Quick Summary

- Teachers and nonprofit workers can roll over a 403(b) into a gold IRA completely tax-free using a direct rollover, with no penalties and no taxable events.

- A gold IRA is a self-directed retirement account that holds physical precious metals like gold bullion and coins approved by the IRS.

- Not everyone qualifies immediately; your eligibility depends on your age, employment status, and your plan’s specific rollover rules.

- The 60-day rule for indirect rollovers is a hard deadline; miss it, and the IRS treats the entire amount as taxable income.

- There’s a critical step in choosing a gold IRA company that most guides skip over, and it could save you from losing your entire retirement savings to fraud.

Rolling over your 403(b) into a gold IRA is one of the most powerful moves a teacher or nonprofit worker can make to protect retirement savings from inflation, and it can be done completely tax-free.

Augusta Precious Metals is a leading precious metals company that specializes in helping educators and nonprofit professionals navigate gold IRA rollovers with confidence. Whether you’re just starting to research your options or ready to make the move, understanding the full process puts you in control of your financial future.

Table of Contents

- Quick Summary

- Teachers and Nonprofit Workers Can Roll Over a 403(b) Into a Gold IRA Tax-Free

- You Must Meet These Eligibility Requirements Before You Roll Over

- Here Are the Step-by-Step Instructions for a 403(b) to Gold IRA Rollover

- Tax Implications You Need to Know Before You Roll Over

- Start Your 403(b) Gold IRA Rollover with Confidence

- Frequently Asked Questions

Teachers and Nonprofit Workers Can Roll Over a 403(b) Into a Gold IRA Tax-Free

Most people assume moving retirement funds is complicated, taxable, or risky. The truth is, when done correctly through a direct rollover, transferring your 403(b) into a gold IRA triggers zero taxes and zero penalties. Your money simply moves from one tax-advantaged account to another, with the added protection of physical gold backing your retirement.

What a Gold IRA Actually Is

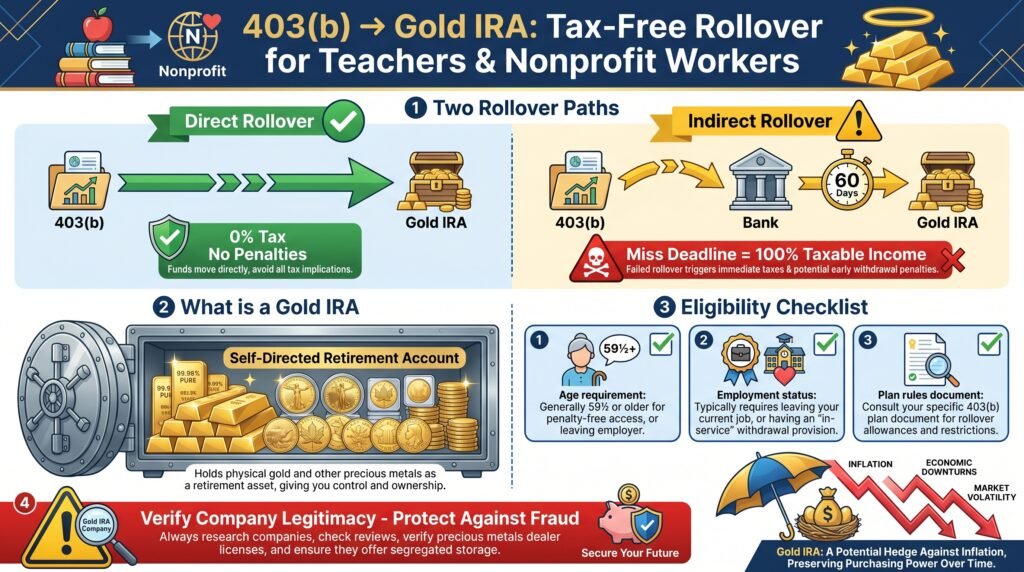

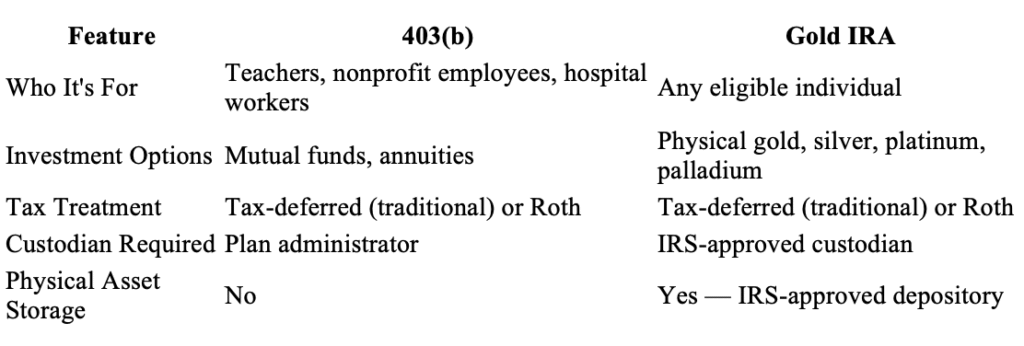

A gold IRA is a self-directed individual retirement account that holds physical precious metals instead of, or alongside, traditional paper assets like stocks and mutual funds. Unlike a standard IRA, a gold IRA requires an IRS-approved custodian and an approved depository to store the physical metals on your behalf. You never personally hold the gold; it lives in a secure, insured facility.

The metals allowed inside a gold IRA must meet strict IRS purity standards. Gold must be at least 99.5% pure, which includes products like the American Gold Eagle coin, Canadian Gold Maple Leaf, and gold bars produced by NYMEX or COMEX-approved refiners. Silver, platinum, and palladium are also permitted under similar purity requirements.

How a 403(b) Differs From a 401(k)

A 403(b) is an employer-sponsored retirement plan specifically designed for employees of public schools, universities, hospitals, and nonprofit organizations. It functions similarly to a 401(k) in terms of contribution limits and tax-deferred growth, but it’s tailored to the unique employment structures of the education and nonprofit sectors.

One key difference is that 403(b) plans are often more restrictive in their investment options, frequently limiting participants to annuities and mutual funds. This is precisely why so many educators and nonprofit workers look to roll over into a self-directed gold IRA; it opens the door to asset classes their 403(b) simply doesn’t offer.

Why Educators Are Turning to Gold for Retirement Security

Teacher pension systems across the country have faced funding shortfalls for years, leaving many educators uncertain about what their retirement will actually look like. Gold has historically held its value during economic downturns, stock market crashes, and periods of high inflation, making it an attractive complement to an otherwise volatile retirement portfolio.

When the purchasing power of the dollar erodes, physical gold tends to move in the opposite direction. For a teacher or nonprofit worker whose pension may already be underfunded, adding gold to a self-directed IRA creates a meaningful layer of financial protection that paper assets simply can’t replicate. Learn about the real benefits of a gold IRA here, such as inflation hedging, portfolio diversification, and much more

You Must Meet These Eligibility Requirements Before You Roll Over

Before you contact a gold IRA company or start any paperwork, you need to confirm you actually qualify for a rollover. Moving forward without checking eligibility first is one of the most common, and costly, mistakes people make.

Age, Employment Status, and Other Qualifying Conditions

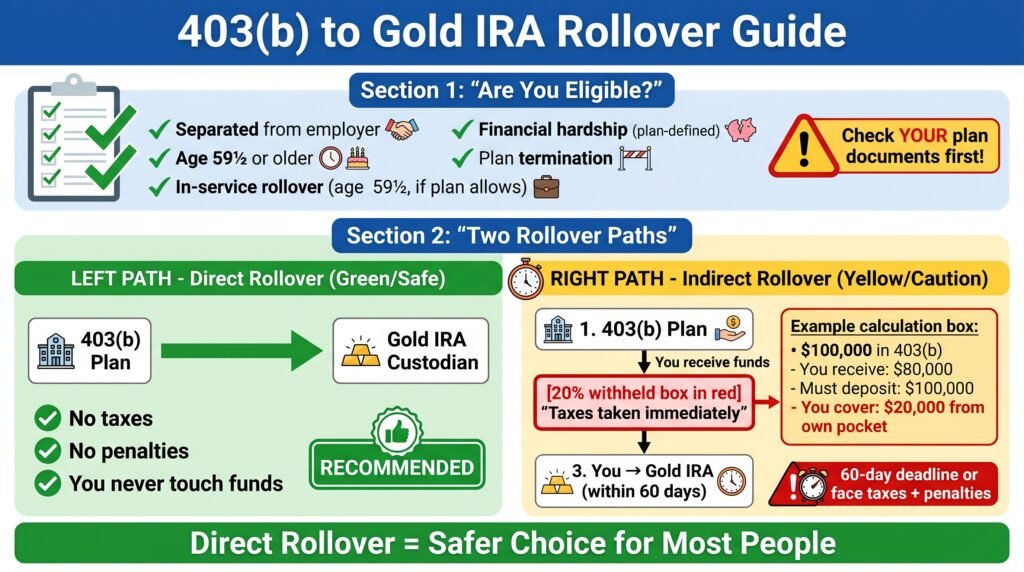

The IRS allows 403(b) rollovers under several qualifying conditions. You are generally eligible if you have separated from your employer, reached age 59½, experienced a financial hardship as defined by your plan, or your plan is being terminated. Some plans also allow in-service rollovers for participants who are still employed but have reached a certain age, typically 59½.

It’s critical to check your specific 403(b) plan documents before assuming you qualify. Each plan has its own rules, and some may have additional restrictions or waiting periods. Contact your plan administrator directly and ask specifically whether your account is eligible for a rollover and what documentation they require.

Direct vs. Indirect Rollover: Which One Protects You From Penalties

A direct rollover means the funds move straight from your 403(b) plan administrator to your new gold IRA custodian. You never touch the money. This is the safest method because it eliminates any risk of triggering taxes or penalties; the IRS does not treat a direct rollover as a distribution.

An indirect rollover works differently. Your plan administrator sends the funds directly to you, and you have 60 days to deposit the full amount into your new gold IRA.

Here’s the catch: your plan administrator is required to withhold 20% for federal taxes upfront. That means if you have $100,000 in your 403(b), you’ll only receive $80,000.

To avoid a taxable event, you must deposit the full $100,000 into your gold IRA within 60 days, including the $20,000 that was withheld, using your own funds. For most people, a direct rollover is the clear choice.

Here Are the Step-by-Step Instructions for a 403(b) to Gold IRA Rollover

The actual rollover process is more straightforward than most people expect, but the order of operations matters. Skipping steps or rushing the paperwork can create delays, tax complications, or worse. Follow this sequence carefully.

1. Choose a Reputable Gold IRA Company

Your Gold IRA company is not the same as your custodian; it is the dealer that guides you through the process, helps you select IRS-approved metals, and connects you with a custodian and depository. Choosing the right one upfront saves you from costly mistakes later.

Look for companies with long operating histories, transparent fee structures, and strong third-party reviews. A company that pressures you into making a quick decision or upsells you into rare or collectible coins is a red flag; collectibles are not IRS-approved for Gold IRAs and can disqualify your account.

Augusta Precious Metals is one example of an established precious metals provider that helps investors navigate the Gold IRA process, offering IRS-approved coins and bars along with educational resources for beginners who are just getting started with precious metals retirement planning.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get started.

Before committing to any company, ask these questions directly:

- What are your setup, storage, and annual maintenance fees?

- Which custodians and depositories do you work with?

- What IRS-approved metals do you carry?

- Do you offer buyback programs if I need to liquidate?

2. Select an IRS-Compliant Custodian

A custodian is the IRS-approved financial institution that works with your chosen gold IRA company and is responsible for administering your gold IRA and keeping your account compliant. The company handles the paperwork, record-keeping, and coordination with the depository where your physical metals are stored. Your gold IRA company will typically have preferred custodian partners they can recommend, but you always have the right to choose your own.

Custodian fees vary and typically include an account setup fee, annual maintenance fee, and storage fees for the physical metals. Make sure you get a full fee schedule in writing before committing to any custodian.

3. Contact Your 403(b) Plan Administrator

- Ask whether your account is eligible for a rollover under your current employment and age status

- Request the specific rollover or distribution forms required by your plan

- Confirm whether your plan requires a signature guarantee or notarization on any documents

- Ask for the exact wire transfer instructions or mailing address for your new gold IRA custodian

- Get a timeline, ask how long the fund transfer typically takes once paperwork is submitted

This step tends to take longer than people anticipate. Some 403(b) plan administrators process rollover requests within a few business days, while others, particularly large institutional plans, can take two to four weeks just to process the initial paperwork.

Stay proactive and follow up regularly. Keep records of every conversation, including the date, the representative’s name, and what was discussed. This paper trail protects you if anything goes wrong during the transfer.

4. Complete the Rollover Paperwork

Once your chosen gold IRA company and 403(b) administrators are aligned, you’ll complete transfer authorization forms from both sides. Your gold IRA custodian will provide a new account application along with a transfer request form that authorizes the movement of funds directly from your 403(b). Double-check every detail, account numbers, legal names, and transfer amounts, before submitting. A single error can delay the process by weeks.

5. Fund Your Gold IRA and Choose Your Metals

Once the funds arrive in your gold IRA, you’ll work with your gold IRA company to select which IRS-approved precious metals to purchase. Your options include gold bullion bars, gold coins like the American Gold Eagle or the Canadian Gold Maple Leaf, and similar approved silver, platinum, or palladium products. Your custodian will then purchase the metals on your behalf and arrange for secure storage at an IRS-approved depository.

The entire process, from opening your gold IRA to having metals stored in your account, typically takes several weeks to more than a month, depending on how quickly your 403(b) plan administrator processes the transfer. Patience here is important. Rushing the process or pressuring any party to move faster than their compliance procedures allow can introduce errors that are difficult to correct.

Tax Implications You Need to Know Before You Roll Over

The tax treatment of your rollover depends entirely on how you execute it and what type of 403(b) you have. Getting this wrong doesn’t just cost you money; it can trigger IRS penalties that take years to recover from.

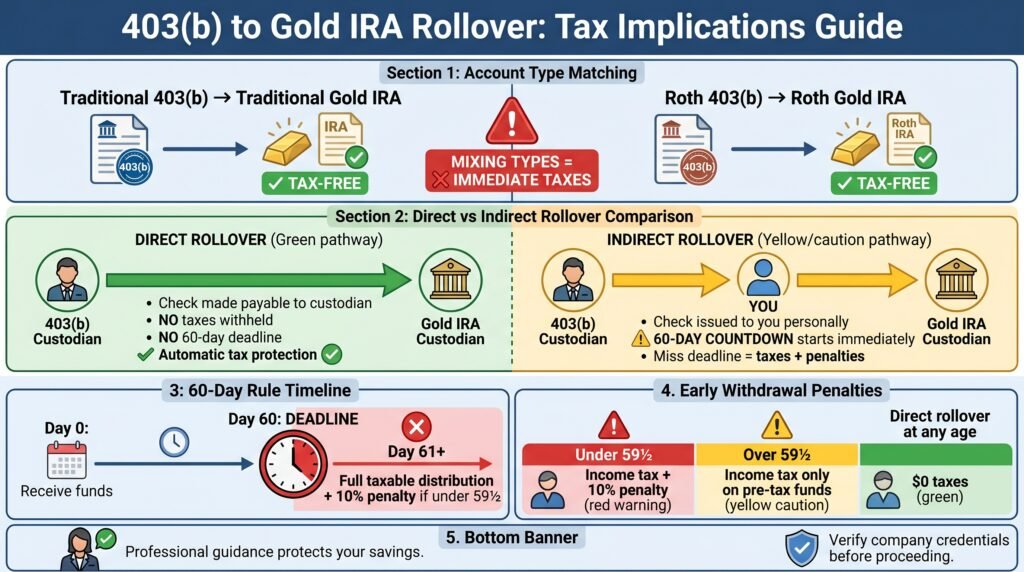

If your 403(b) is a traditional pre-tax account, rolling it into a traditional gold IRA is a non-taxable event when done as a direct rollover. If your 403(b) has a Roth component, it must roll into a Roth gold IRA to maintain that tax-free status. Mixing these up creates an immediate taxable event on the converted amount.

How Direct Rollovers Keep the Transaction Tax-Free

In a direct rollover, the funds never pass through your hands. Your 403(b) plan administrator wires the money, or sends a check made payable directly to your new gold IRA custodian, without any withholding. Because you never receive the funds as a distribution, the IRS does not classify the transaction as taxable income.

This is the single most important reason to choose a direct rollover over an indirect one. The tax protection is automatic and built into the mechanism of the transfer itself. There’s no filing required, no special election to make; the structure of the transaction does the work for you.

Make sure to confirm in writing with your 403(b) administrator that the transfer will be processed as a direct rollover and that the check or wire is made payable to your custodian, not to you personally. This one detail is the difference between a tax-free transfer and an unexpected tax bill.

The 60-Day Rule for Indirect Rollovers

If you choose an indirect rollover, or if a direct rollover somehow results in a check being issued to you, the IRS gives you exactly 60 days to deposit the full original amount into your new gold IRA. Miss that deadline by even one day and the entire amount is treated as a taxable distribution, subject to income tax plus a 10% early withdrawal penalty if you’re under age 59½. The IRS grants very few exceptions to this rule, and “I forgot” is not one of them.

Early Withdrawal Penalties and How to Avoid Them

The 10% early withdrawal penalty applies to any distribution taken from a 403(b) before age 59½ that isn’t rolled over correctly. The simplest way to avoid it is to execute a direct rollover and never take personal possession of the funds. If you’re over 59½, the penalty no longer applies, but income taxes on pre-tax funds still do unless the money moves into another tax-deferred account.

Why Working With a Tax Professional Is Worth It

The IRS rules around retirement account rollovers are detailed, and the stakes are high enough that professional guidance pays for itself many times over. A seasoned gold IRA company familiar with self-directed IRAs can review your specific 403(b) plan documents, confirm your rollover strategy is structured correctly, and help you avoid the kinds of mistakes that trigger audits or penalties.

This is especially important if you have both traditional and Roth contributions in your 403(b), have made after-tax contributions, or your plan includes employer matching funds with vesting schedules. Each of these factors affects how your rollover should be structured, and getting it right from the start is far easier than trying to fix it after the fact.

How to Verify a Gold IRA Company Is Legitimate

The gold IRA industry attracts both legitimate and predatory companies. Before you hand over your life savings to any firm, take the time to independently verify their credentials. A few minutes of due diligence can protect decades of retirement savings. Read more about what to look for when considering a gold IRA company for your 403(b) rollover.

If you want a quick start guide, click the banner below to access Augusta Precious Metals’ free gold IRA company integrity guide. Fill out their short form to get started.

Investment Minimums – Personal Considerations

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, life-long customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Start Your 403(b) Gold IRA Rollover with Confidence

You’ve now got the full picture, eligibility requirements, direct vs. indirect rollover mechanics, tax implications, step-by-step instructions, and how to separate legitimate companies from fraudulent ones. The path forward is clear: choose a reputable gold IRA company, open a self-directed account with an IRS-approved custodian, initiate a direct rollover with your 403(b) plan administrator, and select your IRS-compliant precious metals. Done correctly, the entire transaction is tax-free, penalty-free, and one of the most effective ways to protect your retirement from inflation and market volatility.

Augusta Precious Metals has helped thousands of teachers and nonprofit workers make this transition. Visit Augusta Precious Metals to learn more about your gold IRA rollover options and take the next step toward a more secure retirement.

Find out whether gold IRAs are a good choice for your retirement needs. Access our Gold IRA calculator. Bookmark this page and perform real-time calculations as you read our reviews.

Click the banner below to access these calculators and start protecting your wealth today.

Frequently Asked Questions

If you are still weighing whether a Gold IRA fits your retirement plan, these are the questions most beginners ask before taking the next step.

Can I roll over my 401(k) into a Gold IRA without paying taxes?

Yes, you can roll over a 401(k), 403(b), TSP, or existing traditional IRA into a Gold IRA without triggering taxes or penalties, provided you use a direct rollover. In a direct rollover, the funds move from your existing plan administrator directly to your new Gold IRA custodian; you never personally receive the money.

If you opt for an indirect rollover instead (where the funds are sent to you first), you have 60 days to deposit the full amount into your new Gold IRA or the IRS will treat the distribution as taxable income and apply a 10% early withdrawal penalty if you are under age 59½. Direct rollovers are always the safer, cleaner option.

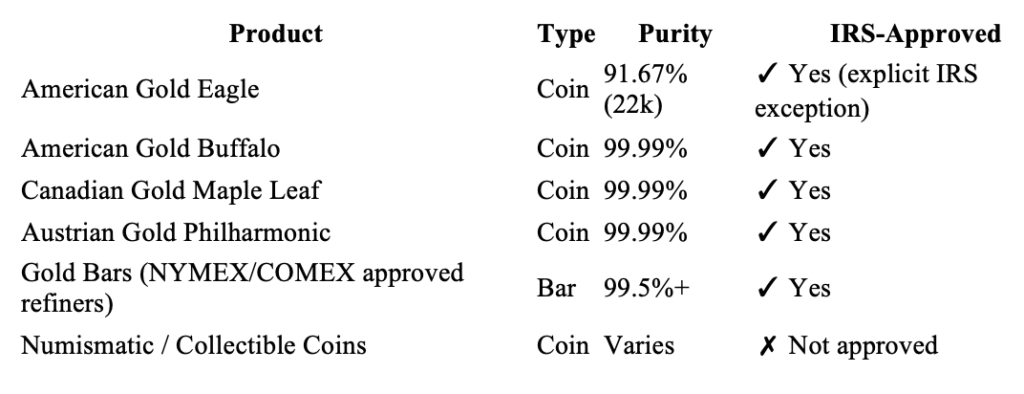

What gold coins and bars are IRS-approved for a Gold IRA?

IRS-approved gold products must meet a minimum fineness of 99.5% (except the American Gold Eagle coin). Below is a breakdown of the most commonly approved gold coins and bars for Gold IRA investors:

Always confirm with your custodian that the specific product you intend to purchase is on the IRS-approved list before completing any transaction. Purchasing a non-qualifying metal inside your IRA can trigger immediate tax consequences.

Gold bars must be produced by a refiner that is accredited by a national government mint or an approved commodities exchange such as NYMEX or COMEX. The bar must also be accompanied by an assay certificate verifying its weight and purity. Your Gold IRA company should handle verification as part of the purchase process; if they do not, that is a red flag worth taking seriously.

How much does it cost to open and maintain a Gold IRA?

The total cost of a Gold IRA typically includes three categories of fees: a one-time setup fee ranging from $50 to $150, an annual custodian administration fee between $75 and $300, and an annual depository storage fee between $100 and $300 (or a percentage-based fee for larger accounts). In total, most investors pay between $175 and $600 per year in ongoing fees, depending on the company and their account balance.

Some providers waive setup fees or first-year storage fees as a promotional incentive, which is worth taking advantage of, as long as you understand what the ongoing costs look like in subsequent years.

What happens to my Gold IRA when I retire?

When you reach retirement age and want to access your Gold IRA funds, you have two primary options: take an in-kind distribution or liquidate your holdings for cash. An in-kind distribution means the physical metals are transferred directly to you; you take possession of the actual gold or silver coins and bars.

A cash distribution means your custodian sells the metals and deposits the proceeds into your account, which you then withdraw as cash. Both options are subject to ordinary income tax for a traditional Gold IRA (since contributions were made pre-tax).

Required Minimum Distributions (RMDs) begin at age 73 for traditional Gold IRAs, the same rule that applies to all traditional IRAs. At that point, you are required to withdraw a minimum amount each year based on your account balance and IRS life expectancy tables.

If your Gold IRA holds physical metals and you want to satisfy your RMD without selling, you can take an in-kind distribution of metals equal in value to the required withdrawal amount, though this adds logistical complexity that not all custodians handle the same way.

If you are ready to explore how physical precious metals can strengthen your retirement strategy, Augusta Precious Metals offers a full range of IRS-approved gold and silver products along with expert guidance to help you build a Gold IRA that works for your long-term goals.

Sources:

Gold IRA Rules and Regulations: LendEDU

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Investments in collectibles in individually directed qualified plan accounts: IRS.gov: Retirement plans FAQs regarding IRAs: IRS.gov

Leave a Reply