Quick Summary

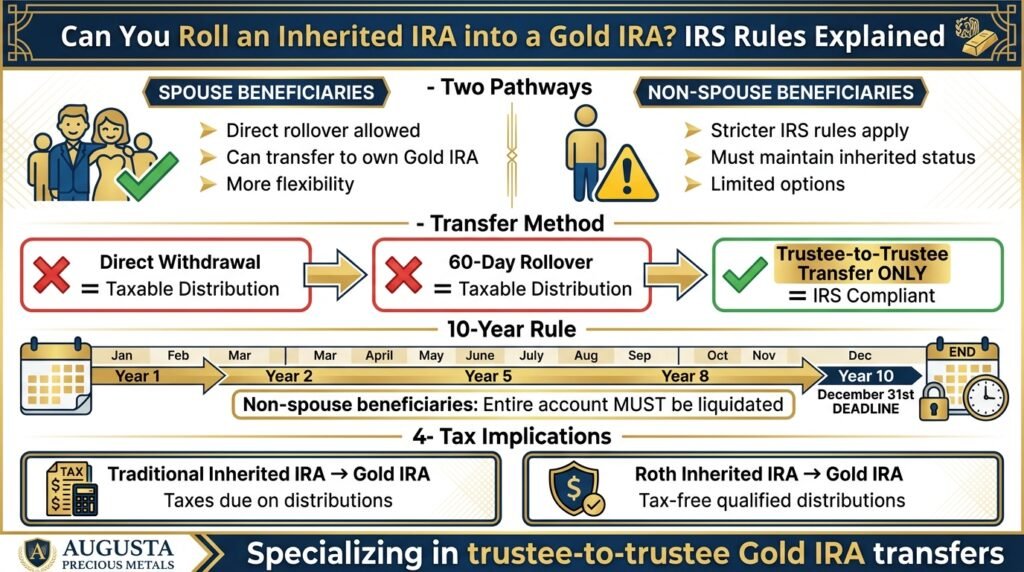

- Spouse beneficiaries can roll an inherited IRA directly into their own Gold IRA, while non-spouse beneficiaries must follow a stricter set of IRS transfer rules.

- The only IRS-compliant way to move inherited IRA funds is through a direct trustee-to-trustee transfer — doing it any other way risks treating the funds as a taxable distribution.

- Most non-spouse beneficiaries are locked into the 10-year rule, meaning the entire inherited account must be liquidated by December 31st of the 10th year after the original owner’s death.

- Augusta Precious Metals specializes in self-directed IRAs and can help beneficiaries navigate trustee-to-trustee transfers into alternative assets like gold.

- There’s a critical difference between what a traditional inherited IRA and a Roth inherited IRA mean for your tax bill when converting to a Gold IRA — and getting it wrong is expensive.

Inheriting an IRA and wanting to move it into gold is absolutely possible — but the rules are strict, and one wrong move can trigger a full taxable distribution.

When someone passes away and leaves you an IRA, what you’re allowed to do with those funds depends almost entirely on your relationship to the deceased and your classification as a beneficiary.

The IRS doesn’t treat all heirs the same, and the path to a Gold IRA rollover is very different depending on which category you fall into. Understanding these distinctions before you make any moves isn’t just smart — it’s essential for protecting the tax-advantaged status of the funds you’ve inherited.

Table of Contents

- Quick Summary

- Not Every Inherited IRA Can Be Rolled into a Gold IRA

- What a Gold IRA Actually Is

- The Only Legal Way to Move Inherited IRA Funds

- Required Minimum Distributions Still Apply to Inherited Gold IRAs

- Step-by-Step: How to Roll an Inherited IRA into a Gold IRA

- The Bottom Line on Inherited IRA to Gold IRA Rollovers

- Frequently Asked Questions

Not Every Inherited IRA Can Be Rolled into a Gold IRA

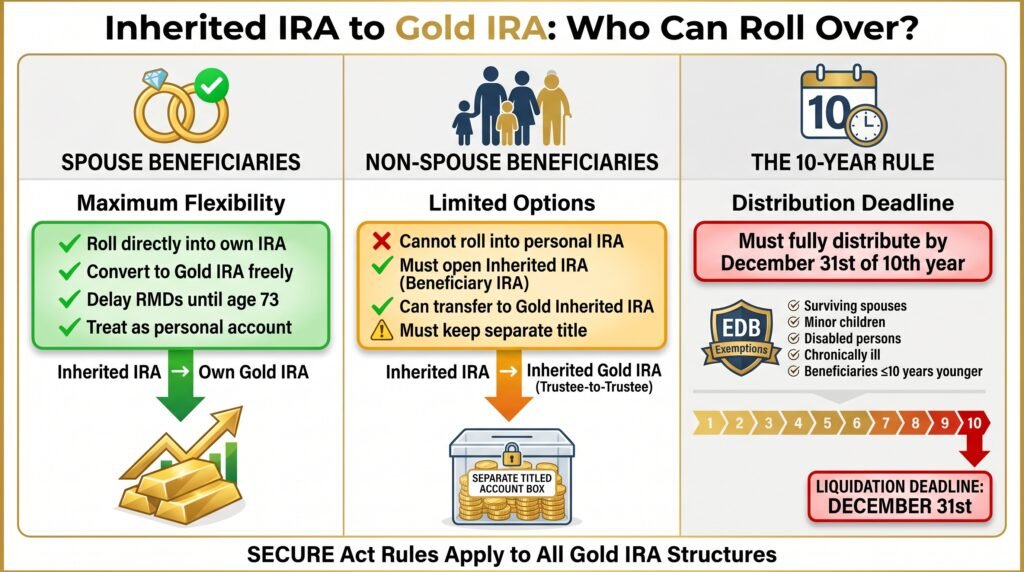

The foundational rule of inherited IRAs is simple but often misunderstood: you cannot treat an inherited IRA as your own unless you are the surviving spouse.

For every other beneficiary — children, siblings, non-married partners, trusts, or estates — the inherited funds must remain in a properly titled inherited IRA and cannot be commingled with your existing retirement accounts. This distinction shapes every decision you’ll make about transferring those funds into a Gold IRA. For people beginning their gold investment research, professional guidance is necessary to take the initial steps.

Why Spouse Beneficiaries Have the Most Options

A surviving spouse has a unique privilege under IRS rules — they can roll the inherited IRA directly into their own IRA, including a self-directed Gold IRA. This means the surviving spouse can delay required minimum distributions (RMDs) until they reach age 73, continue growing the assets tax-deferred, and treat the account exactly as if they had contributed to it themselves.

No other beneficiary category gets this level of flexibility. For a spouse, converting a traditional inherited IRA into a self-directed Gold IRA follows essentially the same process as any standard IRA rollover.

What Non-Spouse Beneficiaries Can and Cannot Do

Non-spouse beneficiaries — which includes adult children, siblings, and most other heirs — cannot roll the inherited IRA into their own personal IRA. What they can do is open an inherited IRA (sometimes called a Beneficiary IRA) titled in the deceased’s name for their benefit, and then initiate a trustee-to-trustee transfer of those funds to a self-directed inherited IRA that holds gold and other IRS-approved precious metals. The account must always remain titled as an inherited IRA, never merged with personal retirement funds.

The 10-Year Rule That Affects Most Beneficiaries

The SECURE Act fundamentally changed the distribution landscape for most non-spouse beneficiaries. Unless you fall into the category of an Eligible Designated Beneficiary (EDB) — which includes surviving spouses, minor children of the deceased, disabled individuals, chronically ill individuals, and beneficiaries not more than 10 years younger than the deceased — you are subject to the 10-year rule.

This means the entire inherited IRA balance must be fully distributed by December 31st of the 10th year following the original account holder’s death. Even within a Gold IRA structure, this liquidation deadline still applies.

What a Gold IRA Actually Is

A Gold IRA is a self-directed individual retirement account that holds physical precious metals instead of — or in addition to — traditional paper assets like stocks and bonds.

The IRS permits certain gold, silver, platinum, and palladium products to be held within these accounts, but the metals must meet strict purity standards and be stored in an IRS-approved depository. You cannot take personal possession of the metals while they remain inside the IRA without triggering a distribution event.

The appeal of a Gold IRA as a destination for inherited retirement funds comes down to diversification and inflation protection. Physical gold has historically held value during periods of economic uncertainty, making it an attractive option for beneficiaries who want to preserve inherited wealth over time rather than liquidate it into cash immediately.

How a Self-Directed IRA Makes Gold Ownership Possible

Standard IRA custodians — the major banks and brokerage firms — typically only offer stocks, bonds, mutual funds, and ETFs. To hold physical gold inside an IRA, you need a self-directed IRA (SDIRA) with a custodian that specializes in alternative assets.

The custodian handles compliance, reporting, and coordinates with an IRS-approved depository where the physical metals are stored on your behalf. This three-party structure — you, the custodian, and the depository — is what keeps the account IRS-compliant.

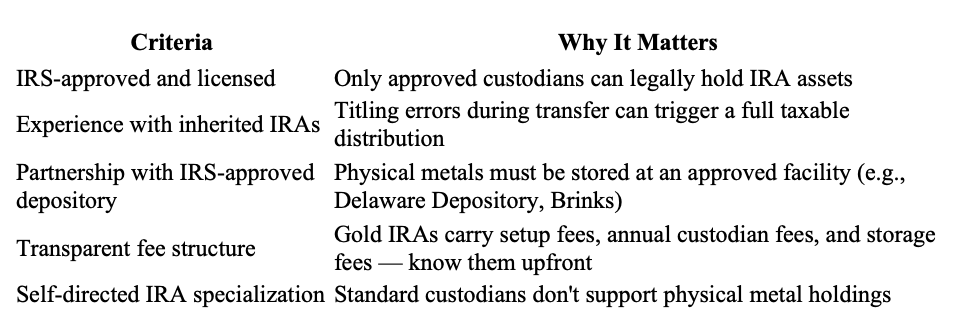

Choose a Reputable Gold IRA Custodian

This is the most important decision in the entire process. Your Gold IRA custodian is the IRS-approved entity that will hold your account, coordinate the transfer, and facilitate metal purchases. Look for custodians with verifiable track records, transparent fee structures, and experience specifically working with federal employees on TSP rollovers.

Be cautious of any company that pressures you to act fast, pushes numismatic or collectible coins with inflated markups, or is vague about storage arrangements and fees. Legitimate custodians never need to rush you. Avoid companies that suggest storing your Gold IRA metals at home; home storage of IRA-owned gold is not IRS-compliant and can result in full account disqualification.

Augusta Precious Metals is a leading and established gold IRA company that helps investors navigate the Gold IRA process, providing a combination of an ethics-centered approach to empower the customer, the best prices, superb customer service, and expert educational resources.

Click the banner below to visit Augusta’s official site and receive a free gold IRA company integrity checklist. Fill out their short form to get started.

The Only Legal Way to Move Inherited IRA Funds

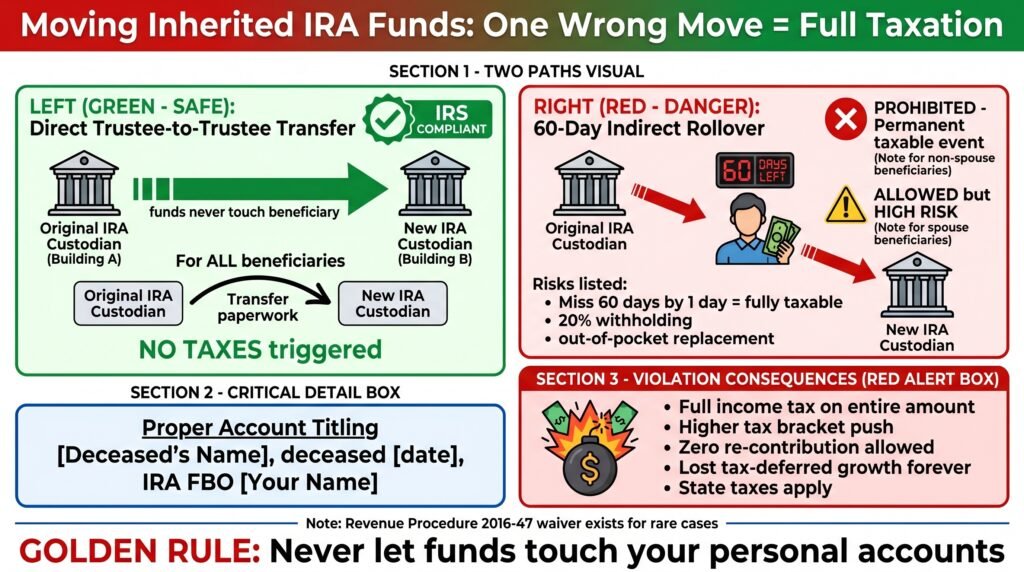

This is where many beneficiaries make costly mistakes. Because an inherited IRA operates under different rules than a standard IRA, the methods for moving those funds are more limited and must be executed precisely. Getting this step wrong doesn’t result in a warning — it results in the entire distribution being treated as taxable income in the year it occurs.

There are technically two ways funds can move from one IRA to another: a direct trustee-to-trustee transfer and an indirect rollover. For inherited IRAs held by non-spouse beneficiaries, only one of these options is truly safe.

Why a Trustee-to-Trustee Transfer Is the Safest Move

A direct trustee-to-trustee transfer means the funds move directly from the existing IRA custodian to the new Gold IRA company that works with a trusted custodian without the money ever passing through your hands. You initiate the transfer paperwork, the two parties coordinate the movement of assets, and the funds land in the new account without triggering a taxable event. For non-spouse beneficiaries especially, this is the only reliably IRS-compliant method.

The key detail is the account titling. The inherited IRA at the receiving custodian must be titled correctly — typically formatted as: “[Deceased’s Name], deceased [date of death], IRA FBO [Beneficiary’s Name].” If the account is titled incorrectly or the funds are deposited into a personal IRA instead of an inherited IRA, the IRS can treat the entire amount as a distribution subject to income tax.

Working with a gold IRA company experienced in inherited IRA transfers — rather than a standard retail brokerage — dramatically reduces the risk of titling errors or procedural missteps during this process.

The 60-Day Indirect Rollover Rule and Its Risks

An indirect rollover is when you take a distribution from the IRA and then re-deposit those funds into another IRA within 60 days. For surviving spouses rolling an inherited IRA into their own IRA, this is technically permitted. However, for non-spouse beneficiaries, the IRS explicitly prohibits indirect rollovers of inherited IRA funds. If a non-spouse beneficiary receives a distribution from an inherited IRA, that money cannot be re-contributed to any IRA — it is a permanent taxable event.

Even for spouses using the indirect rollover method, the risks are significant. Missing the 60-day window by even one day results in the distribution being fully taxable in that year. Additionally, if the inherited IRA was a traditional IRA, the distributing custodian may withhold 20% for federal taxes — meaning you’d have to make up that withheld amount out of pocket to complete a full rollover within the 60-day window, then wait to receive the withholding back as a tax refund.

The bottom line: unless you are a surviving spouse with a very clear reason to use the indirect method, a direct trustee-to-trustee transfer is the only move that makes practical and financial sense.

What Happens If You Violate IRS Transfer Rules

The IRS does not offer a grace period or a second chance when inherited IRA transfer rules are violated. The moment funds from an inherited IRA are distributed incorrectly — whether by being deposited into a personal IRA, withdrawn without proper rollover procedures, or handled through an indirect rollover as a non-spouse beneficiary — the IRS treats the entire amount as an ordinary distribution. That means the full value of the distribution is added to your taxable income for that year.

- Full income tax liability on the distributed amount in the year the violation occurs

- Potential to push you into a higher tax bracket if the inherited balance is substantial

- No ability to re-contribute the funds to any IRA once they’ve been improperly distributed

- Loss of all future tax-deferred growth on the distributed amount

- State income taxes may also apply on top of federal liability, depending on your state of residence

There is one narrow exception worth knowing. The IRS does have a self-certification waiver process under Revenue Procedure 2016-47 that may allow beneficiaries to claim a missed 60-day rollover deadline was due to a qualifying reason — such as a financial institution error or a serious illness. But this is not a guaranteed escape hatch, and it applies only in limited circumstances.

The simplest way to avoid all of this is to never let the funds touch your personal accounts. Instruct the custodians directly, confirm the transfer method in writing, and verify the account titling before any assets move.

Make sure you comply with all IRS rules concerning rollovers by accessing Augusta Precious Metals’ free gold IRA guide. Click the banner below to visit their official site and fill out their short contact form to get started today.

Required Minimum Distributions Still Apply to Inherited Gold IRAs

Moving an inherited IRA into a Gold IRA does not exempt you from required minimum distribution rules. The account structure changes, but the IRS distribution requirements follow the assets regardless of what they’re invested in. Whether your inherited IRA holds physical gold bars or index funds, the same RMD deadlines and calculations apply.

RMD Rules for Eligible Designated Beneficiaries

Eligible Designated Beneficiaries (EDBs) — surviving spouses, minor children of the account owner, disabled individuals, chronically ill individuals, and beneficiaries within 10 years of the deceased’s age — have more flexibility in how they take distributions. Surviving spouses who roll the inherited IRA into their own IRA can delay RMDs until they reach age 73. Other EDBs can generally stretch distributions over their own life expectancy, using IRS Single Life

Expectancy tables to calculate annual RMD amounts. This “stretch IRA” strategy allows the bulk of the account to remain invested — and in a Gold IRA context, to remain in physical metals — for a longer period.

RMD Rules for Non-Eligible Designated Beneficiaries

For most adult children and other non-EDB beneficiaries, the 10-year rule governs everything. The entire inherited Gold IRA balance must be fully distributed by December 31st of the 10th year after the original owner’s death. If the original account owner had already begun taking RMDs before death, the beneficiary must also take annual RMDs during years one through nine of the 10-year window — not just wait until year ten to withdraw everything.

This annual RMD requirement during the 10 years is a detail that catches many beneficiaries off guard, particularly because the IRS issued confusing guidance on this point in the years following the SECURE Act.

The penalty for missing an RMD is a 25% excise tax on the amount that should have been distributed — reduced to 10% if corrected within the correction window. In a Gold IRA, this means you’d need to liquidate a portion of your physical metal holdings each year to satisfy the distribution requirement, which adds a layer of planning complexity.

Step-by-Step: How to Roll an Inherited IRA Into a Gold IRA

The process of moving inherited IRA funds into a Gold IRA involves several distinct stages, each with its own compliance requirements. Skipping steps or rushing the process is how costly errors happen. Here’s exactly how it works from start to finish.

Before initiating anything, gather the original account holder’s death certificate, the IRA account statements, and any beneficiary designation documents on file with the current custodian. These will be required at multiple points in the transfer process.

1. Confirm Your Beneficiary Status and Eligibility

Your first step is confirming how you are classified under IRS rules — spouse, Eligible Designated Beneficiary, or non-eligible designated beneficiary. This classification determines which transfer methods are available to you, what the titling of your new inherited IRA must look like, and what distribution timeline you’re locked into. Contact the current custodian of the inherited IRA to confirm the account details and your designated beneficiary status on file.

If the estate or a trust is named as beneficiary rather than an individual, the rules become even more complex. Trust beneficiaries generally cannot roll over inherited IRA assets at all — funds must remain in the inherited IRA and can only be moved via trustee-to-trustee transfer to another custodian. A tax attorney or financial advisor with specific inherited IRA expertise is essential in these situations.

2. Find an IRS-Approved Gold IRA Custodian

What to look for in a Gold IRA custodian:

Not all gold IRA companies are created equal when it comes to inherited IRAs specifically. A custodian that handles standard IRA rollovers regularly may have little experience with the specific titling and transfer requirements that inherited accounts demand. Ask directly: “Have you processed trustee-to-trustee transfers for inherited IRAs into self-directed Gold IRAs before?”

Fees vary significantly across Gold IRA custodians. Setup fees typically range from $50 to $300, annual custodial fees from $75 to $300, and storage fees from $100 to $300 per year depending on whether you choose segregated or commingled storage at the depository. Segregated storage means your specific metals are stored separately from other clients’ holdings — this typically costs more but provides greater clarity on exactly what you own.

3. Open a Self-Directed IRA in Your Name

Once you’ve selected your Gold IRA company, you’ll open a new self-directed IRA account. These gold companies, such as Augusta Precious Metals, Birch Gold Group, National Gold Group, and others, work directly with custodians and facilitate the gold IRA rollover and storage process.

If you’re a non-spouse beneficiary, this account must be titled as an inherited IRA — not a standard IRA in your name. The typical titling format is: “[Deceased’s Full Name], IRA (deceased [date of death]), for the benefit of [Your Full Name].” Your new custodian should guide you through this titling precisely, but confirm it matches IRS requirements before signing anything.

You’ll complete new account paperwork with the Gold IRA company, provide identification, and designate your own beneficiaries for the inherited account. Once the account is officially open and titled correctly, you’re ready to initiate the transfer.

4. Initiate a Direct Trustee-to-Trustee Transfer

Contact the current custodian of the inherited IRA — the institution where the original account owner held the funds — and request a direct trustee-to-trustee transfer to your new self-directed inherited Gold IRA. Provide them with the new custodian’s account details, the exact account title, and any transfer authorization forms required. Most custodians require a medallion signature guarantee or notarized authorization for inherited IRA transfers, so confirm the documentation requirements early to avoid delays.

Do not request a distribution check made payable to you. Even if you intend to deposit it into the new Gold IRA, any check made payable to you personally is treated as a distribution the moment it’s issued, regardless of what you do with it afterward. The check — or wire transfer — must go directly from the original custodian to the new Gold IRA custodian.

5. Select Your IRS-Approved Gold Assets

Once the funds arrive at your new self-directed inherited Gold IRA custodian, you’ll work with them — and potentially a precious metals dealer they work with — to select which IRS-approved gold products to purchase.

Common choices include the American Gold Eagle (1 oz, ½ oz, ¼ oz, and 1/10 oz denominations), the American Gold Buffalo (99.99% pure), Canadian Gold Maple Leaf coins, and gold bars from approved refiners like PAMP Suisse or Credit Suisse in sizes ranging from 1 gram to 400 troy ounces. The custodian will coordinate delivery of the physical metals to the IRS-approved depository, where they’ll be held in your account’s name until you take a distribution.

Learn more about the IRA tax rules in more depth here

The Bottom Line on Inherited IRA to Gold IRA Rollovers

An inherited IRA can absolutely be moved into a Gold IRA — but only if you follow the IRS rules precisely, use a direct trustee-to-trustee transfer, choose a custodian experienced with inherited accounts, and maintain the correct account titling throughout the process.

Spouse beneficiaries have the most flexibility; non-spouse beneficiaries are bound by the 10-year rule in most cases, and the tax treatment of every distribution depends on whether the original account was traditional or Roth. The physical gold strategy can be a powerful way to preserve and grow inherited wealth — but only when executed correctly from the very first step.

Frequently Asked Questions

Here are the most common questions beneficiaries have when considering moving inherited IRA funds into a Gold IRA.

Can a non-spouse beneficiary roll an inherited IRA into a Gold IRA?

Yes — but with important restrictions. A non-spouse beneficiary cannot roll inherited IRA funds into their own personal IRA. Instead, they must open a properly titled inherited IRA (also called a Beneficiary IRA) with a self-directed custodian that supports gold holdings, and transfer the funds via a direct trustee-to-trustee transfer. The account must always remain titled as an inherited IRA in the deceased’s name for the benefit of the beneficiary, and the 10-year liquidation rule still applies. The funds can be invested in IRS-approved physical gold within that inherited IRA structure for the duration of the distribution period.

Is there a penalty for missing the 60-day rollover window?

Yes — and it’s severe. If a surviving spouse uses the indirect rollover method and misses the 60-day redeposit deadline, the entire distributed amount is treated as ordinary income for that tax year. There is no partial forgiveness.

The IRS does have a narrow self-certification process under Revenue Procedure 2016-47 that may apply if the missed deadline was caused by a qualifying event — such as a financial institution error, a serious illness, or a natural disaster — but this is not guaranteed relief. For non-spouse beneficiaries, the 60-day indirect rollover option doesn’t exist at all — any distribution from an inherited IRA by a non-spouse is permanently taxable and cannot be re-contributed to any IRA, period.

Do I still have to take RMDs from an inherited Gold IRA?

Yes. Transferring an inherited IRA into a Gold IRA does not change or suspend your RMD obligations. The type and timing of RMDs depend on your beneficiary classification. Eligible Designated Beneficiaries, including surviving spouses and certain other qualifying individuals, can take distributions over their life expectancy.

Most other beneficiaries — including adult children — are subject to the 10-year rule, which requires full liquidation of the account by December 31st of the 10th year after the original owner’s death. If the original owner had already begun taking RMDs before death, non-EDB beneficiaries must also take annual RMDs during years one through nine of the 10-year window. Missing an RMD triggers a 25% excise tax on the amount that should have been distributed, reduced to 10% if corrected within the IRS correction window.

If you’re ready to explore your options for an inherited IRA to Gold IRA transfer, click the banner below to visit Augusta’s official site and receive a free gold IRA company guide. Fill out their short form to get started.

Augusta Precious Metals provides step-by-step guidance on rollovers, custodian selection, and IRS-compliant precious metals investing tailored specifically for government workers and uniformed service members.

Investment Minimums – Personal Considerations

Certain IRA companies have higher investment minimums than others. If you are a serious investor with a minimum of $50,000, you can take advantage of Augusta Precious Metals’ higher competitive prices, life-long customer service, and educational resources.

If you require a lower barrier to entry, both National Gold Group and Birch Gold Group are trustworthy companies that provide a $10,000 investment minimum.

National Gold Group provides exceptional price transparency and reliable buyback commitment. Birch Gold Group is one of the most established and trusted gold IRA companies, spanning over 20 years, and provides some of the lowest fees in the industry.

Decide which gold IRA company works for you by clicking the banners below and accessing their free gold IRA guide. Fill out their short contact form to get started.

Birch Gold Group: Best Gold IRA for Established Trust & Low Fees

National Gold Group: Best Gold IRA for Transparency & Buyback

Sources:

Gold IRA Rules and Regulations: LendEDU

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Investments in collectibles in individually directed qualified plan accounts: IRS.gov: Retirement plans FAQs regarding IRAs: IRS.gov

Transform Your TSP into a Secure Gold Investment – FedPilot

Gold IRA storage rules: IRS requirements for storing precious metals: Yahoo!Finance

Leave a Reply