Quick Summary

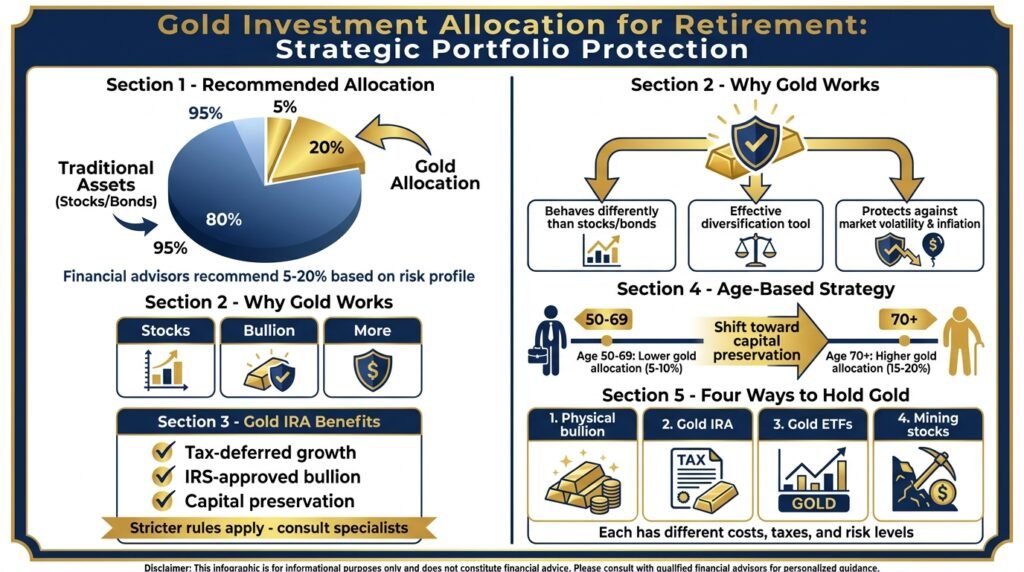

- Most financial advisors recommend allocating between 5% and 20% of your retirement portfolio to gold, depending on your risk profile and timeline.

- Gold behaves differently from stocks and bonds, making it one of the most effective diversification tools available to retirees.

- A Gold IRA offers tax-deferred growth using IRS-approved bullion, but the rules are stricter than most people realize.

- Your ideal gold allocation should shift as you age, with retirees 70 and older often benefiting from a higher weighting toward capital preservation.

- There are four distinct ways to hold gold in a retirement portfolio, each with different cost structures, tax treatments, and risk levels.

Gold isn’t just a shiny metal; it’s one of the most time-tested tools for protecting retirement wealth when everything else starts to wobble.

For retirees and pre-retirees navigating market uncertainty, rising inflation, and decades of living expenses ahead, knowing how to use gold strategically can mean the difference between a comfortable retirement and one spent hoping the market recovers in time.

Augusta Precious Metals specializes in helping everyday investors understand exactly how precious metals fit into a long-term financial plan, and the gold IRA guide pulls from that same practical, no-nonsense approach to owning physical gold in a tax-advantaged way.

Table of Contents

- Quick Summary

- Gold Belongs in Your Retirement Portfolio: Here’s Exactly How Much

- How Your Risk Profile and Age Determine Your Gold Allocation

- Gold as a Hedge Against Inflation and Currency Risk

- The Right Gold Allocation Comes Down to Your Specific Situation

- Frequently Asked Questions

Gold Belongs in Your Retirement Portfolio: Here’s Exactly How Much

The debate isn’t really whether gold belongs in a retirement portfolio. It’s how much. Get that number wrong in either direction, too little, and you’re exposed; too much, and you’ve sacrificed growth, and your retirement security takes a real hit.

The 5-20% Rule Most Financial Advisors Recommend

Most financial advisors recommend keeping between 5% and 20% of your retirement portfolio in gold, with the sweet spot for most people landing around 10% to 15%. Some recent analysis has pointed to an optimal allocation closer to 18% for retirees without a pension, specifically because gold offsets the absence of guaranteed income. The range is wide because personal factors, age, income needs, existing assets, and risk tolerance all pull the number in different directions.

For a retiree with a solid pension and Social Security covering core expenses, 5% to 10% in gold may be plenty. For someone relying entirely on a self-managed portfolio to fund 25 or 30 years of retirement, pushing toward 15% to 20% is a reasonable defensive move. The key is that no single number fits everyone, and adjusting over time is just as important as the initial allocation.

Why Gold Behaves Differently Than Stocks and Bonds

Gold has a low or negative correlation with stocks and bonds, which is the technical way of saying it tends to move independently — and often in the opposite direction during market stress. When equity markets dropped sharply during the 2008 financial crisis, gold prices climbed. When inflation surged in the 1970s and again in the early 2020s, gold held and grew its purchasing power while fixed-income investments lost ground in real terms.

This independence is what makes gold genuinely useful in a portfolio rather than just a feel-good hedge. Adding an asset that doesn’t move in lockstep with your other holdings reduces overall portfolio volatility without necessarily reducing long-term returns — a powerful combination for anyone who can’t afford to ride out a multi-year market correction.

How Gold Protects Purchasing Power Over Decades

Inflation is the slow leak in any retirement plan. A 3% annual inflation rate cuts your purchasing power nearly in half over 25 years. Retirees living on fixed income streams feel this erosion directly — the same dollar buys fewer groceries, less healthcare, less of everything over time.

Gold has historically maintained its purchasing power over long periods, even when paper currencies have not. This isn’t about gold making you rich — it’s about gold keeping you whole. For a retiree facing a 20 to 30-year time horizon, even a modest allocation to gold helps offset what inflation quietly takes away year after year.

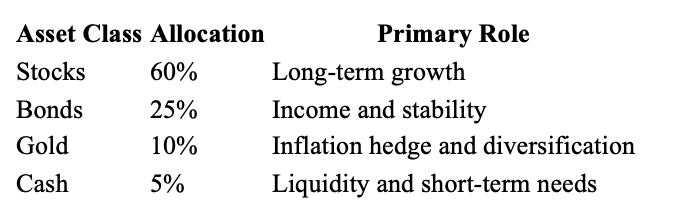

Here’s a simple look at how a balanced retirement portfolio might be structured with gold included:

How Your Risk Profile and Age Determine Your Gold Allocation

Your risk tolerance isn’t just about how you feel about market swings, it’s about how much volatility your retirement income can actually absorb. Someone with a pension, Social Security, and rental income can afford to be aggressive with their investment portfolio. Someone living entirely off their savings cannot. That difference shapes everything, including how much gold makes sense.

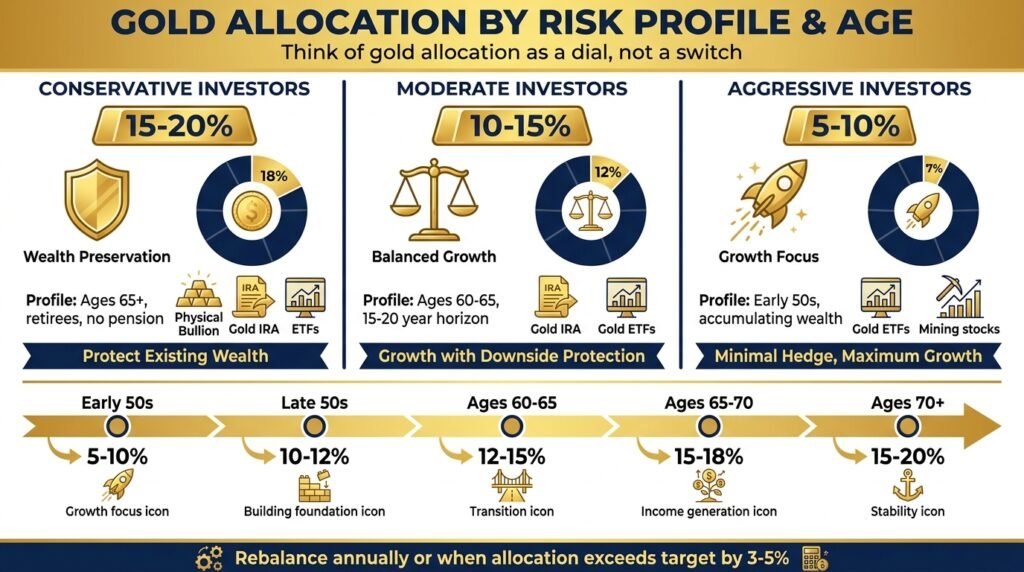

Think of gold allocation as a dial, not a switch. You’re not choosing between having gold or not; you’re choosing how loud to turn it up based on your specific financial picture.

Conservative Investors: 15-20% Allocation for Wealth Preservation

Conservative investors, typically those who prioritize not losing money over growing it, tend to benefit most from a higher gold allocation. A 15% to 20% weighting in gold provides meaningful protection against both market downturns and inflation without requiring the investor to time the market or take on equity risk they’re not comfortable with.

A practical example: a 70-year-old retiree without a pension, living on portfolio withdrawals and Social Security, might hold 18% in gold split between physical bullion and a gold ETF. The rest of the portfolio sits in dividend-paying stocks and short-duration bonds. This structure prioritizes capital preservation while still generating income, exactly what a conservative retirement portfolio needs to do.

- Primary goal: Protect existing wealth from erosion

- Gold vehicles: Physical bullion, Gold IRA, gold ETFs

- Rebalancing frequency: Annually or when gold exceeds target by 3-5%

- Best suited for: Retirees 65+, no pension, high sensitivity to loss

Moderate Investors: 10-15% Allocation for Balanced Growth

Moderate investors want growth but aren’t willing to absorb large drawdowns. A 10% to 15% gold allocation gives this group meaningful downside protection while keeping the bulk of the portfolio in assets with stronger long-term return potential. This is the most common allocation range among retirees who still have a 15 to 20-year planning horizon.

For a 62-year-old with a mix of 401(k) assets, some bond exposure, and a moderate risk appetite, putting 12% into gold, split between a Gold IRA and gold ETFs, hits the right balance. It adds stability without sacrificing the growth potential needed to fund a long retirement.

Aggressive Investors: 5-10% Allocation as a Minimal Hedge

Aggressive investors who are comfortable with equity risk and have a longer time horizon typically use gold as a minimal hedge rather than a core holding. A 5% to 10% allocation is enough to provide some inflation protection and reduce portfolio correlation without meaningfully dragging down returns in a bull market.

This approach works well for investors in their early 50s who are still accumulating wealth and have time to recover from market downturns. The gold position essentially acts as an insurance policy — you hope you never need it, but you’re glad it’s there when you do.

Best suited for: Pre-retirees in their 50s, high risk tolerance, diversified income sources

Primary goal: Growth with a minimal safety net

Gold vehicles: Gold ETFs, gold mining stocks

Rebalancing frequency: Annually

How Age and Retirement Timeline Affect Gold Allocation

Early 50s: Still accumulating: use gold as a 5-10% hedge while growth assets do the heavy lifting

Late 50s: Begin building the foundation: shift toward 10-12% as retirement approaches

Ages 60-65: Transition phase: prioritize capital preservation, consider 12-15% allocation

Ages 65-70: Early retirement: income generation becomes critical, gold anchors the defensive side

Ages 70+: Late retirement: stability over growth, 15-20% may be appropriate depending on income sources.

The Best Ways to Hold Gold in a Retirement Portfolio

Not all gold is created equal when it comes to retirement planning. The way you hold gold determines your tax treatment, liquidity, storage responsibilities, and overall cost. Each method has genuine advantages and real trade-offs that matter depending on your situation.

There are four main ways retirees hold gold, and many seasoned investors use a combination of two or more to balance the benefits of each.

Physical Gold: Coins, Bars, and Storage Considerations

Owning physical gold, whether American Gold Eagles, Canadian Maple Leafs, or gold bars, gives you direct, tangible ownership of the asset. There’s no counterparty risk, no fund manager, and no platform that can go bankrupt and take your holdings with it. For retirees who’ve lived through enough market crises to distrust financial institutions, physical gold has a particular appeal.

The trade-offs are real, though. Physical gold requires secure storage, either a home safe or a third-party vault, which adds ongoing costs. Selling it also takes more effort than clicking a button in a brokerage account. Premiums over spot price are common when buying coins and smaller bars, and you’ll want to work with a reputable dealer to avoid overpaying.

For IRS purposes, physical gold held outside a retirement account is classified as a collectible and taxed at a maximum capital gains rate of 28%, higher than the standard long-term capital gains rate for stocks. That tax difference is worth factoring into your allocation decisions.

Gold ETFs and Mutual Funds: Low-Cost Paper Exposure

Gold ETFs like the SPDR Gold Shares (GLD) and iShares Gold Trust (IAU) track the spot price of gold and trade on major stock exchanges just like shares of stock. They’re the most accessible and lowest-cost way to add gold exposure to a retirement portfolio, with expense ratios typically below 0.40%. You can hold them inside a traditional IRA, Roth IRA, or standard brokerage account without any special custodian requirements.

Gold Mining Stocks: Higher Risk, Higher Reward Potential

Gold mining stocks, companies like Newmont Corporation (NEM) and Barrick Gold (GOLD), give you leveraged exposure to gold prices. When gold rises 10%, a well-run mining company might see its stock climb 20% or more, because the profit margin expands faster than the underlying commodity price. That leverage cuts both ways, though; mining stocks can fall hard and fast when gold prices drop or when operational problems hit.

For retirement portfolios, gold mining stocks are best used as a small satellite position rather than a core gold holding. They introduce company-specific risk, management risk, and geopolitical risk that physical gold and ETFs simply don’t carry. If you’re going to use them, consider a gold miners ETF like the VanEck Gold Miners ETF (GDX) to spread that risk across multiple companies rather than betting on a single name.

Gold IRAs: Tax-Deferred Growth With IRS-Approved Bullion

A Gold IRA is a self-directed Individual Retirement Account that holds physical gold — but with strict IRS rules about what qualifies. The gold must meet a minimum purity of .995 fineness, must be stored in an IRS-approved depository (not your home), and must be held through a qualified custodian. Approved coins include the American Gold Eagle, American Gold Buffalo, and Canadian Gold Maple Leaf, among others.

The main benefit is tax treatment. Like a traditional IRA, contributions may be tax-deductible, and growth is tax-deferred until withdrawal. A Roth Gold IRA allows for tax-free growth if you meet the income requirements. Either way, a Gold IRA lets your gold position grow without annual tax drag, a significant advantage over a 20 to 30-year retirement horizon.

Your chosen Gold IRA company is not the same as your custodian; it is the dealer that guides you through the process, helps you select IRS-approved metals, and connects you with a custodian and depository. Choosing the right, one upfront saves you from costly mistakes later.

Look for companies with long operating histories, transparent fee structures, and strong third-party reviews. A company that pressures you into making a quick decision or upsells you into rare or collectible coins is a red flag; collectibles are not IRS-approved for Gold IRAs and can disqualify your account.

Augusta Precious Metals is one example of an established precious metals provider that helps investors navigate the Gold IRA process, offering IRS-approved coins and bars along with educational resources for beginners who are just getting started with precious metals retirement planning.

Click the banner below to visit Augusta’s official site and receive a free gold IRA guide. Fill out their short form to get started.

Gold as a Hedge Against Inflation and Currency Risk

Inflation and currency debasement are the two slow-moving threats that most retirement plans are least prepared for, and gold is one of the few assets specifically designed to counter both.

Understanding exactly how and when gold delivers on that inflation hedging promise helps you hold the position with conviction rather than second-guessing it every time a financial headline makes it look overpriced.

What History Shows About Gold During High Inflation Periods

During the high-inflation decade of the 1970s, gold prices surged from approximately $35 per ounce to over $800 per ounce by 1980, a gain that dramatically outpaced the inflation rate of that era. More recently, when U.S. inflation hit multi-decade highs in 2021 and 2022, gold maintained its purchasing power even as bonds lost significant real value.

The pattern isn’t perfect — gold doesn’t always move immediately with inflation data, but over multi-year periods of sustained inflation, its track record as a purchasing power preserver is well-established.

How Gold Performs When the U.S. Dollar Weakens

Gold is priced in U.S. dollars, which means when the dollar weakens against other currencies, gold prices in dollar terms typically rise. This inverse relationship isn’t a coincidence; it’s structural. As the dollar loses purchasing power relative to other currencies or relative to goods and services, the dollar price of gold adjusts upward to reflect the same underlying value. For retirees whose savings are denominated in dollars, gold provides a built-in counterweight to currency depreciation.

Key Relationship — U.S. Dollar vs. Gold:

• Dollar strengthens → Gold prices typically face short-term pressure

• Dollar weakens → Gold prices typically rise in dollar terms

• Federal Reserve expands money supply → Long-term upward pressure on gold

• Geopolitical uncertainty rises → Safe-haven demand pushes gold higher

• Real interest rates turn negative → Gold becomes more attractive vs. bonds

The Right Gold Allocation Comes Down to Your Specific Situation

There is no universally correct percentage of gold for a retirement portfolio, but there is a correct process for finding your number. Start with your income sources. If Social Security and a pension cover your basic living expenses, your investment portfolio can afford to take more risk and needs less gold.

If your portfolio is your only income source, the defensive allocation, including gold, needs to be more substantial. Layer in your age, your withdrawal timeline, your inflation sensitivity, and your tax situation, and the right allocation starts to take shape. For most retirees, that number lands somewhere between 10% and 20%, with the specific point within that range determined by the factors above.

What matters most is that your gold allocation is intentional, sized correctly for your situation, diversified across more than one form of gold ownership, held primarily inside tax-advantaged accounts, and rebalanced annually. Do those five things consistently, and gold will do exactly what it’s designed to do in a retirement portfolio: protect what you’ve built while everything else handles growth and income.

Learn how to own physical gold in a tax-advantaged way without the need or liability of storing the precious metal in your residence. Click the banner below to access Augusta Precious Metals’ free gold IRA guide on their official site. Fill out their short contact form to get started.

Click the banner below to receive a free gold IRA company integrity checklist from Augusta Precious Metals. Fill out their short contact form to get started.

Investment Minimums – Personal Considerations

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, life-long customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and a reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Frequently Asked Questions

Retirees and pre-retirees ask a consistent set of questions when they start thinking seriously about adding gold to their retirement strategy. The answers below reflect the practical reality of how gold actually behaves in a retirement context, not theory, not marketing, but the specific mechanics that matter when real money and real retirement security are on the line.

What percentage of my retirement portfolio should be in gold?

Most financial advisors recommend between 5% and 20% of a retirement portfolio in gold, with 10% to 15% being the most common range for moderate-risk retirees. Conservative retirees without guaranteed income sources like a pension often benefit from the higher end of that range, 15% to 20%, while aggressive investors with diversified income streams may be comfortable at 5% to 10%. The right number depends on your age, income needs, risk tolerance, and whether you’re still accumulating wealth or actively drawing it down.

Does gold actually protect against inflation in retirement?

Yes, over multi-year and multi-decade periods, gold has consistently maintained its purchasing power against inflation. During the 1970s-inflationary decade, gold dramatically outpaced the inflation rate. During the post-COVID inflation surge of 2021 and 2022, gold held value even as bond prices fell in real terms.

The protection isn’t perfect year-to-year — gold can lag inflation in the short term — but as a long-term store of purchasing power, its track record is stronger than most fixed-income alternatives. For retirees facing 20 to 30 years of inflation exposure, even a partial hedge through a 10% to 15% gold allocation meaningfully reduces the long-term erosion of buying power.

Is a Gold IRA better than buying physical gold directly?

Gold IRA vs. Physical Gold: Key Comparison

Tax Treatment: Gold IRA offers tax-deferred (traditional) or tax-free (Roth) growth; physical gold outside an IRA is taxed as a collectible at up to 28% on gains

Storage: A Gold IRA requires an IRS-approved depository; physical gold allows a home safe or private vault

Accessibility: Gold IRA withdrawals are subject to IRA rules and potential penalties before age 59½; physical gold can be accessed at any time

Setup complexity: Gold IRA requires a custodian, depository, and IRS-compliant bullion; physical gold can be purchased directly from a dealer

Annual costs: Gold IRA carries custodian and storage fees ($200–$500/year, typically); physical gold storage varies based on method

Best for: Gold IRA suits long-term tax-advantaged growth; physical gold suits investors who want direct access and no account structure

Neither option is universally better; they serve different purposes. A Gold IRA is the superior choice for long-term retirement savings where tax efficiency matters most. The tax-deferred growth over a 20 to 30-year retirement horizon can significantly compound the value of your gold position compared to holding it in a taxable account, where gains are hit at 28% each time you rebalance.

Physical gold held outside a retirement account makes sense as a complementary holding for retirees who want a portion of their gold to be immediately accessible without navigating IRA withdrawal rules. Think of it as the liquid emergency layer of your gold allocation — the portion you can convert to cash quickly and without account restrictions if an unexpected major expense arises.

For most retirees, the optimal approach is a combination: the bulk of the gold allocation held inside a Gold IRA for tax efficiency, with a smaller physical gold position held outside the account for direct access and liquidity. This split captures the tax advantages of the IRA structure while preserving the direct-ownership benefits that physical gold uniquely provides.

If you are ready to explore how physical precious metals can strengthen your retirement strategy, Augusta Precious Metals offers a full range of IRS-approved gold and silver products along with expert guidance to help you build a Gold IRA that works for your long-term goals.

Sources:

The Role of Gold in a Balanced Retirement Portfolio: A Strategic Guide

How Much Gold Should I Hold in My Retirement Portfolio?

Could Investing in Gold Add a New Dimension to Your Portfolio?

Leave a Reply