Quick Summary

Gold isn’t behaving like a traditional “safe haven” during the current war and oil shock. Prices can fall—even during crises—because gold is driven by liquidity, interest rates, and global capital flows, not just fear.

A surge in oil prices is fueling inflation and higher interest rates, which hurts gold since it doesn’t produce yield. Central banks and countries may sell gold to cover economic stress, reducing demand and pushing prices down.

Gold still has a long-term role as a hedge, but short-term performance can be volatile and counterintuitive. Depending on the duration of the conflict and the level of central bank support in the form of monetary easing and money supply expansion will dictate the longer term price action of gold.

Introduction

Is gold still worth it? Like all things, it’s all about timing and context.

“One of the strongest arguments for gold is that it acts as a hedge against geopolitical instability, wars, fragmentation, and loss of trust between countries.

In those environments, investors look for assets that aren’t tied to any one government, and gold fits that role. It’s a neutral asset.

But what’s interesting, and often misunderstood, is that gold doesn’t just go up every time there’s a crisis.

You can actually see situations where geopolitical tensions rise, and gold initially spikes… but then either levels off or even declines.

And that’s because gold isn’t just reacting to fear; it’s mainly reacting to variables like interest rates, the dollar, liquidity, and the world central bank’s reaction to the conflict.

So even if a conflict increases uncertainty, if it also leads to higher real rates or a stronger dollar, that can offset or even overwhelm the bullish impact on gold.

Which means the relationship between geopolitics and gold is real, but it’s not simple, and it’s definitely not one-directional.”

The recent events of March 2026 perfectly illustrate this exact point:

- Gold initially surged when the Middle East conflict escalated.

→ Early reaction: safe-haven buying. - But then gold fell sharply despite the ongoing war. Down 13–15% after the conflict began

- Why? Because:

- Rising oil → higher inflation expectations. But not Monetary inflation,

- Central banks stay tighter with higher rates.

- This leads to a Stronger dollar plus higher real yields

- This leads to downward Pressure on gold.

Geopolitics alone doesn’t drive gold. Macro conditions determine whether the move sticks.

“Gold doesn’t just trade on fear — it trades on the macro response to that fear.”

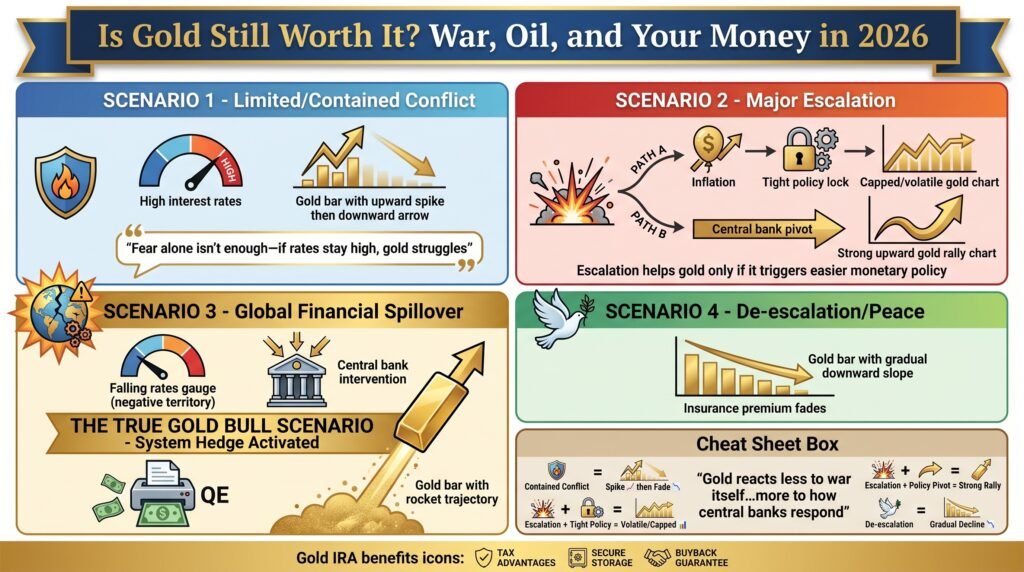

Scenario 1 – Limited / Contained Conflict

What happens:

- Conflict remains regional with no major escalation.

- Markets initially react with fear and then normalize.

- Oil may spike briefly, then stabilize.

Macro response:

- Central banks stay cautious or slightly hawkish.

- Real rates remain stable or slightly elevated.

- USD stays relatively strong.

🪙 Gold reaction:

- Initial spike due to safe-haven demand.

- Then plateaus or pulls back.

“Fear alone isn’t enough — if rates stay high, gold struggles.”e to that fear.”

Scenario 2 – Major Escalation – Regional War Expansion

What happens:

- Broader Middle East involvement.

- Oil supply disruption is leading to a sharp spike in energy prices.

- Global uncertainty increases significantly.

Macro response leads to two possible paths…

Path A – Inflation Shock plus Tight Policy

- Oil-driven inflation rises.

- Central banks stay tighter for longer.

- Real rates rise or stay elevated.

👉 Gold Outcome..

- Short-term surge.

- Then suppressed or volatile.

Path B: Crisis leads to a Central Bank Policy Pivot.

- Growth slows sharply.

- Financial stress emerges.

- Central banks cut rates and inject liquidity.

👉 Gold Outcome:

Sustained a strong rally.

Escalation helps gold only if it leads to easier monetary policy. The easing essentially increases the monetary supply, leading to inflation.

Scenario 3 – Global Financial Spillover – This is the true “gold bull” scenario.

What happens:

- War triggers:

- Banking stress.

- Credit tightening.

- Market instability.

Macro response:

Real rates fall (or go negative).

Central banks intervene aggressively.

Liquidity increases through QE or money printing.

🪙 Gold reaction:

- Strong, sustained upside.

🎯 Key takeaway:

This is where gold behaves exactly as advertised, as a system hedge.

Scenario 4 – De-escalation – A Sustained Peace Resolution.

What happens:

- Tensions ease.

- Oil prices fall.

- Risk sentiment improves.

Macro response:

- Inflation expectations decline.

- Real rates may stabilize or rise.

- Risk assets outperform.

Gold reaction:

- Gradual decline or underperformance.

Key takeaway:

Gold loses its “insurance premium” when fear fades.

A Simplified Cheat Sheet.

- A contained conflict equals Gold Spike, then fades.

- An escalation with tight monetary policy equals a volatile and capped gold price.

- An escalation with a tight monetary policy pivot equals a strong rally for gold.

- De-escalation of conflict equals a gradual decline and evening out of the gold price.

Whichever of these scenarios is likely will largely depend on the duration and the amount of liquidity and national debt resulting from money supply growth.

“Gold reacts less to the war itself… and more to how central banks respond to it.”

To take advantage of the volatility of gold and silver before their eventual resurgence.

Gold and silver IRAs are a tax-advantaged means of owning physical gold with the need or potential liability of storing the precious metal in your own residence. Gold IRA companies provide competitive price matches, lifetime customer service, secured storage, and solid buyback guarantees for their clients.

Augusta Precious Metals is a gold IRA company with over a decade in the industry of providing account rollover services. Augusta is one of the leading gold investing companies for trust, customer empowerment, and prices.

Click the banner below to receive a free gold IRA integrity checklist from their official site. Fill out their sort contact form to get started.

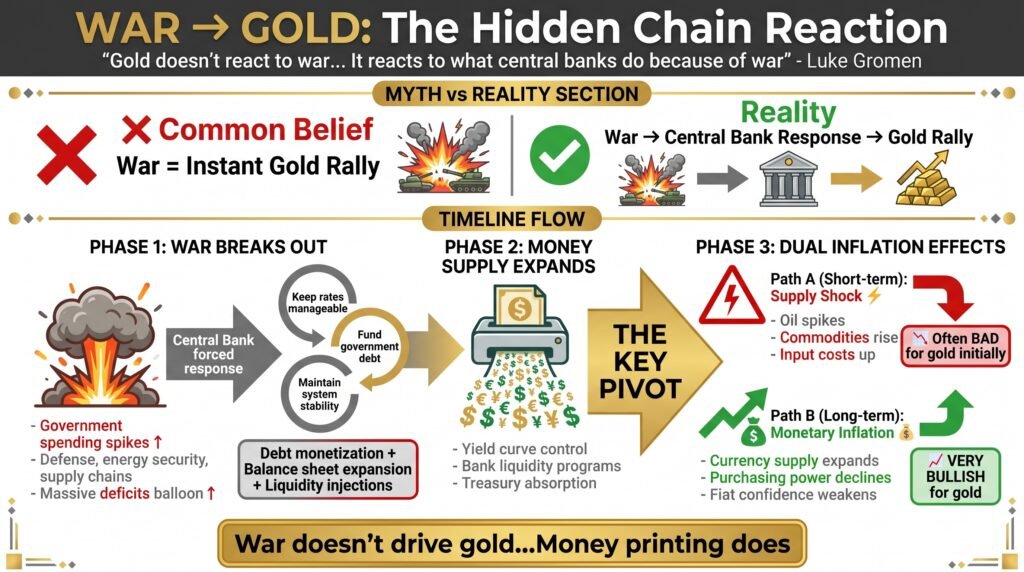

Why War Doesn’t Immediately Send Gold Higher

Many investors think war automatically sends gold higher.But that’s not actually how it works.

According to a macro investor named Luke Gromen: Gold doesn’t react to war…It reacts to what central banks do because of war.

Here’s the chain reaction:

War breaks out, governments spend massively, and deficits explode. Now, central banks have a problem: They can’t let interest rates rise too much…

Or the system breaks under the debt.

So, what do they do? They step in, add liquidity, and expand the money supply.

But here’s the part most people miss: At first, war pushes oil higher, which drives inflation, which keeps the central bank’s monetary policy tight, so gold might actually stall or even drop early on.

The real move happens later. When markets realize: Central banks have to ease…and money supply starts expanding. That’s when gold tends to break out in a big way.

So, the takeaway is simple: War doesn’t drive gold…Money printing does.

Phase 1, War Breaks Out, and Central Banks Are Forced to Respond

When global conflict escalates, Governments increase spending on: Defense, Energy security, Supply chains, and Alliances to provide aid. This creates large fiscal deficits

According to Gromen, central banks don’t operate independently in these scenarios.

They are effectively forced to:

- Keep interest rates from rising too much.

- Ensure government debt remains fundable.

- Maintain financial system stability.

👉 This often leads to:

- Debt monetization, direct or indirect.

- Balance sheet expansion.

- Liquidity injections.

Phase 2 – Money Supply Expands

This is the key pivot – War leads to deficits, then monetization and the resulting money printing.

Even if not explicit Q.E., it can show up as: Yield curve control, implicit. The creation of Bank liquidity programs and/ or Treasury issuance is absorbed by the system.

Phase 3 – Downstream Inflation Effects

This creates two layers of inflation:

1. Immediate – Supply Shock.

- Oil spikes.

- Commodity prices rise.

- Input costs increase.

👉 This is oil-driven inflation. Often bad for gold in the short term.

2. Secondary – Monetary Inflation.

- Currency supply expands.

- Real purchasing power declines.

- Confidence in fiat weakens.

👉 This is monetary inflation, which is very bullish for gold.

To get started on your gold investing journey by obtaining a free investment guide from one of the gold IRA companies below. Whether you require a company with a low investment minimum to gets started or are a serious investor with a larger portfolio to protect, a tax-advantaged gold IRA is a great vehicle to own physical gold without the need or liability of storage within your own home.

Click the right banner for your individual needs. Fill out their short contact form on their site to get started.

Gold’s Role and Timeline of Gold Reaction

Gold doesn’t respond to the war itself, it responds to the policy response to the war.

Phase 1: Shock.

- War begins.

- Oil spikes.

- Rates expectations rise.

👉 Gold is volatile and mixed.

Phase 2: Policy Constraint

- Governments can’t afford high rates.

- Financial stress builds.

👉 Markets begin to anticipate:

- Intervention.

- Liquidity support.

👉 Gold starts to stabilize.

Phase 3: Monetary Expansion

- Central banks ease – explicitly or implicitly.

- Money supply grows.

👉 Gold = strong, sustained rally.

“Gold is driven by real rates, liquidity, and macro response — not just geopolitics.”

Gromen’s view is essentially the endgame of that logic:

- Geopolitics forces policy.

- Policy drives liquidity.

- Liquidity drives gold.

Tie-In to Gold–Oil Ratio – A Critical Connection

This is where it all clicks:

Early War Phase:

- Oil rises in price.

- Gold rises, but not as much as oil.

The Ratio falls, Gold appears weak.

Later Phase (Gromen Scenario):

- Money supply rises.

- Real rates are down.

- Gold increases.

- Oil stabilizes or falls.

Ratio rises, True gold bull phase begins.

Conclusion

In summary, Gromen’s Big Macro Bet, if you condense his view:

The U.S. and global system cannot sustain: High debt, High rates, AND geopolitical conflict. Something has to give…And that “something” is: Currency value declines due to money supply expansion

Again, “War doesn’t just create inflation — it forces the system to print, and that’s when gold really moves.

Another factor, the geopolitical fallout of the large US military interventions and the resulting divestment in the dollar as a result play into the bullish case for gold.

With increasing geopolitical tensions, the desire by world governments and central banks to seek a neutral asset that does not carry the same counterparty risk as the US dollar will become more and more a priority. Only time will tell.

But waiting is not an option as an investor. Preparation is. And one rule has remained true and constant over 5,000 years: gold has never gone to zero. Currencies have.

To take advantage of the volatility of gold and silver before their eventual resurgence, see the links below to obtain a free guide from either Birch Gold Group or Augusta Precious Metals. Fill out their short contact form on their site to get started.

Best Gold IRA for Low Investment Minimums and Fees

Best Gold IRA for Prices, Customer Support, & Education

Frequently Asked Questions

Is gold still a good investment in 2026?

Gold can still play a role as a long-term hedge against inflation and uncertainty, but it’s not reliable in the short term. Its performance depends heavily on interest rates, the dollar, and global liquidity—not just geopolitical events.

Why is gold falling during a war?

Because markets are reacting to economic mechanics, not headlines. Rising oil prices increase inflation and interest rates, which reduces gold’s appeal. At the same time, investors and governments may sell gold to raise cash.

Does gold always go up during crises?

No. While gold often rises during uncertainty, it can fall if:

- Interest rates rise

- The U.S. dollar strengthens

- Investors need liquidity

These factors can outweigh the “fear trade.”

How do interest rates affect gold?

Gold doesn’t pay income. When interest rates rise, bonds and cash become more attractive, pulling money away from gold.

What role do central banks play in gold prices?

Central banks are major buyers of gold, but during economic stress they may:

- Slow purchases

- Sell reserves

This shift in demand can significantly impact prices.

Is gold better than stocks or bonds?

Not necessarily. Gold:

- Doesn’t generate income

- Relies on price appreciation alone

Stocks and bonds provide returns through earnings or interest, making them more productive assets over time.

Should you hold gold in your portfolio?

Yes—in moderation. Gold works best as:

- A diversification tool

- A hedge against extreme scenarios

But relying on it as a primary investment strategy is risky.

What’s the biggest misconception about gold?

That it always rises during crisis. In reality, gold follows liquidity and macroeconomic conditions, which can cause it to drop even when fear is high.

Leave a Reply