Quick Summary

Investing in gold is primarily about protecting wealth—not chasing high returns. The metal has historically served as a store of value, helping investors hedge against inflation, currency devaluation, and economic uncertainty. It also provides portfolio diversification, often moving independently from stocks and bonds, which can reduce overall risk.

Gold becomes especially valuable during market crashes, recessions, and geopolitical instability, where it tends to hold or increase its value while traditional assets decline. Its tangible nature and limited supply further enhance its appeal as a long-term hedge against financial system risks.

In short, gold isn’t about rapid growth—it’s about preserving purchasing power and stabilizing your portfolio during uncertain times.

Table of Contents

- The Real Reasons Gold Belongs in Your Portfolio

- Protection Against Currency Destruction

- Uncorrelated Performance During Market Stress

- Ownership Without Institutional Dependency or Counterparty Risk

- Historical Crisis Performance

- Universal Acceptance and Deep Liquidity

- Implementation Strategies That Actually Work

- Wealth Insurance Investing

- Key Takeaways

- Frequently Asked Questions

The Real Reasons Gold Belongs in Your Portfolio

1. Protection Against Currency Destruction

The mathematical reality of fiat currency is straightforward. Governments can create unlimited amounts of it. This is literally how modern monetary systems function.

When you hold dollars, euros, or any other paper currency, you own a claim on purchasing power that governments can dilute by expanding the money supply.

Gold provides a counterbalance to this structural dynamic because of basic geology and economics. All the gold ever mined throughout human history would fit in a cube roughly 22 meters on each side.

New gold production adds only about 1-2% to the total supply annually, constrained by the difficulty and expense of mining.

This scarcity doesn’t depend on policy or government promises. Planetary formation billions of years ago determined it.

The purchasing power comparison becomes stark when you examine long timeframes.

In 1913, before the Federal Reserve’s creation, a $20 bill and a one-ounce gold coin (also worth $20 at the time) had equivalent value. Today, that same paper $20 buys considerably less than it did then, while the gold coin is worth well over $3,000.

The gold maintained its purchasing power. The currency did not.

This matters enormously for retirees living on savings accumulated over decades of work. If you’ve spent 30-40 years building a nest egg, currency debasement can silently erode that purchasing power even if your account balance looks stable.

A portfolio allocation to gold directly addresses this risk without requiring you to forecast when inflation will accelerate or which policies will debase the currency.

The protection operates continuously, quietly maintaining value while paper assets fluctuate.

2. Uncorrelated Performance During Market Stress

Most diversification strategies fail when you need them most because assets that normally move independently suddenly correlate during crises. Stocks and corporate bonds both declined in 2008 because both depend on corporate profitability and credit availability.

Real estate and stocks both suffered because both depend on economic growth and credit conditions.

Even international stocks provide less diversification than many realize because global equity markets increasingly move together.

Gold genuinely behaves differently because it responds to different drivers. When stock markets decline because of recession fears, gold often rises as investors seek safety.

When bond yields fall during flight-to-quality episodes, gold appreciates alongside them.

When both stocks and bonds struggle during stagflation periods like the 1970s, gold can surge while traditional assets languish.

The mechanism behind this low correlation relates to gold’s role as a monetary choice as opposed to a productive asset. Stocks and bonds represent claims on future cash flows generated by economic activity.

Real estate generates rental income.

These assets all join in the economic cycle.

Gold doesn’t generate cash flows; it simply exists as a scarce, universally recognized store of value. However, we will discuss a means of investing in gold that does generate a yield very soon.

This basic difference creates the diversification benefit.

Research examining multi-decade periods confirms that adding gold allocations of 5-15% to traditional stock/bond portfolios reduces overall volatility while maintaining comparable returns. The mathematics work because gold’s independent price behavior smooths the portfolio’s total fluctuation.

During periods when stocks surge, the gold allocation might lag, but during market crashes, gold’s stability or appreciation offsets equity losses.

A common objection to gold and silver ownership is the opportunity cost of potential gains in the aforementioned risk assets.

The answer to this is gold and silver leases. Gold and silver leases provide investors with the opportunity to gain a competitive interest rate that matches or exceeds the yield on bonds. Monetary Metals is a gold investment company that delivers a real interest yield on gold, paid in actual gold.

Click the banner below to learn more about Monetary Metals’ fixed-income products, and get started earning a competitive interest rate in addition to gold’s natural price appreciation. Fill out their short contact form to get started.

3. Ownership Without Institutional Dependency or Counterparty Risk

This characteristic deserves more attention than it typically receives. When you own physical gold coins or bars, you possess an asset that doesn’t depend on anyone else’s solvency, honesty, or competence.

No counterparty can fail to deliver, no institution that must remain solvent, no government that must honor obligations.

Compare this to stocks, which represent partial ownership in companies that can go bankrupt. Or bonds, which are promises to pay that can default. Or bank deposits, which depend on the bank’s continued operation and the deposit insurance system’s funding.

Or even real estate, which needs enforceable property rights and a functioning legal system to maintain title.

Physical gold needs none of these intermediaries. The metal itself has intrinsic value recognized globally for thousands of years.

If your bank fails, your gold stays valuable.

If the stock market closes during a crisis, you still own your gold. If a company goes bankrupt, your gold is unaffected. If political upheaval disrupts property rights, gold stays portable and valuable.

The 2008 financial crisis illustrated this distinction vividly. Bear Stearns shareholders watched their stock value evaporate.

Lehman Brothers bondholders recovered pennies on the dollar. Money market funds “broke the buck,” returning less than investors deposited.

Meanwhile, physical gold owners simply held an asset whose value actually increased during the chaos, rising from around $800 in early 2008 to over $1,100 by late 2009.

This counterparty-free characteristic provides psychological benefits that extend beyond mathematical portfolio optimization.

During market turmoil, when headlines scream about bank failures and corporate bankruptcies, physical gold ownership offers genuine peace of mind.

You’re not wondering whether some institution will honor its obligations; you hold direct ownership of a globally recognized asset.

4. Historical Crisis Performance

Gold’s safe-haven reputation comes from documented performance across many crisis types. The pattern repeats consistently.

When uncertainty rises and traditional assets stumble, gold tends to appreciate or at least maintain value.

The 1970s stagflation period provides a particularly relevant case study for today’s environment. As oil shocks drove inflation higher and economic growth stagnated, stocks and bonds both struggled. The traditional 60/40 portfolio suffered meaningful losses in real terms.

Gold, meanwhile, surged from $35 per ounce in 1971 to over $800 by 1980, preserving and growing purchasing power while other assets floundered.

The 2008 financial crisis demonstrated gold’s crisis characteristics from a different angle. The initial market panic actually saw gold decline slightly alongside everything else as investors liquidated positions to meet margin calls.

But as the crisis deepened and central banks responded with unprecedented monetary expansion, gold began a multi-year rally that nearly doubled prices between 2008 and 2011.

Investors who owned gold before the crisis began enjoyed protection that late buyers missed.

More recently, the COVID-19 pandemic created a sharp test of gold’s defensive properties. In the initial market crash of March 2020, the S&P 500 fell nearly 34% from peak to trough.

Gold initially declined modestly but quickly recovered and pushed to new all-time highs above $2,000 per ounce by August 2020.

The divergent performance provided exactly the diversification benefit that strategic gold positions deliver.

Today, you are seeing massive gains in gold and silver as concerns about the dollar’s long-term solvency, the US national debt and deficits, and countries’ drawdown of US bonds start to grow.

Also, the increasing mass accumulations of gold bullion by world central banks that have remained steady for the last 10 years have provided a stable floor under the gold price.

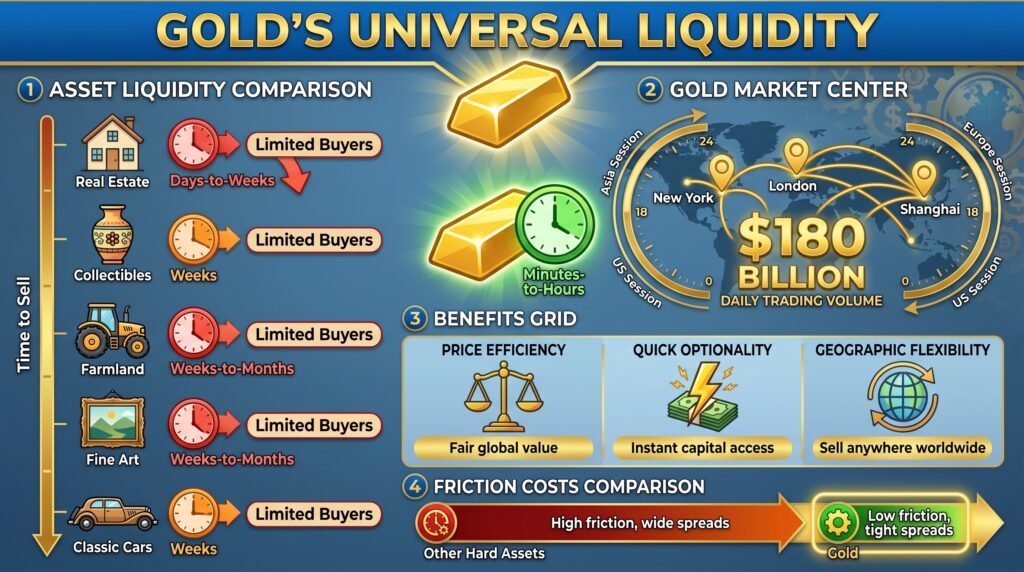

5. Universal Acceptance and Deep Liquidity

Some assets offer excellent theoretical characteristics but lack practical liquidity when you actually need to transact. Collectibles might hold value, but finding buyers takes time.

Certain real estate can be difficult to sell quickly.

Even some financial instruments have limited markets with wide bid-ask spreads.

Gold operates in a different universe entirely. The global gold market trades over $180 billion daily across many time zones and continents.

London, New York, Shanghai, and other financial centers maintain continuous markets with transparent pricing and large liquidity.

This depth means you can buy or sell meaningful positions without materially affecting the price or accepting unfavorable terms.

The practical implications extend beyond just trading convenience. Universal liquidity creates price efficiency, ensuring you receive fair value based on global market conditions as opposed to local supply constraints.

It provides optionality, allowing you to access capital quickly if circumstances change.

And it offers geographic flexibility, since gold’s global recognition means you can sell in any major city worldwide.

This liquidity characteristic distinguishes gold from other hard assets often proposed as inflation hedges. Farmland might protect against inflation, but selling acreage quickly at fair prices presents challenges.

Classic cars or fine art might appreciate, but finding qualified buyers willing to pay full value needs time and effort.

Gold’s liquidity eliminates these friction costs.

Implementation Strategies That Actually Work

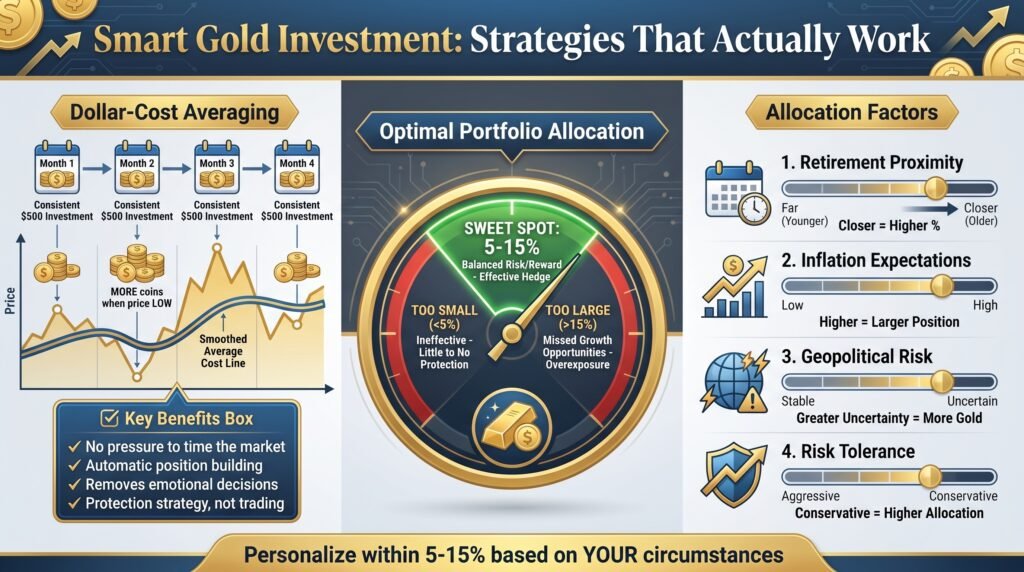

Dollar-cost averaging provides the most straightforward approach for most investors. Rather than attempting a single perfectly-timed purchase, you commit to buying fixed dollar amounts at regular intervals, perhaps monthly or quarterly.

This method automatically buys more ounces when prices are lower and fewer when prices are higher, smoothing your average cost over time.

The psychological advantage of dollar-cost averaging shouldn’t be underestimated. You eliminate the pressure to forecast market bottoms or worry about buying before a correction. Instead, you’re systematically building a position regardless of short-term price movements.

This aligns perfectly with gold’s strategic purpose; you’re gradually establishing protection, not trying to trade it.

Portfolio allocation percentages need personal consideration based on your specific circumstances, but the 5-15% range appears in recommendations from various financial institutions and advisors for good reasons.

Below 5%, the position may be too small to provide meaningful diversification benefits during market stress.

Above 15%, you’re potentially allocating too much to a non-yielding asset at the expense of growth opportunities.

Your allocation within that range should reflect several factors. Proximity to retirement matters; a closer retirement might justify higher allocations for protection.

Inflation concerns play a role; higher inflation expectations support larger positions.

Geopolitical risk assessment factors in, and greater uncertainty argues for more defensive positioning. Overall risk tolerance influences the decision; conservative investors might prefer higher gold allocations.

Avoiding Common Implementation Mistakes

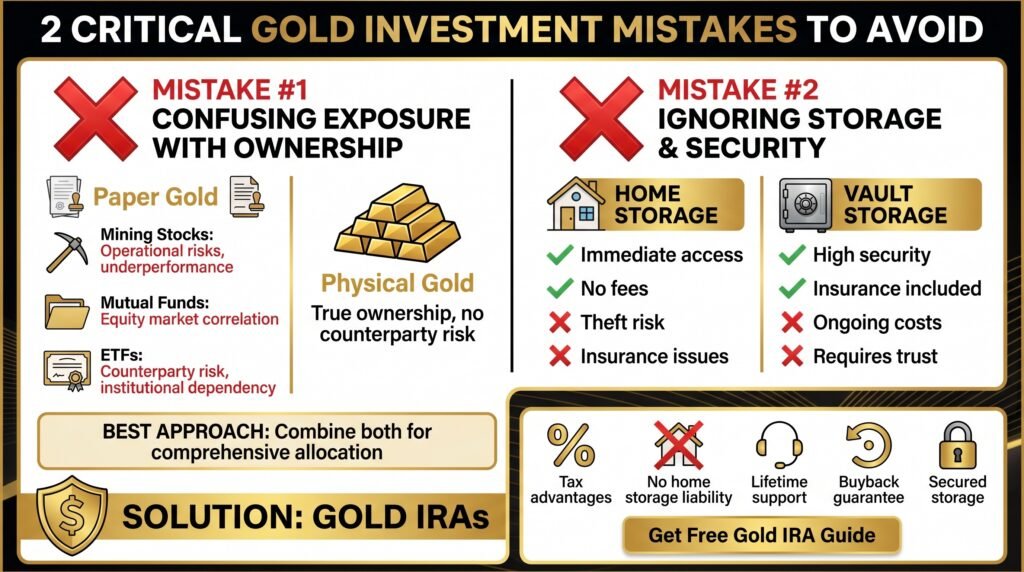

The first major mistake involves confusing gold exposure with gold ownership. Gold mining stocks, gold mutual funds, and gold ETFs all provide price exposure to gold, but they introduce counterparty risk and correlation to equity markets that physical gold ownership avoids.

Mining stocks often underperform gold itself because of operational challenges, regulatory issues, and general equity market correlation.

ETFs depend on institutional solvency and proper metal backing.

These paper gold choices offer advantages in tax-advantaged retirement accounts and provide convenient trading. But they fundamentally differ from direct physical ownership in ways that matter for gold’s core strategic purposes.

A comprehensive approach might include both physical holdings and paper exposure for different roles within your overall allocation.

The second mistake involves inadequate attention to storage and security for physical gold. Home storage provides immediate access and eliminates storage fees, but it introduces theft risk and potential insurance complications.

Professional vault storage offers high security and insurance, but it adds ongoing costs and requires trust in the storage provider.

The optimal solution depends on position size, the person’s circumstances, and risk preferences.

Gold IRAs are a tax-advantaged way of owning physical gold and silver without the need or liability of storing the actual precious metal in your own residence.

These gold IRA companies provide lifetime customer support, competitive price matches, buyback guarantees, low fees, and secured storage. See the links below to find the right gold IRA company that fits your individual needs. Fill out their short contact form and receive a free gold IRA guide.

Gold IRAs are a tax-advantaged way of owning physical gold and silver without the need or liability of storing the actual precious metal in your own residence.

These gold IRA companies provide lifetime customer support, competitive price matches, buyback guarantees, low fees, and secured storage. See the links in the video description to find the right gold IRA company that fits your individual needs. Fill out their short contact form and receive a free gold IRA guide.

The third mistake centers on buying gold from inappropriate sources at excessive premiums. Reputable dealers charge modest premiums over spot prices for standard bullion products.

Less scrupulous operators charge far higher markups for “rare” or “collectible” coins that don’t offer extra benefits for investment purposes.

Focus on recognized bullion products, American Eagles, Canadian Maple Leafs, or standard bars, from established dealers with transparent pricing.

Augusta Precious Metals is a gold IRA company with over a decade in the industry of providing account rollover services. Augusta is one of the leading gold investing companies for trust, customer empowerment, and prices.

Click the banner below to receive a free gold IRA integrity checklist from their official site. Fill out their sort contact form to get started.

Wealth Insurance Investing

Gold’s value in your portfolio has nothing to do with predicting price movements. The metal maintains purchasing power, reduces correlation to traditional assets, eliminates counterparty risk, provides crisis protection, and confirms liquidity.

Trying to time gold purchases represents a basic misunderstanding of its strategic purpose.

Implementation through dollar-cost averaging at suitable allocation percentages (5-15% depending on a person’s circumstances) provides the practical approach that aligns with gold’s characteristics. Physical ownership offers the final benefit set that paper choices can’t fully replicate, though both may play roles in a comprehensive strategy.

The investment sophistication required to use gold properly involves recognizing that some assets exist for protection, diversification, and wealth preservation across generations as opposed to growth. Mastering this distinction elevates your entire approach to portfolio construction beyond simple return chasing toward genuine risk management.

Key Takeaways

Gold’s value in your portfolio has nothing to do with predicting price movements. The metal maintains purchasing power, reduces correlation to traditional assets, eliminates counterparty risk, provides crisis protection, and confirms liquidity.

Trying to time gold purchases represents a basic misunderstanding of its strategic purpose.

Implementation through dollar-cost averaging at suitable allocation percentages (5-15% depending on a person’s circumstances) provides the practical approach that aligns with gold’s characteristics. Physical ownership offers the final benefit set that paper choices can’t fully replicate, though both may play roles in a comprehensive strategy.

The investment sophistication required to use gold properly involves recognizing that some assets exist for protection, diversification, and wealth preservation across generations as opposed to growth. Mastering this distinction elevates your entire approach to portfolio construction beyond simple return chasing toward genuine risk management.

To get started on your gold investing journey, obtain a free investment guide from one of the gold IRA companies below. Whether you require a company with a low investment minimum to get started or are a serious investor with a larger portfolio to protect, a tax-advantaged gold IRA is a great vehicle to own physical gold without the need or liability of storage within your own home.

Augusta Precious Metals: Best Gold IRA Company for Prices, Education, and Lifetime Customer Support. $50,000 Minimum.

Birch Gold Group: Most Trusted Customer Service, Low Investment Minimums, and Low Fees. $10,000 Minimum

Click the right banner for your individual needs. Fill out their short contact form on their site to get started.

Frequently Asked Questions

Can gold protect against inflation?

Gold has historically maintained purchasing power during inflationary periods. The 1970s provide the clearest example, when inflation averaged over 7% annually, and gold surged from $35 to over $800 per ounce.

More recently, during the 2021-2023 inflation spike, gold appreciated meaningfully while bond portfolios suffered losses.

The protection mechanism works because gold’s supply increases slowly (only 1-2% annually from mining) while fiat currency supplies can expand rapidly.

Should I buy physical gold or gold ETFs?

Physical gold provides final ownership without counterparty risk, making it ideal for the strategic protection role discussed throughout this article. Gold ETFs offer convenience and work well in retirement accounts where physical ownership presents challenges.

Many investors use both physical holdings for core strategic positions and ETFs for tactical allocations or retirement account exposure.

The choice depends on your specific goals and circumstances.

How much gold should I own in my portfolio?

Most financial advisors and institutions recommend allocations between 5-15% of total portfolio value. Below 5%, the position may not provide meaningful protection during market stress.

Above 15%, you’re potentially sacrificing too much growth potential from productive assets.

Your specific allocation within that range should reflect your proximity to retirement, inflation concerns, risk tolerance, and overall financial situation.

Is now a good time to buy gold?

This question reflects the timing mindset that misses Gold’s strategic purpose. The relevant question focuses on whether you now have adequate protection against currency debasement, market volatility, and systemic risks.

If you don’t have a gold position matching your target allocation, then yes, now is a suitable time to begin building one through dollar-cost averaging.

If you already maintain your target allocation, then no extra purchases are needed regardless of current prices.

Does gold pay dividends or interest?

Unless you are investing in a gold lease, gold generates no income, which represents one of its key characteristics as opposed to a weakness. Assets that generate cash flows, such as stocks, bonds, and rental properties, depend on economic activity and institutional functioning.

Gold’s value doesn’t need corporate profits, interest payments, or rental income.

This independence from cash flow generation provides the diversification benefit that makes gold valuable for portfolio protection as opposed to growth.

To get started on your gold investing journey, obtain a free investment guide from one of the gold IRA companies below. Whether you require a company with a low investment minimum to get started or are a serious investor with a larger portfolio to protect, a tax-advantaged gold IRA is a great vehicle to own physical gold without the need or liability of storage within your own home.

Click the right banner for your individual needs. Fill out their short contact form on their site to get started.

Leave a Reply