is more developed, and the investor education gap has narrowed considerably compared to five years ago.

- Inflation hedging: Physical gold has historically maintained purchasing power during inflationary periods, making it a logical allocation for long-duration retirement accounts.

- Portfolio diversification: Gold’s low correlation to equities and bonds reduces overall portfolio volatility when included as a strategic allocation.

- Tax-advantaged accumulation: Holding gold inside an IRA structure shelters gains from the 28% collectibles capital gains tax rate that applies to metals held in taxable accounts.

- Estate planning efficiency: Roth Gold IRAs in particular offer tax-free inheritance for beneficiaries, making them a powerful multi-generational wealth transfer tool.

- Currency debasement protection: Investors concerned about long-term dollar purchasing power view gold as a structural hedge against monetary policy risk.

The investors moving into Gold IRAs in 2026 aren’t chasing a trend; they’re making deliberate structural decisions about where they want their retirement wealth to sit over the next decade. That distinction matters, because it means the due diligence required goes beyond simply opening an account and buying the first approved coin on the list.

How to Evaluate a Gold IRA Provider Before You Commit

The surge in Gold IRA rollover activity in 2026 has attracted both reputable firms and predatory operators into the space. Choosing the wrong provider doesn’t just cost you in fees; it can expose your retirement savings to compliance failures, hidden markups on metals, and custodians who aren’t actually IRS-authorized. The evaluation process deserves as much attention as the rollover mechanics themselves.

A legitimate Gold IRA provider will be transparent about their fee structure from the first conversation. Setup fees, annual custodial fees, storage fees, and transaction fees should all be disclosed in writing before you sign anything. If a provider is vague about costs, pushes urgency, or leads with promises of guaranteed returns on gold, treat those as immediate disqualifying signals.

BBB, Trustpilot, and Google Reviews as Verification Tools

Start your vetting process with third-party review platforms. A strong Better Business Bureau (BBB) rating, ideally A or A+, combined with consistent positive reviews on Trustpilot and Google, gives you a multi-source picture of how a provider actually operates with real clients. Look specifically at how the company responds to negative reviews, not just the volume of positive ones. A provider that engages professionally with complaints signals institutional accountability.

Beyond reviews, verify that the custodian is registered with the appropriate regulatory bodies. Self-directed IRA custodians are typically regulated by state banking authorities or the IRS, and their approval status should be independently verifiable. Never rely solely on a provider’s own claims about their compliance status.

Red Flags to Watch for in Provider Selection

Some of the most damaging Gold IRA mistakes investors make in 2026 start with provider selection, not the rollover process itself. Watch for these specific warning signs before you hand over your retirement funds:

- Pressure tactics pushing you to act before you’ve reviewed all documentation

- Promotions of home storage Gold IRAs as a legal, IRS-compliant option

- Vague or verbal-only fee disclosures with no written schedule provided

- No clear disclosure of which depository your metals will be stored in

- Metals offered at prices significantly above spot price without explanation

- No verifiable BBB, Trustpilot, or Google review presence

- Claims of guaranteed returns or recession-proof performance

Any provider worth working with will actively encourage you to take your time, ask questions, and compare options. The ones who push back on that approach are telling you everything you need to know.

Choosing a Reputable Gold IRA Company

Your Gold IRA company is not the same as your custodian; it is the dealer that guides you through the process, helps you select IRS-approved metals, and connects you with a custodian and depository. Choosing the right one upfront saves you from costly mistakes later.

Look for companies with long operating histories, transparent fee structures, and strong third-party reviews. A company that pressures you into making a quick decision or upsells you into rare or collectible coins is a red flag; collectibles are not IRS-approved for Gold IRAs and can disqualify your account.

Augusta Precious Metals is one example of an established precious metals provider that helps investors navigate the Gold IRA process, offering IRS-approved coins and bars along with educational resources for beginners who are just getting started with precious metals retirement planning.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get started.

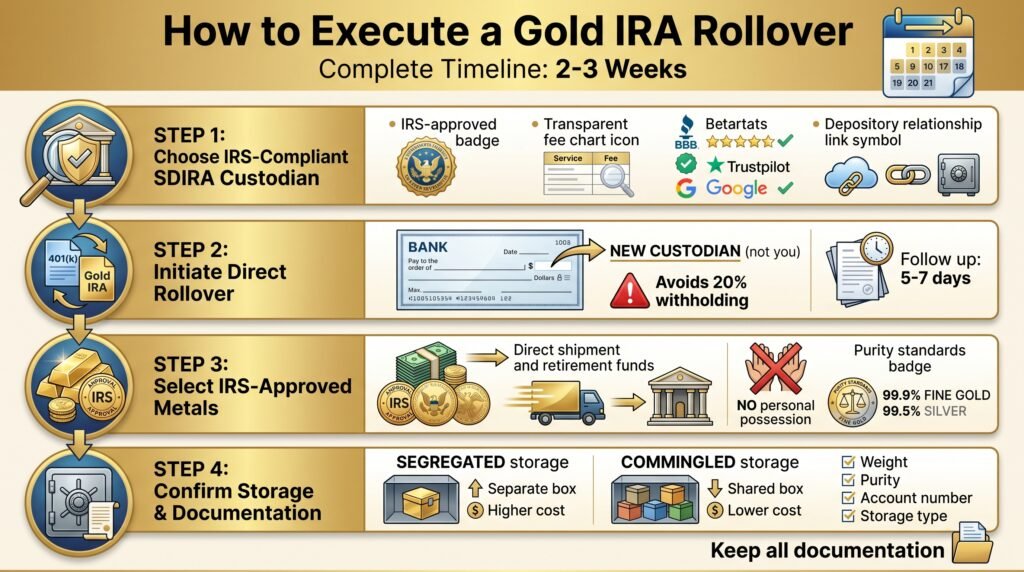

How to Execute a Gold IRA Rollover in 2026

The actual mechanics of a Gold IRA rollover are straightforward when you follow the right sequence. Most rollovers from a 401(k) to a Gold IRA take approximately 2 to 3 weeks from initiation to completion, longer than a standard IRA-to-IRA transfer because the 401(k) plan administrator, your employer, and the new custodian all need to coordinate. Knowing each step in advance prevents delays and costly mistakes.

1. Choose an IRS-Compliant Self-Directed IRA Custodian

Not every IRA custodian supports physical precious metals. You need a self-directed IRA (SDIRA) custodian that is specifically authorized to hold alternative assets, including gold bullion.

Verify that your chosen custodian is IRS-approved, maintains transparent fee structures, and has established relationships with IRS-compliant depositories. Review their ratings on the Better Business Bureau (BBB), Trustpilot, and Google before committing.

2. Initiate a Direct Rollover from Your 401(k) Administrator

Contact your current 401(k) plan administrator and request a direct rollover to your new Gold IRA custodian. Specifically request that the distribution check be made payable to your new custodian, not to you personally. This single instruction is what prevents the mandatory 20% federal withholding from reducing your transfer amount.

Your new custodian will typically provide a rollover request letter or transfer form that you submit to your 401(k) administrators to initiate the process. Keep copies of every document submitted and follow up within 5 to 7 business days if you have not received confirmation of the transfer in progress.

3. Select IRS-Approved Metals and an Approved Depository

Once funds arrive in your new self-directed IRA, you direct your custodian to purchase specific IRS-approved metals on your behalf. Your custodian executes the purchase and arranges for direct shipment to an approved depository; you never take physical possession of the metals during this stage.

Confirm the specific coins or bars you’re purchasing meet IRS purity standards before the order is placed, and request written confirmation of depository assignment and storage allocation once the transaction clears.

4. Confirm Regulated Storage and Receive Account Documentation

Once your metals have been purchased and delivered to the approved depository, request written confirmation from both your custodian and the depository facility, this documentation should include the specific metals held, their weight and purity, your account number, and the storage allocation type, either segregated (your metals stored separately from other clients’ holdings) or commingled (stored together with other clients’ equivalent holdings). Segregated storage costs more but provides cleaner asset identification, which matters significantly at the time of distribution.

Which Gold Products Are Actually IRS-Approved

Not all gold qualifies for an IRA. The IRS has strict purity and sourcing requirements, and purchasing a non-compliant product inside your IRA can result in the entire account being treated as a taxable distribution. The standard purity requirement for gold bullion is 99.5% fineness (0.995) or higher.

There is one notable exception to the 99.5% rule: the American Gold Eagle coin, which is only 91.67% pure (22 karat) but is specifically authorized by the IRS as an approved IRA investment due to its status as U.S. legal tender. Every other coin must meet the 99.5% threshold.

24K Coins: American Buffalo and Canadian Maple Leaf

The American Gold Buffalo (24K, 99.99% pure) and the Canadian Gold Maple Leaf (24K, 99.99% pure) are both fully IRS-compliant for Gold IRA inclusion in 2026. These are among the most widely held coins in self-directed precious metals IRAs because of their recognized purity, global liquidity, and broad custodian acceptance. The South African Krugerrand, by contrast, does not meet IRS standards and is explicitly prohibited.

Approved Bars from Accredited Refiners Like PAMP Suisse

Gold bars are eligible when they meet the 99.5% purity standard and are produced by an NYMEX- or COMEX-approved refiner or assayer, or a national government mint. PAMP Suisse bars are among the most widely accepted in the industry.

Custodians typically maintain resources listing IRS-compliant refiners and products; always verify your specific bar or coin with your custodian before purchasing inside the account.

What Gets Disqualified and Why

The most common disqualifying factors come down to purity and sourcing. Gold that falls below the 99.5% fineness threshold, with the sole exception of the American Gold Eagle, cannot be held in an IRA. Collectible coins, numismatic coins, and gold jewelry are explicitly prohibited regardless of their market value or gold content. The IRS draws a hard line between investment-grade bullion and collectibles.

Purchasing a disqualified asset inside your Gold IRA doesn’t just result in that single item being removed, the IRS can treat the entire transaction as a taxable distribution. That means the full value of the purchase could be added to your taxable income for that year, plus the 10% early withdrawal penalty if you’re under 59½. Always verify compliance with your custodian before executing any purchase inside the account.

If you are ready to explore how physical precious metals can strengthen your retirement strategy, Augusta Precious Metals offers a full range of IRS-approved gold and silver products along with expert guidance to help you build a Gold IRA that works for your long-term goals.

Investment Minimums – Personal Considerations

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, life-long customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Summary

Gold IRA demand has reached a notable inflection point in 2026, driven by a confluence of macroeconomic pressures and structural shifts in retirement planning. Persistent inflation, geopolitical instability, and growing skepticism toward dollar-denominated assets have pushed investors toward physical gold as a long-term portfolio anchor. The full implementation of SECURE Act 2.0 has further accelerated this trend, prompting a fresh reassessment of distribution strategies, Roth conversions, and legacy planning — all areas where a Gold IRA can play a meaningful role.

The core benefits driving adoption include inflation hedging, portfolio diversification, tax-advantaged accumulation inside an IRA structure, and protection against currency debasement. Roth Gold IRAs in particular are gaining traction as multi-generational wealth transfer tools, offering tax-free inheritance for beneficiaries.

However, the surge in demand has also attracted predatory operators into the space. Choosing the right provider requires rigorous due diligence — verifying IRS-authorized custodians, scrutinizing fee disclosures, checking BBB and Trustpilot ratings, and avoiding any company that promotes home storage IRAs or guarantees returns. Red flags in provider selection are often more costly than mistakes made during the rollover itself.

Executing a Gold IRA rollover involves four key steps: selecting an IRS-compliant self-directed IRA custodian, initiating a direct rollover from your 401(k) administrator, purchasing IRS-approved metals, and confirming regulated depository storage. Only metals meeting the IRS 99.5% purity threshold qualify — with the American Gold Eagle as the sole exception – and all holdings must be stored at an approved depository, never at home.

For investors ready to act, providers like Augusta Precious Metals (best for investors with $50K+), Birch Gold Group (best for established trust and low fees), and National Gold Group (best for transparency and buyback) each offer distinct strengths depending on your investment size and priorities.

Frequently Asked Questions

Q: Why is Gold IRA demand surging in 2026? A: A combination of persistent inflation, geopolitical instability, and the full implementation of SECURE Act 2.0 provisions has prompted investors to seek more resilient retirement allocations. Physical gold’s low correlation to equities and its historical role as a purchasing power hedge have made Gold IRAs an increasingly deliberate choice — not a speculative one.

Q: What’s the difference between a Gold IRA company and a custodian? A: A Gold IRA company (or dealer) guides you through the process, helps you select IRS-approved metals, and connects you with a custodian and depository. The custodian is the IRS-authorized institution that actually holds your account. You need both — and vetting each separately is essential before committing.

Q: What gold products are approved for a Gold IRA? A: Gold must meet a minimum purity of 99.5% fineness. IRS-approved options include the American Gold Buffalo, Canadian Gold Maple Leaf, and bars from NYMEX/COMEX-approved refiners like PAMP Suisse. The American Gold Eagle is the one exception — it’s only 91.67% pure but is IRS-approved due to its U.S. legal tender status. Collectibles, numismatic coins, and jewelry are prohibited.

Q: Can I store my Gold IRA metals at home? A: No. Home storage Gold IRAs are not a legitimate IRS-compliant option despite being promoted by some providers. Your metals must be held at an IRS-approved depository. Taking personal possession of the metals before a qualified distribution triggers a taxable event and potential penalties.

Q: How long does a 401(k) to Gold IRA rollover take? A: Most rollovers take approximately 2 to 3 weeks from initiation to completion. The timeline is longer than a standard IRA-to-IRA transfer because the 401(k) plan administrator, employer, and new custodian all need to coordinate. Always request a direct rollover — payable to your new custodian, not to you — to avoid mandatory 20% federal tax withholding.

Sources:

Gold IRA Rules and Regulations: LendEDU

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Investments in collectibles in individually directed qualified plan accounts: IRS.gov: Retirement plans FAQs regarding IRAs: IRS.gov

Leave a Reply