Quick Summary

You don’t need $25K to open a gold IRA — National Gold Group, Birch Gold Group, and American Hartford Gold all accept accounts starting around $10,000. National Gold Group is best for personalized guidance; Birch Gold Group excels at rollover support and metal variety; American Hartford Gold wins on low ongoing costs (~$175/year) and a flat-fee structure that doesn’t penalize smaller investors. Before opening, factor in that flat annual fees (~$175–$180) represent ~1.8% of a $10K account, so a long-term hold strategy and planned contributions make the most sense.

Table of Contents

- Quick Summary

- The best gold IRA providers that welcome accounts under $10,000 and won’t turn you away for being a smaller investor.

- Top 3 Gold IRA Companies for Small Investors

- 1. National Gold Group

- 2. Birch Gold Group

- 3. American Hartford Gold

- How to Choose the Right Provider for Your Situation

- Taking the Next Step

- Frequently Asked Questions

The best gold IRA providers that welcome accounts under $10,000 and won’t turn you away for being a smaller investor.

A common mistake many people make is assuming that you need $25,000 or more to open a gold IRA and that anything less isn’t worth the effort. However, if you can identify companies that specifically welcome smaller accounts and offer transparent fee structures, you can get real precious metals diversification with $10,000 or less.

You might be avoiding gold IRAs entirely because you keep seeing high minimums advertised everywhere, and these barriers can lead to postponing diversification indefinitely or feeling shut out of precious metals investing altogether.

Instead, you can focus on the handful of reputable firms that have built their business model around serving smaller investors, which quickly leads to actual precious metals in your retirement account as well as peace of mind that you’re not missing out on this asset class.

In this guide, you’ll explore the three best gold IRA companies with low investment minimums that have helped thousands of investors get started with modest balances.

This material includes detailed fee breakdowns from many independent review sources and shows you how to choose the right provider for your situation. After you read through these options, ask yourself: do you have any doubt that you can open a gold IRA with $10,000 or less?

People who haven’t explored this market recently often believe they could never use a gold IRA with their current savings level. They couldn’t be more wrong.

You actually can separate the marketing hype from the real accessibility of these accounts.

The transparent approach helps whether you’re rolling over a small 401(k) or making your first IRA contribution. The core principle is proven to be effective across different account sizes.

Often, the peace of mind from the diversification in later years will multiply what you invest in setup time and modest fees today.

Sometimes, far better.

Top 3 Gold IRA Companies for Small Investors

These three companies stand out for actually welcoming investors with $10,000 or less, maintaining transparent fee structures, and providing solid educational support throughout the process.

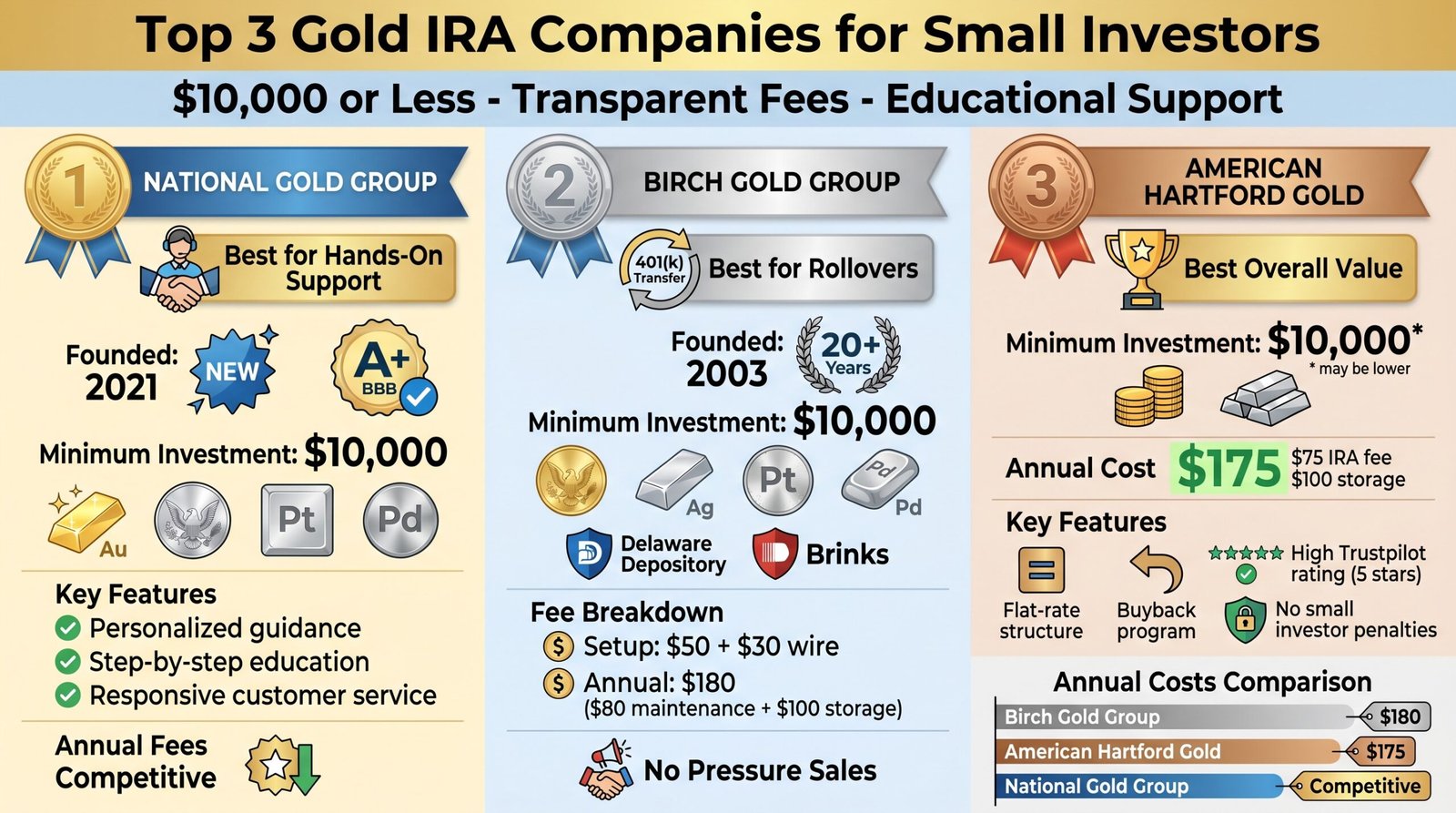

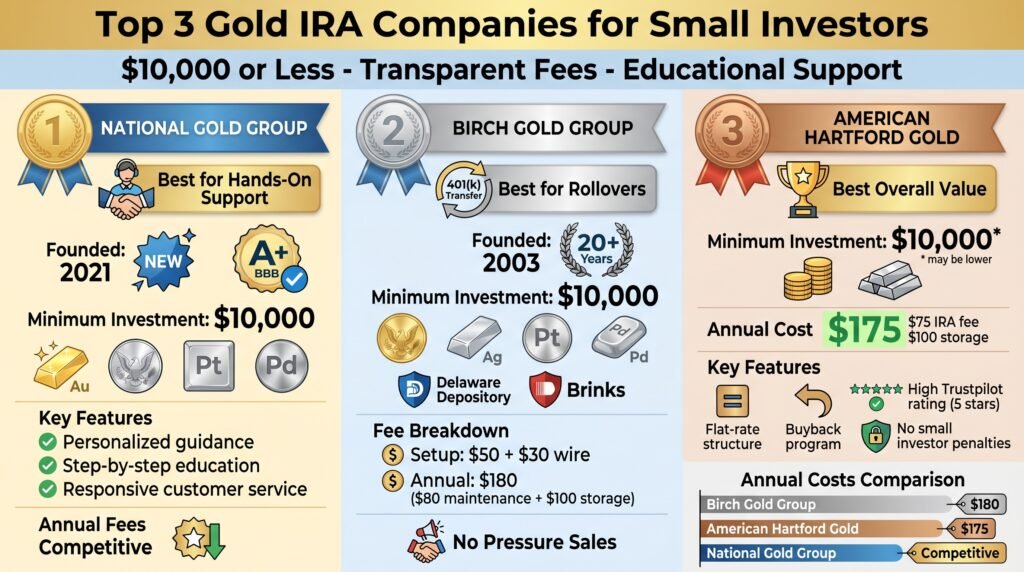

1. National Gold Group

Best for hands-on support and personalized guidance

National Gold Group is the newest of these three companies, founded in 2021, but it has already earned an A+ rating with the Better Business Bureau and shows up consistently in independent reviews as a strong option for smaller investors.

The company sets its minimum at $10,000 for both physical metals purchases and precious metals IRAs, which puts it squarely in reach for moderate investors. According to Retirement Living and other review sources, National Gold emphasizes personalized customer service and ongoing account support.

What makes National Gold particularly appealing if you’re new to precious metals is the focus on education and guidance. Representatives walk you through each step of opening your account, selecting appropriate metals, and understanding the storage and insurance arrangements.

Multiple reviews highlight responsive customer service and a willingness to answer questions without rushing you through the process.

The fee structure follows industry standards with competitive annual maintenance and storage costs. The company promotes low first-year fees and sometimes offers promotional waivers for larger accounts, though you should verify current terms when you contact them.

You can invest in gold, silver, platinum, and palladium through National Gold, working with approved custodians and depositories that meet IRS requirements. The company focuses on helping you build a mix of metals based on your specific situation as opposed to pushing any single product.

Because it’s newer, you won’t find the same decades-long track record you get with Birch Gold Group. However, current customer feedback is consistently positive, and the company appears on many “best of” lists for 2025 and 2026.

Start your gold IRA or rollover account today with National Gold Group by clicking the banner below and filling out their short form to receive their free guide.

2. Birch Gold Group

Best for rollover assistance and many precious metal options

Birch Gold Group has operated since 2003 and built a solid track record helping people roll over existing retirement accounts into precious metals IRAs. They set their least at exactly $10,000, which is confirmed by many independent review sites, including Retirement Living and Investing.com.

If you have funds spread across old employer 401(k) plans or traditional IRAs, Birch provides hands-on support to navigate the rollover process. They work with several qualified custodians and use well-known depositories like Delaware Depository and Brinks for secure storage of your metals.

The fee structure is transparent and typical for the industry. You’ll pay a one-time $50 account setup fee and a $30 wire transfer fee when you open your account.

After that, expect about $80 per year in maintenance fees and roughly $100 annually for storage, bringing your total ongoing cost to about $180 per year.

One advantage Birch Gold offers is access to gold, silver, platinum, and palladium, as long as they meet IRS purity standards. That gives you more diversification options within your precious metals allocation compared with companies that only focus on gold and silver.

The company emphasizes investor education and takes time to explain both the potential benefits and risks of precious metals investing. Multiple reviewers note that representatives don’t use high-pressure tactics and focus on helping you understand what you’re buying.

To get started protecting your hard-earned retirement savings with Birch Gold Group, click the banner below to visit their official site and fill out their short form to receive a free gold IRA guide:

3. American Hartford Gold

Best overall for low ongoing costs and strong reputation

American Hartford Gold makes it straightforward to open a precious metals IRA with around $10,000, and some sources indicate they have no formal minimum for self-directed gold IRAs. The company built its reputation on transparent pricing and keeping annual costs manageable for smaller accounts.

American Hartford typically charges an annual IRA fee of just $75 for accounts up to $100,000, plus about $100 per year for depository storage. That puts your total ongoing cost at around $175 annually, which is competitive across the industry.

The company often offers promotions that waive first-year fees for larger purchases, though you shouldn’t count on those applying to a $10,000 account.

What really sets American Hartford apart is that they don’t punish you for being a smaller investor. You get the same flat-rate fee structure as someone with a six-figure account, which means the percentage cost is higher for you, but you’re not paying scaled-up fees or facing the lowest balance penalties.

You can hold IRS-approved gold and silver products from major mints, and the company maintains a buyback program if you need to liquidate your metals later. Their customer service ratings are consistently high, with strong marks on Trustpilot and positive feedback about the educational approach they take with new investors.

To take advantage of American Hartford Gold’s trusted reputation and service, click the banner below to visit their official site and fill out their short form to receive a free gold IRA investment.

How to Choose the Right Provider for Your Situation

When you’re working with $10,000 or less, the math matters differently than it does for larger accounts. A $180 annual fee represents 1.8% of a $10,000 account but only 0.18% of a $100,000 account.

That means you need to think about your timeline and contribution plans.

If you plan to hold your gold IRA for many years and expect to add contributions over time, the percentage cost gradually shrinks and the diversification benefit can outweigh the fee impact. If you’re planning to open a $10,000 account and never add to it, you need to factor in that ongoing cost when deciding whether a gold IRA makes sense for you.

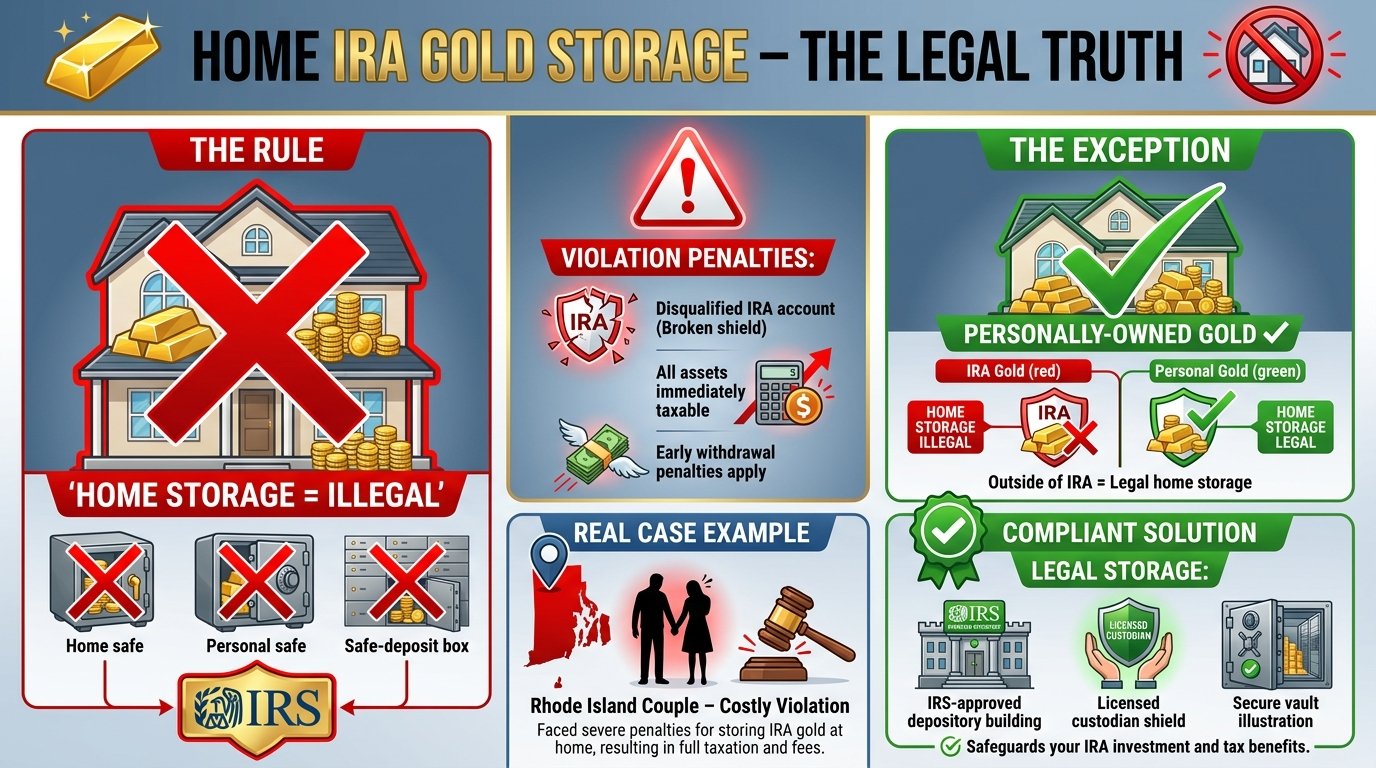

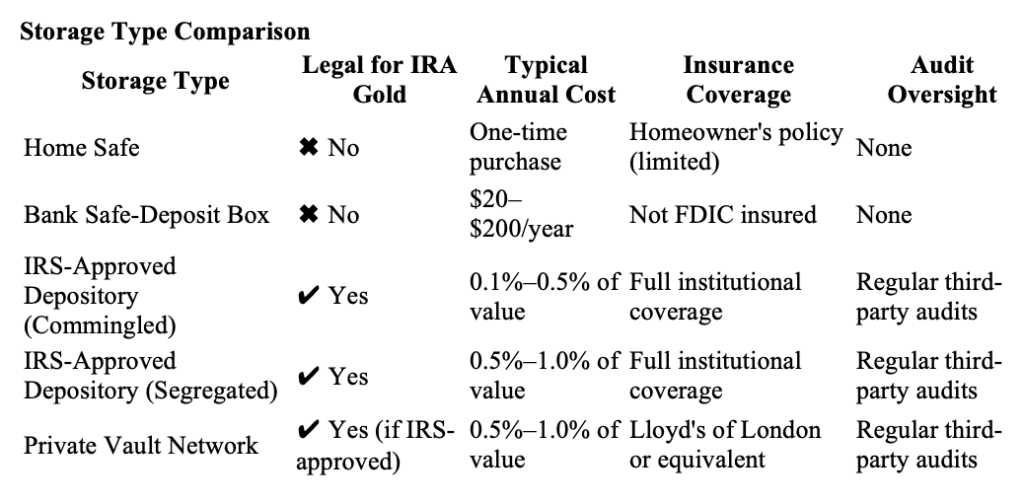

All three of these companies use similar custodial and storage arrangements. Your metals will be held in an IRS-approved depository with insurance and security.

You won’t physically possess the metals while they’re in your IRA, but you can typically arrange delivery or liquidation when you reach retirement age.

The main differences come down to customer service style, exact fee amounts, and how much hand-holding you want during the process.

National Gold Group gives you a more personalized, guided experience if that matters to you.

Birch Gold Group provides excellent rollover support and more metal choices.

American Hartford Gold offers the best combination of low fees and a strong reputation.

Taking the Next Step

The practical move is to contact your top choice directly and ask specific questions about opening an account at your exact balance. Get written confirmation of all fees, including setup costs, annual maintenance, storage charges, and any potential transaction fees for buying or selling metals.

Compare what you receive in writing with the fee ranges described here. If something doesn’t match, ask for clarification before you commit.

Reputable companies will provide clear documentation and won’t pressure you to decide immediately.

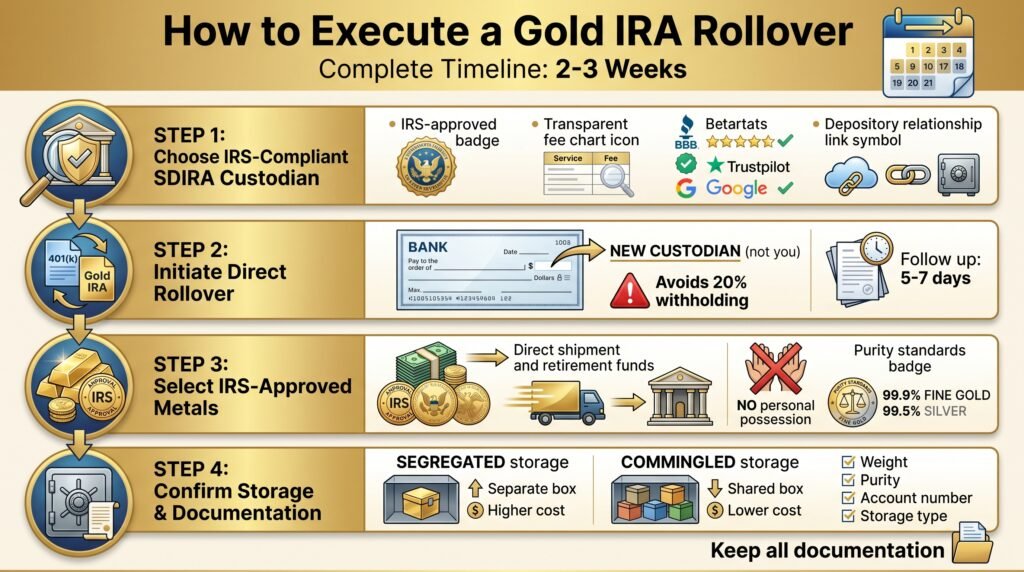

Most of these firms will assign you a representative who walks you through opening a self-directed IRA with their preferred custodian, initiating a rollover or transfer from your existing retirement account, selecting IRS-approved metals, and completing the purchase. The entire process typically takes a few weeks from start to finish.

Click the banner below to receive a free gold investing guide from the gold IRA company that is right for you. Fill out their short contact form to get started.

Frequently Asked Questions

Can you really open a gold IRA with less than $10,000?

Yes, several companies, including American Hartford Gold, accept accounts at or near $10,000, and some have no stated minimum for self-directed IRAs. The challenge isn’t usually the least itself but rather the fee percentage on smaller balances.

With flat annual fees around $175 to $180, you’re looking at roughly 1.8% of a $10,000 account going to fees each year.

That’s workable if you plan to hold long-term and add to the account, but it’s a meaningful percentage to consider when deciding whether a gold IRA makes sense for your situation.

How do gold IRA fees affect small accounts differently?

Gold IRA companies typically charge flat annual fees for maintenance and storage as opposed to percentage-based fees. A $180 annual fee costs you the same whether your account holds $10,000 or $100,000.

For smaller accounts, that represents a higher percentage cost.

The trade-off is that you get access to the same services, security, and diversification benefits as larger investors. You can offset the percentage impact by planning to grow your account over time through extra contributions or rollovers.

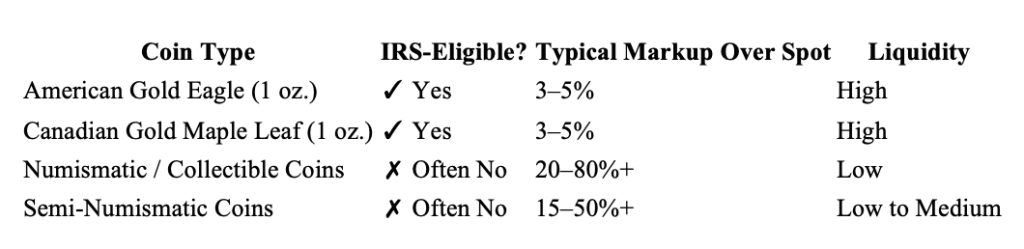

What metals can you hold in a gold IRA?

The IRS sets strict purity requirements for metals in self-directed IRAs.

For gold, you need .995 fineness or higher.

Silver must be .999 pure.

Platinum and palladium must meet .9995 purity.

Common approved products include American Gold Eagles, Canadian Gold Maple Leafs, Austrian Gold Philharmonics, and gold bars from approved refiners.

The companies listed here work with IRS-approved metals and can guide you toward products that qualify.

Collectible coins, numismatic items, and certain commemorative pieces don’t qualify for IRA holding.

Is a gold IRA better than buying physical gold outside an IRA?

Each approach has different benefits. A gold IRA gives you tax advantages since your investment grows tax-deferred in a traditional IRA or tax-free in a Roth IRA.

You can roll over existing retirement funds without triggering taxes.

The downsides are annual fees, restrictions on which metals qualify, and the requirement to store metals in an approved depository as opposed to at home.

Buying physical gold outside an IRA gives you direct possession, no annual storage fees, and more flexibility in what you buy, but you lose the tax advantages and typically buy with after-tax dollars.

How long does it take to open a gold IRA?

The timeline from initial contact to having metals in your account typically runs two to four weeks. You’ll spend a few days opening the self-directed IRA with the custodian, then start your rollover or transfer, which can take one to two weeks, depending on your current retirement account provider.

Once funds arrive, selecting and purchasing your metals usually happens within a few days.

Some steps can overlap, and urgent situations might move faster, but plan on a few weeks for the complete process.

Can you add to your gold IRA after you open it?

Yes, you can make extra contributions to your gold IRA, subject to annual IRA contribution limits set by the IRS. For 2025, the limit is $7,000 for people under 50 and $8,000 for those 50 and older.

You can also roll over extra funds from other qualified retirement accounts at any time.

Many investors start with a smaller balance and gradually build their precious metals allocation over several years. Adding to your account over time helps reduce the percentage impact of flat annual fees.

What happens to your gold IRA if the company goes out of business?

Your metals are held in an IRS-approved depository, not by the gold dealer or IRA company. If the company you purchased through goes out of business, your metals stay safely stored in your name at the depository.

You would work with your IRA custodian to engage a different dealer for any future transactions or to arrange a transfer to another provider.

The separation between the dealer, custodian, and depository provides important protection. This is why working with established companies that use well-known custodians and depositories matters for peace of mind.

References

- Retirement Living, “American Hartford Gold Review (2026)”

- Money.com, “American Hartford Gold Group Gold IRA Review”

- Retirement Living, “Birch Gold Group Review (2026)”

- Investing.com, “Birch Gold Group Review 2026”

- Retirement Living, “National Gold Group Review (2026)”

- ConsumerAffairs, “The Best Gold IRA Companies (2026 Guide)”

- Bankrate, “The Best Gold IRA Companies: Where To Set Up A Gold IRA”