Quick Summary

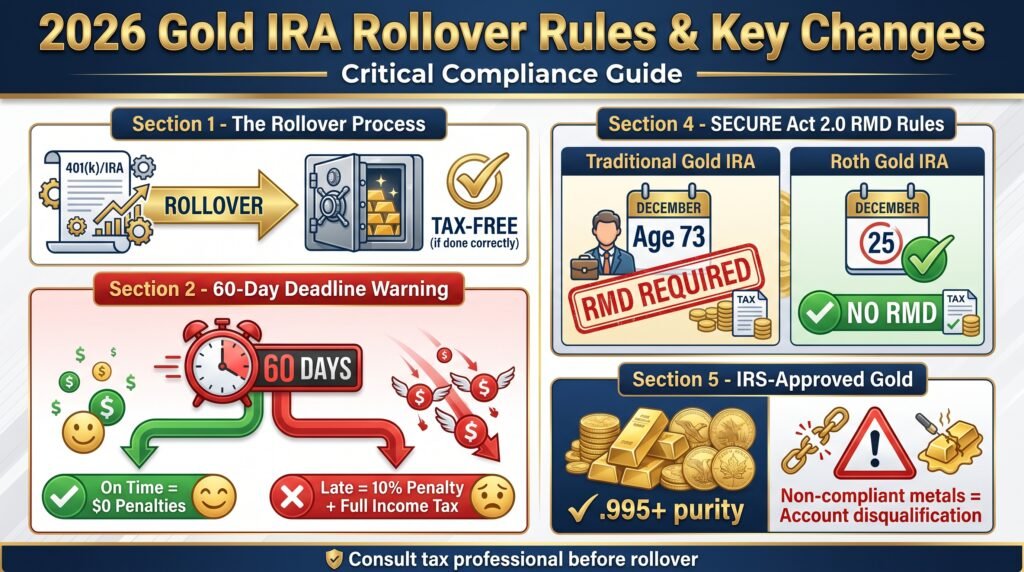

A Gold IRA rollover lets you move funds from a 401(k) or existing IRA into a self-directed account holding physical precious metals, completely tax-free if done correctly in 2026.

Missing the 60-day indirect rollover deadline triggers a 10% early withdrawal penalty plus ordinary income tax on the full balance, a mistake that can cost tens of thousands of dollars.

In 2026, contribution limits have increased: $7,500 for those under 50, and $8,600 for those 50 and older using the catch-up provision.

SECURE Act 2.0 rules now require Traditional Gold IRA holders to begin Required Minimum Distributions at age 73, Roth Gold IRAs have no such requirement.

Not all gold is IRS-approved; keep reading to find out exactly which coins and bars qualify, and which ones will disqualify your entire account.

Table of Contents

- Quick Summary

- Gold IRA Rollovers Are Changing in 2026: Here’s What You Need to Know First

- Direct vs. Indirect Rollovers: The Rule That Could Cost You 20%

- 2026 IRS Contribution Limits for Gold IRAs

- SECURE Act 2.0 Distribution Rules Now in Effect

- Home Storage of IRA Gold Is Still Illegal in 2026

- MAGI Phase-Out Ranges and Tax Implications in 2026

- How to Execute a Gold IRA Rollover in 2026

- The Bottom Line on Gold IRA Rollover Rules in 2026

- Frequently Asked Questions

Gold IRA Rollovers Are Changing in 2026: Here’s What You Need to Know First

The rules governing Gold IRA rollovers have never been more consequential than they are right now. With macroeconomic uncertainty pushing record numbers of investors away from traditional paper assets, Gold IRA rollover activity has surged sharply in 2026, according to a research report by Gold Silver News. That surge brings both opportunity and risk because the IRS rules governing these accounts are unforgiving, and a single procedural mistake can turn a tax-free transfer into a taxable distribution.

Whether you’re moving funds from a former employer’s 401(k) or reallocating an existing Traditional IRA, understanding the mechanics of how these rollovers work in 2026 is the difference between preserving your retirement wealth and watching a chunk of it disappear in penalties and taxes.

Direct vs. Indirect Rollovers: The Rule That Could Cost You 20%

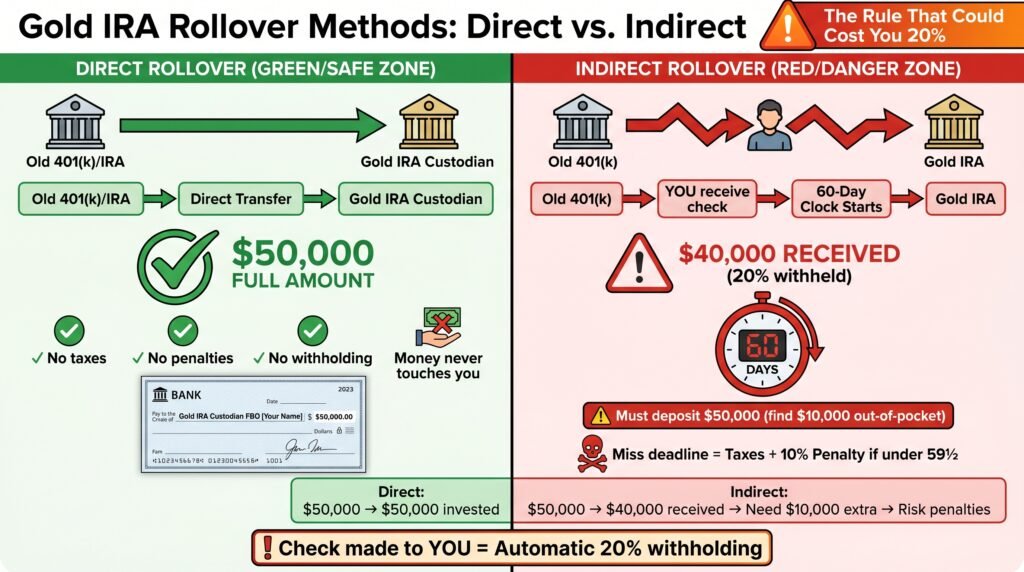

This is the most critical distinction in the entire Gold IRA rollover process, and it’s the one most investors get wrong. There are two methods: a direct rollover and an indirect (60-day) rollover. The method you choose determines whether your full account balance makes it into your new Gold IRA, or whether 20% of it gets withheld before you ever see it.

How a Direct Rollover Protects Your Full Account Value

In a direct rollover, the funds move directly from your existing plan administrator or IRA custodian to your new Gold IRA custodian. You never touch the money. The check is made payable to the new custodian, not to you, and there is no tax withholding, no penalty, and no reportable income event. This is the cleanest, safest way to execute a Gold IRA rollover in 2026.

A practical example: an investor transferring $50,000 from a former employer’s 401(k) into a self-directed Gold IRA via direct rollover receives the full $50,000 deposited into the new account. That full amount is immediately available to purchase IRS-approved metals. Nothing is lost to withholding.

The 60-Day Indirect Rollover Window and Its Penalties

With an indirect rollover, your plan administrator sends the distribution check directly to you. You then have exactly 60 calendar days to deposit the full amount into your new Gold IRA. Miss that deadline by even one day, and the IRS treats the entire distribution as ordinary taxable income, plus a 10% early withdrawal penalty if you’re under age 59½. There are no extensions and very few exceptions.

Why the Check Must Never Be Made Out to You

When a 401(k) distribution is paid directly to you, your employer’s plan administrator is required by law to withhold 20% for federal taxes upfront. That means if you’re rolling over $50,000, you only receive $40,000. To complete a valid rollover, you must deposit the full $50,000 into your Gold IRA within 60 days, which means you’d need to pay the missing $10,000 out of pocket. This is why a direct rollover is almost always the superior choice.

2026 IRS Contribution Limits for Gold IRAs

Rollovers do not count toward your annual contribution limits, but new contributions do. Here’s what the IRS allows in 2026:

The $7,500 Standard Limit and Who It Applies To

For investors under the age of 50, the 2026 IRS contribution limit for a Gold IRA is $7,500 per year. This applies whether your account is structured as a Traditional Gold IRA or a Roth Gold IRA. This limit is per person, not per account, meaning if you hold both a Traditional and a Roth IRA, your combined contributions across both accounts cannot exceed $7,500.

The $8,600 Catch-Up Contribution for Ages 50 and Over

If you’re 50 or older, the IRS allows an additional catch-up contribution, bringing your total annual limit to $8,600 in 2026. This provision exists specifically to help those closer to retirement age accelerate their precious metals accumulation within a tax-advantaged structure. If you haven’t been maximizing this, 2026 is the year to start.

How the Combined Limit Works Across Traditional and Roth IRAs

The $7,500 (or $8,600 catch-up) limit is an aggregate limit. Splitting contributions between a Traditional Gold IRA and a Roth Gold IRA is permitted, but the combined total cannot exceed the annual cap. Exceeding the limit triggers a 6% excise tax on the excess amount for every year it remains in the account, an easily avoidable but surprisingly common mistake.

SECURE Act 2.0 Distribution Rules Now in Effect

The SECURE Act 2.0 introduced phased changes to Required Minimum Distribution ages that are now actively shaping how Gold IRA holders plan their withdrawals. Understanding exactly when your RMDs kick in, and how to potentially eliminate them, is one of the highest-leverage decisions you can make in retirement planning right now.

Required Minimum Distributions Starting at Age 73

Under SECURE Act 2.0, individuals born between 1951 and 1959 must begin taking Required Minimum Distributions from their Traditional Gold IRA at age 73. For those born in 1960 or later, the RMD start age shifts to age 75, though that provision doesn’t become effective until 2033. Missing an RMD triggers a penalty of 25% of the amount that should have been withdrawn, reduced to 10% if corrected promptly within a two-year correction window. Your custodian is required to calculate your RMD annually, but the legal responsibility to take it on time falls on you.

Augusta Precious Metals is one example of an established traditional precious metals IRA and can help investors navigate the Gold IRA process with educational resources and competitive prices.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get started.

Why Roth Gold IRAs Have No RMD Requirement

This is one of the most powerful and underutilized advantages of the Roth Gold IRA structure. Roth accounts carry no RMD requirement during the original account holder’s lifetime, which means your physical gold holdings can continue compounding tax-free indefinitely.

When you pass, your beneficiaries inherit the account with the tax-free status intact, though they are subject to the 10-year distribution rule under SECURE Act 2.0. For investors who don’t need retirement income from this account and want to maximize estate transfer efficiency, the Roth Gold IRA is often the stronger structure.

Bear in mind, contributions for traditional gold IRAs are funded with pre-tax dollars. Contributions may be tax-deductible for the year you make them.

Roth gold IRA contributions are funded with after-tax dollars. You do not get an upfront tax deduction for your contributions.

Select the account type that works for your specific needs.

Home Storage of IRA Gold Is Still Illegal in 2026

This is a point worth stating plainly: you cannot store IRA-owned gold at home, in a personal safe, or in a safety deposit box in your name. Some marketing in the precious metals industry promotes so-called “home storage Gold IRAs” as a legal structure; they are not. The IRS requires that all physical metals held inside a Gold IRA be stored in an IRS-approved, insured depository managed by a qualified trustee or custodian.

Taking physical possession of your IRA metals, for any reason other than a qualified distribution, is treated by the IRS as a full taxable distribution of the assets you received. Popular approved depositories include Brink’s Global Services, Delaware Depository, and International Depository Services (IDS). Your Gold IRA custodian will facilitate the transfer of purchased metals directly to one of these facilities; you should never be handling the metals in transit yourself.

MAGI Phase-Out Ranges and Tax Implications in 2026

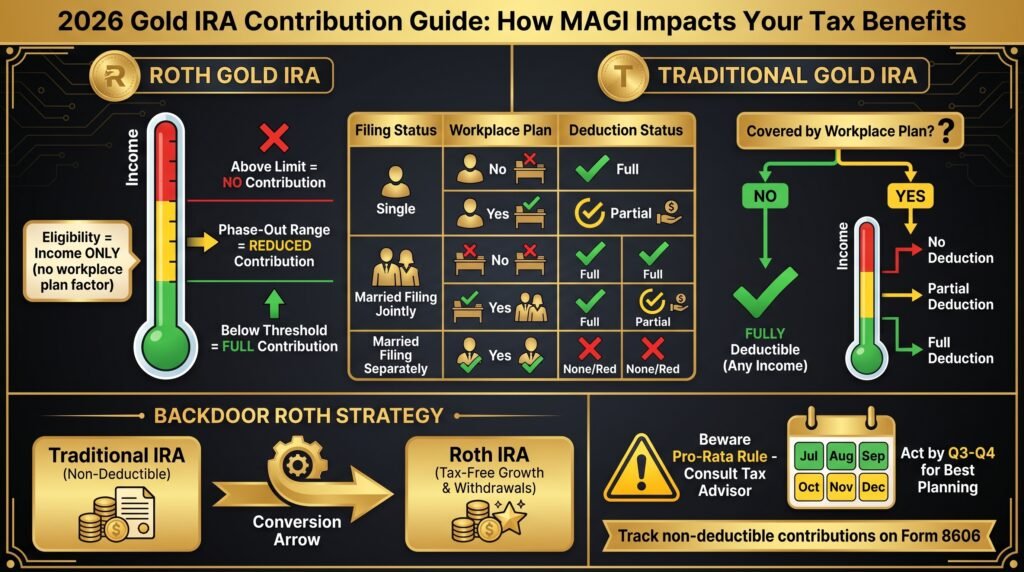

Your Modified Adjusted Gross Income (MAGI) directly determines both your ability to contribute to a Roth Gold IRA and whether your Traditional Gold IRA contributions are tax-deductible. These aren’t minor technical details; they can mean the difference between a fully deductible contribution and one that provides zero immediate tax benefit.

Both Traditional and Roth Gold IRAs are subject to income-based restrictions, but the rules work differently for each. Traditional IRA deductibility is affected by whether you (or your spouse) are covered by a workplace retirement plan. Roth IRA eligibility is based purely on income, with no workplace plan variable involved.

How MAGI Affects Your Roth Gold IRA Eligibility

In 2026, single filers with a MAGI below the phase-out threshold can make a full Roth Gold IRA contribution. Once your income enters the phase-out range, your contribution limit begins to reduce proportionally. Once you exceed the upper limit of the phase-out range, you are completely ineligible to contribute to a Roth Gold IRA for that tax year.

One workaround that remains available in 2026 is the backdoor Roth IRA conversion, making a non-deductible Traditional IRA contribution and then immediately converting it to a Roth. This strategy requires careful execution to avoid the pro-rata rule triggering unintended taxes, and it’s worth coordinating with a tax advisor before proceeding.

Traditional Gold IRA Deductibility Based on Income

If neither you nor your spouse participates in a workplace retirement plan, your Traditional Gold IRA contributions are fully deductible regardless of your income level. This is a significant advantage for self-employed investors or those whose employers don’t offer retirement benefits.

If you are covered by a workplace plan, your deduction begins to phase out once your MAGI crosses the IRS threshold for your filing status. Contributions above the deductible limit can still be made as non-deductible Traditional IRA contributions, but you’ll want to track your cost basis carefully using IRS Form 8606 to avoid being taxed again on that money at distribution.

One important planning note: even if your contribution isn’t deductible, the gold held inside the account still grows tax-deferred until withdrawal. That continued shelter from annual capital gains taxes on precious metals, which are typically taxed at the higher collectibles rate of 28% when held outside an IRA, is a meaningful advantage even without the upfront deduction.

Getting clarity on your MAGI position before the contribution deadline is one of the most impactful steps you can take before year-end. Running the numbers with a tax professional in Q3 or Q4 gives you time to adjust contributions, execute a conversion, or explore alternative strategies before the window closes.

How to Execute a Gold IRA Rollover in 2026

The actual mechanics of a Gold IRA rollover are straightforward when you follow the right sequence. Most rollovers from a 401(k) to a Gold IRA take approximately 2 to 3 weeks from initiation to completion, longer than a standard IRA-to-IRA transfer because the 401(k) plan administrator, your employer, and the new custodian all need to coordinate. Knowing each step in advance prevents delays and costly mistakes.

Here is the complete process as it stands in 2026:

1. Choosing a Reputable Gold IRA Company

Your Gold IRA company is not the same as your custodian; it is the dealer that guides you through the process, helps you select IRS-approved metals, and connects you with a custodian and depository. Choosing the right one upfront saves you from costly mistakes later.

Look for companies with long operating histories, transparent fee structures, and strong third-party reviews. A company that pressures you into making a quick decision or upsells you into rare or collectible coins is a red flag; collectibles are not IRS-approved for Gold IRAs and can disqualify your account.

Augusta Precious Metals is one example of an established precious metals provider that helps investors navigate the Gold IRA process, offering IRS-approved coins and bars along with educational resources for beginners who are just getting started with precious metals retirement planning.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get started.

2. Choose an IRS-Compliant Self-Directed IRA Company

Not every IRA company supports physical precious metals. You need a self-directed IRA (SDIRA) custodian that is specifically authorized to hold alternative assets, including gold bullion. Verify that your chosen company works with a custodian that is IRS-approved and has established relationships with IRS-compliant depositories. Review their ratings on the Better Business Bureau (BBB), Trustpilot, and Google before committing.

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, lifelong customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Initiate a Direct Rollover From Your 401(k) Administrator

Contact your current 401(k) plan administrator and request a direct rollover to your new Gold IRA custodian. Specifically request that the distribution check be made payable to your new custodian, not to you personally. This single instruction is what prevents the mandatory 20% federal withholding from reducing your transfer amount.

Your new custodian will typically provide a rollover request letter or transfer form that you submit to your 401(k) administrator to initiate the process. Keep copies of every document submitted and follow up within 5 to 7 business days if you have not received confirmation of the transfer in progress.

4. Select IRS-Approved Metals and an Approved Depository

Once funds arrive in your new self-directed IRA, you direct your custodian to purchase specific IRS-approved metals on your behalf. Your custodian executes the purchase and arranges for direct shipment to an approved depository; you never take physical possession of the metals during this stage. Confirm the specific coins or bars you’re purchasing meet IRS purity standards before the order is placed, and request written confirmation of depository assignment and storage allocation once the transaction clears.

5. Confirm Regulated Storage and Receive Account Documentation

Once your metals have been purchased and delivered to the approved depository, request written confirmation from both your custodian and the depository facility.

This documentation should include the specific metals held, their weight and purity, your account number, and the storage allocation type, either segregated (your metals stored separately from other clients’ holdings) or commingled (stored together with other clients’ equivalent holdings). Segregated storage costs more but provides cleaner asset identification, which matters significantly at distribution time.

The Bottom Line on Gold IRA Rollover Rules in 2026

The rules governing Gold IRA rollovers in 2026 reward investors who understand the mechanics and penalize those who don’t. A direct rollover executed correctly costs you nothing in taxes or penalties and preserves every dollar of your retirement savings for precious metals acquisition. An indirect rollover mishandled by a single day, or a check made payable to you instead of your custodian, can wipe out years of tax-advantaged growth in a single transaction.

The contribution limits, SECURE Act 2.0 distribution rules, IRS-approved metals requirements, and MAGI phase-out thresholds are all working parts of the same system. Each one interacts with the others, which is why a piecemeal understanding of these rules is genuinely dangerous. The investors who are positioning themselves most effectively in 2026 are treating their Gold IRA as an integrated component of a broader retirement architecture, not as a standalone product.

Know your rollover type. Verify your metals. Choose a custodian with a verified compliance record. Confirm your storage. And if any step in that process is unclear, get it answered before you move a single dollar, because in the world of IRS retirement regulations, the cost of a mistake is always higher than the cost of asking the right question in advance.

If you are ready to explore how physical precious metals can strengthen your retirement strategy, Augusta Precious Metals offers a full range of IRS-approved gold and silver products along with expert guidance to help you build a Gold IRA that works for your long-term goals.

Frequently Asked Questions

The most common questions about Gold IRA rollovers in 2026 center on tax treatment, timing rules, product eligibility, and contribution limits. Here are the answers to the questions investors ask most, answered directly, without the usual industry hedging.

Can I Roll Over My Entire 401(k) Into a Gold IRA Without Paying Taxes?

Yes, provided you execute a direct rollover from your 401(k) plan administrator to your new Gold IRA custodian. In a direct rollover, the funds transfer between institutions without ever touching your hands, which means no taxable distribution is triggered and no 20% federal withholding is applied. The full balance of your 401(k) arrives intact in your new self-directed IRA.

The tax-free treatment applies regardless of the dollar amount being transferred, and the rollover does not count toward your annual IRA contribution limit. The key is ensuring the distribution check is made payable to your new custodian, not to you personally. If the check comes to you, the 20% withholding kicks in automatically and you’re on the clock for the 60-day redeposit window.

What Happens If I Miss the 60-Day Indirect Rollover Deadline?

Missing the 60-day deadline on an indirect rollover converts your rollover into a taxable distribution. The full amount of the distribution is added to your ordinary income for that tax year, and if you’re under age 59½, a 10% early withdrawal penalty is applied on top of the income tax owed. There is no standard grace period, and the IRS grants waivers only in very specific hardship circumstances, such as medical emergencies, natural disasters, or financial institution errors. The simplest way to eliminate this risk is to use a direct rollover instead.

How Many Times Per Year Can I Roll Over Into a Gold IRA?

The IRS’s one-rollover-per-year rule applies specifically to indirect (60-day) rollovers between IRAs. You are limited to one indirect rollover per 12-month period across all your IRA accounts combined, not per account. If you execute a second indirect IRA-to-IRA rollover within the same 12-month window, the second rollover is treated as a taxable distribution.

Direct rollovers and trustee-to-trustee transfers are not subject to this limitation. You can execute an unlimited number of direct rollovers or direct transfers in a given year without triggering the one-rollover rule. This is another reason why direct rollovers are the preferred mechanism; they give you flexibility to move funds multiple times within a year if your strategy requires it.

The 12 months are measured from the date you received the funds in the indirect rollover, not from January 1 of the calendar year. So if you received an indirect rollover distribution on March 15, 2026, you cannot initiate another indirect IRA-to-IRA rollover until March 16, 2027.

Does a Gold IRA Rollover Count Toward My Annual Contribution Limit?

No. A rollover, whether direct or indirect, does not count toward your annual IRA contribution limit. The IRS treats rollovers as transfers of existing retirement funds, not as new contributions. This means you can roll over $50,000, $200,000, or your entire 401(k) balance into a Gold IRA in 2026 without affecting your ability to also make a separate annual contribution of up to $7,500 (or $8,600 if you’re 50 or older) to that same account or another IRA.

This distinction is one of the most valuable aspects of the rollover mechanism. It allows investors approaching retirement to consolidate large employer-sponsored plan balances into a self-directed Gold IRA while simultaneously continuing to make regular annual contributions, maximizing both the transfer efficiency and the ongoing tax-advantaged accumulation potential of the account.

The one exception worth noting is a Roth conversion, which is treated differently from a rollover for tax purposes. Converting a Traditional Gold IRA balance to a Roth Gold IRA triggers ordinary income tax on the converted amount in the year of conversion, but it also does not count as a contribution toward the annual limit. Roth conversions have no dollar cap, giving high-income investors a pathway to Roth Gold IRA accumulation that bypasses the standard income eligibility restrictions.

Click the banner below to access these calculators and start protecting your wealth today.

Sources:

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Investments in collectibles in individually directed qualified plan accounts: IRS.gov

Leave a Reply