Quick Summary

Chasing short-term gold price moves is one of the biggest mistakes precious metals investors make. Gold prices are driven by emotion, fear, speculation, interest rates, currency strength, and geopolitical events — all of which create unpredictable volatility. Investors who buy after major rallies often enter near market peaks and risk panic-selling during corrections.

Instead of treating gold like a fast-moving trade, the article explains why it works better as a long-term wealth preservation asset and portfolio hedge. Successful investors typically focus on disciplined accumulation, diversification, and long-term strategy rather than trying to “time” gold price spikes. The article also highlights how emotional investing, FOMO, and headline-driven decisions can lead to poor returns and missed opportunities elsewhere.

Table of Contents

- Introduction

- Reason 1. Gold Should Not Be Treated as a Risk Asset.

- Reason 2. Gold Investing Requires a Deeper Understanding of the Investing Landscape

- Reason 3. Understanding Gold’s Strategic Purpose

- Reason 4. Making Portfolio Diversification a Priority. Not Price.

- Avoiding Gold Investing Mistakes

Introduction

Why are Americans often called ‘bubble chasers’? They wait until prices have already surged, read headlines about new all-time highs, feel that unmistakable pull of missing out, and then finally jump in, right before a topping, price stabilization, or a correction.

Most of the time, Americans are deal-finders and are always on the lookout for a deal. Sadly, with investing, when finding a bargain matters the most, many uneducated investors buy at the top and panic sell at the bottom.

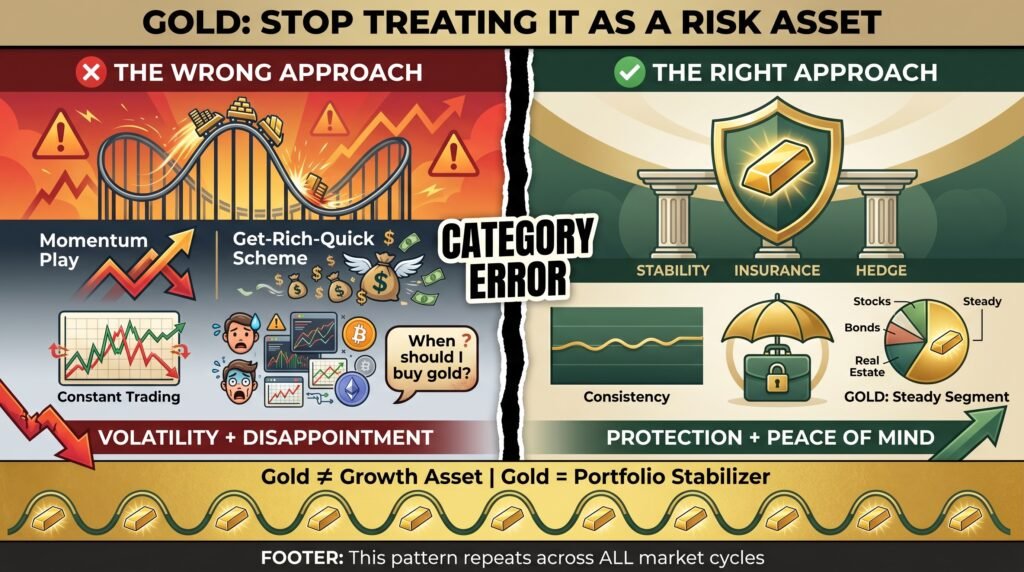

Reason 1. Gold Should Not Be Treated as a Risk Asset.

This pattern repeats itself with remarkable consistency across market cycles.

Gold investing should be one of the most straightforward components of a diversified portfolio. Gold provides stability, acts as insurance against currency devaluation, and offers a hedge during periods of genuine uncertainty.

When investors start treating it like a momentum play or a get-rich-quick scheme, they transform what should be a stabilizing force into a source of unnecessary volatility and disappointment.

The basic problem with chasing gold prices comes from the timing and the psychology that drives late-stage buying decisions.

The obsession with timing entries and exits, predicting price spikes, and trading around market sentiment has led countless people to miss the actual point of owning this metal.

The question “When should I buy gold?” fundamentally misunderstands what gold actually does in your financial life.

The recent prevailing narrative treats gold like a momentum stock or cryptocurrency, something you jump in and out of based on technical charts and analyst predictions.

Gold serves a completely different function than growth assets, and trying to trade it like one represents a basic category error that costs investors real money and genuine protection when they need it most.

Reason 2. Gold Investing Requires a Deeper Understanding of the Investing Landscape

Gold can best be characterized as wealth insurance. A long-held philosophy of gold ownership is ‘You don’t own gold to get rich. You own gold to keep from going broke.’

On the contrary, I imagine investors who bought gold in 2023 in the $2000 range have benefited greatly from the price appreciation.

However, you simply do not wait until the cost of insurance is at record highs to finally insure the car or house. That would be irrational. Correct? Well, the same goes for your wealth.

The real question shouldn’t be ‘Will the gold price continue rising?’ The real questions are: ‘Will the dollar continue to lose value?’ ‘Are we in an inflationary or stagflation currency environment?’, ‘Is there continued economic uncertainty?’, ‘Is there global conflict and geopolitical instability?’, ‘Will the national debt and monetary expansion continue to grow?’.

If you said yes to a majority of these questions, then the question of whether gold prices will continue to rise answers itself. In the affirmative. How fast or slow depends on the momentum of the answers from those prior questions.

Two more crucial questions should settle the matter. First, from a long view of history, how many fiat currencies have lost significant value, have gone to zero, or gone negative? Feel free to Google that one now. Secondly, how many times has gold gone to zero? You will not need to Google that answer.

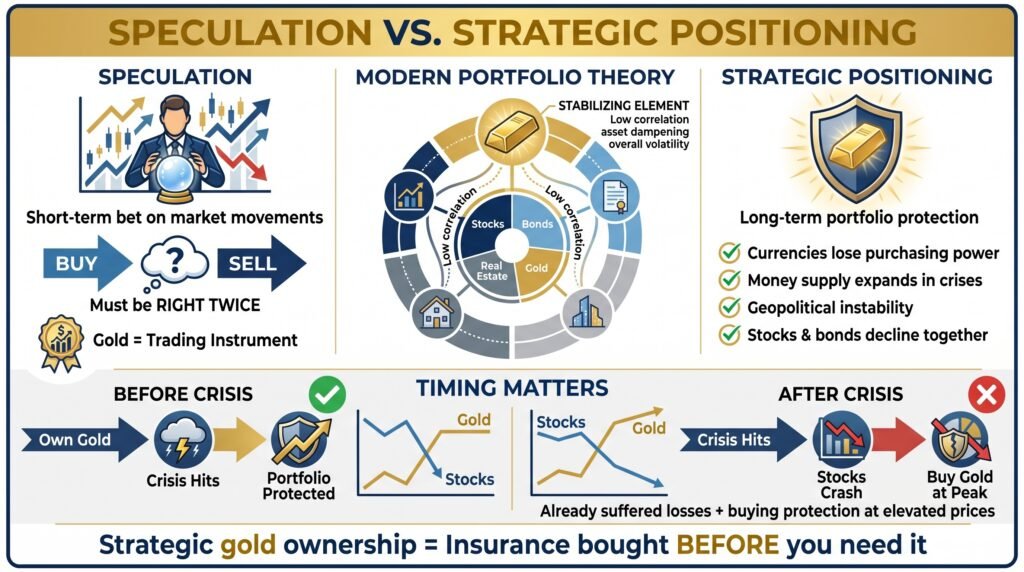

Reason 3. Understanding Gold’s Strategic Purpose

The distinction between speculation and strategic positioning might seem subtle, but these represent entirely different philosophies of investing. When you speculate on gold prices, you’re essentially making a bet on short-term market movements driven by sentiment, technical factors, and timing.

This approach needs you to be right twice, when you buy and when you sell, and it positions gold as just another tradable instrument in your portfolio.

Strategic gold ownership operates from a radically different premise. You’re acknowledging certain structural realities about modern financial systems.

Currencies lose purchasing power over time.

Governments expand money supplies during crises. Geopolitical tensions create financial instability.

Traditional assets like stocks and bonds sometimes move in synchronized declines.

The theoretical foundation here draws from decades of academic research on portfolio construction and risk management. Modern Portfolio Theory emphasizes the importance of combining assets with low correlation to reduce overall volatility.

Gold’s historical behavior during market stress periods provides exactly this characteristic, but only if you own it before the crisis hits.

Trying to buy gold after stocks have already crashed defeats the entire purpose; you’ve already suffered the equity losses, and you’re now buying protection at elevated prices.

Reason 4. Making Portfolio Diversification a Priority. Not Price.

If you are wheel-house as an investor is stocks and risk assets, you may need some guidance with gold investing. Gold is often seen as a ‘boring investment’. Of course, it is. It’s not supposed to be exciting.

Insurance is bought to protect the sports car; it’s not meant to be as exciting as driving the sports car itself. And you wouldn’t drive that lovely sports car down the crowded highway without insurance, would you?

However, the steady rise in the gold price in the last 3 years has provided some excitement for those who bought at the right time. They didn’t buy when gold was rocketing up in price. They bought gold because it was time to buy insurance and prepare for any time risk.

Yes, bonds do provide some hedging protection. But bonds are not a hard asset like precious metals, real estate, fine art, or the like. Bonds also suffer from a similar drawback that stocks suffer from, counterparty risk. That party is the federal government.

If we were living in a steady environment of fiscal responsibility, national debt solvency, zero inflation, and balanced budgets, then government bonds would probably be the only portfolio hedging asset you would need. But we do not live in this world and do not appear to be entering it at any point soon.

Regardless of the political party or administration in power, both sides appear to have a steady record and insatiable appetite for overspending. Hence, owning an asset that a counterparty cannot manipulate the supply and value of is of paramount importance.

Furthermore, certain gold investing vehicles can provide tax-deferred growth. Gold IRAs are a tax-advantaged way of owning physical gold and silver without the need or liability of storing the actual precious metal in your own residence.

These gold IRA companies provide lifetime customer support, competitive price matches, buyback guarantees, low fees, and secured storage. Click the banner below to get Augusta Precious Metals’ free gold IRA checklist. Fill out their short form to get started.

Avoiding Gold Investing Mistakes

The first major mistake involves confusing gold exposure with gold ownership. Gold mining stocks, gold mutual funds, and gold ETFs all provide price exposure to gold, but they introduce counterparty risk and correlation to equity markets that physical gold ownership avoids.

Mining stocks often underperform gold itself because of operational challenges, regulatory issues, and general equity market correlation.

ETFs depend on institutional solvency and proper metal backing.

These paper gold choices offer advantages in tax-advantaged retirement accounts and provide convenient trading. But they fundamentally differ from direct physical ownership in ways that matter for gold’s core strategic purposes.

A comprehensive approach might include both physical holdings and paper exposure for different roles within your overall allocation.

The second mistake involves inadequate attention to storage and security for physical gold. Home storage provides immediate access and eliminates storage fees, but it introduces theft risk and potential insurance complications.

Professional vault storage offers high security and insurance, but it adds ongoing costs and requires trust in the storage provider.

The optimal solution depends on position size, the person’s circumstances, and risk preferences.

Gold IRAs are a tax-advantaged way of owning physical gold and silver without the need or liability of storing the actual precious metal in your own residence.

These gold IRA companies provide lifetime customer support, competitive price matches, buyback guarantees, low fees, and secured storage. See the links below to find the right gold IRA company that fits your individual needs. Fill out their short contact form and receive a free gold IRA guide.

Gold IRAs are a tax-advantaged way of owning physical gold and silver without the need or liability of storing the actual precious metal in your own residence.

These gold IRA companies provide lifetime customer support, competitive price matches, buyback guarantees, low fees, and secured storage. See the links in the video description to find the right gold IRA company that fits your individual needs. Fill out their short contact form and receive a free gold IRA guide.

The third mistake centers on buying gold from inappropriate sources at excessive premiums. Reputable dealers charge modest premiums over spot prices for standard bullion products.

Less scrupulous operators charge far higher markups for “rare” or “collectible” coins that don’t offer extra benefits for investment purposes.

Focus on recognized bullion products, American Eagles, Canadian Maple Leafs, or standard bars, from established dealers with transparent pricing.

Augusta Precious Metals is a gold IRA company with over a decade in the industry of providing account rollover services. Augusta is one of the leading gold investing companies for trust, customer empowerment, and prices.

Click the banner below to receive a free gold IRA integrity checklist from their official site. Fill out their sort contact form to get started.

Frequently Asked Questions

Is gold a bad investment?

Not necessarily. Gold can serve as a hedge against inflation, economic uncertainty, and currency weakness. However, problems often arise when investors chase rapid price increases or treat gold as a short-term speculation vehicle instead of a long-term portfolio diversifier.

Why is chasing the gold price risky?

Gold prices can swing sharply due to changing interest rates, geopolitical tensions, investor sentiment, and currency movements. Investors who buy after large rallies may enter near temporary highs and suffer losses during pullbacks.

What is the biggest mistake gold investors make?

One of the biggest mistakes is emotional investing — buying because prices are surging or headlines create fear of missing out. This often leads to buying high and selling low during corrections.

Is gold better for long-term investing?

Many investors use gold primarily as a long-term store of value and portfolio hedge rather than a short-term trading asset. Long-term accumulation strategies generally reduce the risks associated with trying to time the market.

Why doesn’t gold always rise during crises?

While gold is considered a safe-haven asset, it can still fall during periods of market stress. Investors sometimes sell gold to raise cash, cover losses, or respond to rising interest rates and a stronger U.S. dollar.

Does gold generate income like stocks or bonds?

No. Physical gold does not pay dividends or interest. Returns depend entirely on price appreciation, which is why some investors view it as a hedge or insurance asset rather than a growth investment.

Gold Leases, such as those provided by Monetary Metals, generate a fixed-income return competitive with the interest yield produced by bonds. The company provides a real yield on your gold investment, paid in actual gold. See the link here to learn more.

Leave a Reply